HSBC 2005 Annual Report Download - page 98

Download and view the complete annual report

Please find page 98 of the 2005 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

|

|

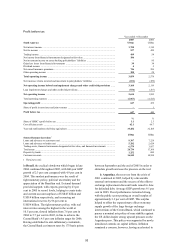

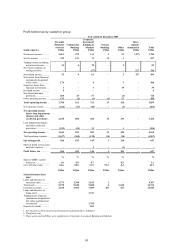

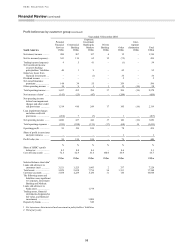

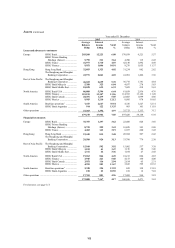

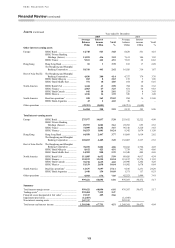

HSBC HOLDINGS PLC

Financial Review (continued)

96

as a proportion of assets increased by 3 percentage

points in the SME portfolio, in line with overall

market performance, and MME credit quality also

declined slightly. In Argentina, net recoveries

decreased as significant releases from amounts

recognised at the time of the sovereign debt default

and pesification were not repeated. However,

underlying credit quality improved substantially and

impaired loans as a percentage of assets more than

halved.

Operating expenses of US$368 million were

19 per cent higher than in 2004, though the cost

efficiency ratio improved by 3 percentage points as

income grew faster than costs. Staff numbers in

Brazil increased by 34 per cent following a

recruitment drive initiated in the second half of 2004

to support expansion of the SME business. Higher

incentive payments, reflecting increased income, and

union agreed pay increases also contributed to an

increase in staff costs. New marketing campaigns,

including the award winning ‘30, 60, 90 Dias de

Apuros’ campaign focusing on invoice financing,

increased advertising and marketing costs. Expenses

in Argentina increased by 24 per cent, driven by

higher staff costs, reflecting pay rises agreed with

local unions, together with a 9 per cent increase in

headcount in support of business expansion.

Corporate, Investment Banking and Markets

reported a pre-tax profit of US$146 million, an

increase of 12 per cent, driven by higher net interest

income in Argentina and a decline in loan impairment

charges in Brazil.

Total operating income at US$313 million

decreased by 7 per cent compared with 2004. In

Argentina, a reduction in funding costs in Global

Markets was augmented by the positive impact of an

appreciating CER (an inflation-linked index) on

holdings of government bonds. Continuing economic

growth and improved market confidence stimulated

demand for credit, resulting in a 67 per cent growth

in balances. Brazil reported a decrease in balance

sheet management and money market revenues as a

result of high short-term interest rates and an inverted

yield curve.

Trading activities generated higher income as

Global Markets in Brazil benefited from a wider

product range and the addition of new delivery

capabilities. This investment and the relatively

buoyant local market resulted in higher business

volumes, particularly in foreign exchange. In

Argentina, Global Markets income rose in line with

increased trading activity in response to the sovereign

debt swap.

In Brazil, a US$15 million net release of loan

impairment charges compared favourably with a net

charge in 2004. A recovery in the energy sector was

accompanied by the non-recurrence of allowances

raised against two specific corporate accounts in

2004.

Operating expenses of US$138 million were

8 per cent lower than in 2004, primarily due to a

reduction in profit share and bonus payments in

Brazil. This was partly offset by higher centralised

support function staff costs, driven by pay rises

agreed with local unions. In Argentina, operating

expenses were broadly in line with 2004.

Private Banking reported a pre-tax profit of

US$1 million, a modest increase on 2004. The

business was reorganised in 2005, with the transfer of

smaller accounts to Personal Financial Services in

Brazil, following a resegmentation of the customer

base.

In Brazil, HSBC’s insurance business was

reclassified from Other to Personal Financial

Services. As a result, operating income decreased by

US$106 million and operating expenses were

US$90 million lower. In Argentina, the receipt of

compensation bonds and other items related to the

pesification in 2002 led to a US$17 million increase

in profit before tax.