HSBC 2005 Annual Report Download - page 149

Download and view the complete annual report

Please find page 149 of the 2005 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

|

|

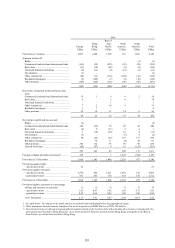

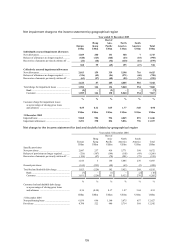

147

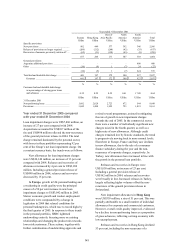

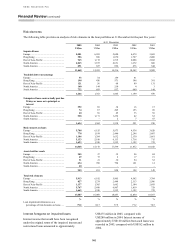

were also improvements in mainland China and

Singapore, due to strong economic growth.

In North America, impaired loans increased by

4 per cent to US$4,045 million. This rise reflected

portfolio growth and accelerated bankruptcies ahead

of new US legislation, particularly in secured and

personal unsecured lending. The trend in US

impaired loans as a percentage of gross receivables

was stable year-on-year. In Mexico, impaired loans

increased in line with portfolio growth. Improving

credit conditions in Canada, on the back of a strong

economy, drove a decrease in impaired loans,

offsetting the rises in the US and Mexico.

A rise of 26 per cent to US$891 million in South

America’s impaired loans was mainly due to the

34 per cent increase in Brazil. This was partly driven

by strong balance sheet growth, but there was also

some weakening in credit quality in the consumer

finance business, particularly in the low income

segment. Action taken during the year to amend

lending parameters has assisted in stabilising

delinquency. Argentina’s economy continued its

steady recovery and as a result impaired loans

declined by 9 per cent, partly offsetting the rise in

Brazil.

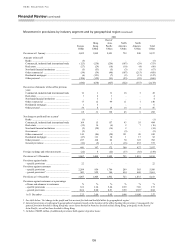

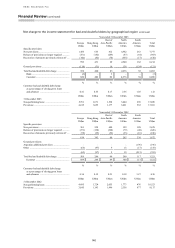

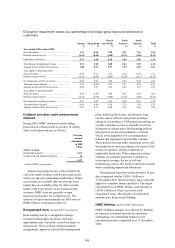

Troubled debt restructurings

US GAAP requires separate disclosure of any loans

whose terms have been modified because of

problems with the borrower to grant concessions

other than are warranted by market conditions. These

are classified as ‘troubled debt restructurings’ and

are distinct from the normal restructuring activities

described above. Disclosure of troubled debt

restructurings may be discontinued after the first

year if the debt performs in accordance with the new

terms.

The fall in troubled debt restructurings was

driven by the decline in Hong Kong, a product of the

continuing improvement in the quality of the loan

book.

Unimpaired loans past due 90 days or more

The rise in Europe was due to the UK, where

improved processes led to better credit data

collection. In North America, HSBC Finance’s

business benefited from improvement in delinquency

and default trends year on year. In common with

other card issuers, including other parts of HSBC,

HSBC Finance continues to accrue interest on credit

cards past 90 days until charged off. Appropriate

provisions are raised against the proportion judged to

be irrecoverable.

Potential problem loans

Credit risk elements also cover potential problem

loans. These are loans where information about

borrowers’ possible credit problems causes

management serious doubts about the borrowers’

ability to comply with the loan repayment terms.

There are no potential problem loans other than

those identified in the table of risk elements set out

below.