HSBC 2005 Annual Report Download - page 147

Download and view the complete annual report

Please find page 147 of the 2005 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

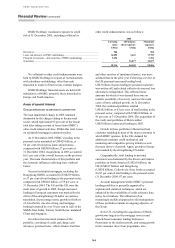

|

|

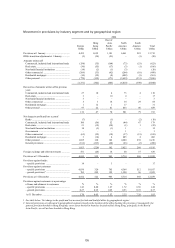

145

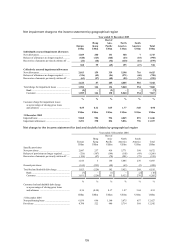

contributed to increased vehicle finance lending.

With the exception of the areas immediately affected

by Hurricane Katrina, the US housing market

remained strong, supported by low interest rates and

transaction costs, and increased availability of credit.

Within the US, HSBC’s portfolios remained

geographically diverse, and were largely secured by

first lien positions.

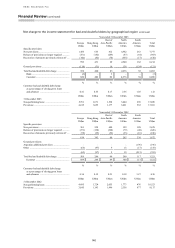

Although increased mortgage borrowing has

contributed to the record level of consumer debt

burden in the US, levels have largely stabilised and

are expected to decline gradually, as incomes rise

sufficiently to repay debt, notwithstanding higher

interest rates. Bankruptcy filings increased sharply in

the second half of 2005 as a result of a change in

legislation, but receded to more modest levels by the

end of the year. This has continued into 2006.

Notwithstanding the effect of additional impairment

allowances required for the Hurricane Katrina and

increased bankruptcy filings, delinquency rates

continued to fall across the majority of portfolios

during 2005, and trends in lending quality improved.

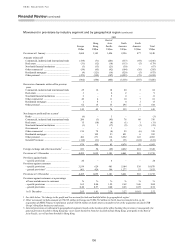

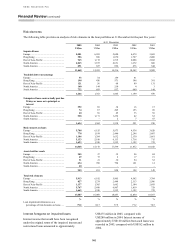

In Mexico, HSBC utilised well-developed

distribution capabilities and enhanced marketing

initiatives to grow consumer lending, card and

mortgages. Net interest margin was partially offset

by a lower interest rate environment during the year.

In the UK, growth in personal lending was

mainly in the mortgage market, where HSBC

focused on retaining existing customers, and

increasing market share through competitive pricing

and marketing strategies. Fixed rate mortgages were

the main driver of growth, against the background of

a more subdued market. Overall, the secured

mortgage portfolio represented 64 per cent of total

lending to personal customers in the UK, and

although delinquency increased modestly during

2005, losses remained negligible.

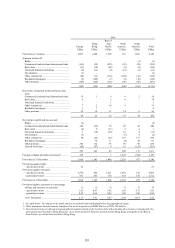

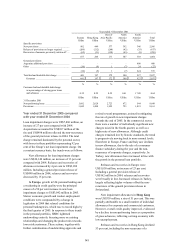

The unsecured portfolio in the UK also

continued to expand, driven by credit and charge

cards, and to a lesser extent unsecured personal

lending, though growth in gross lending was largely

offset by the US$1 billion write-off mentioned

above. In response to prevailing market conditions,

which saw a progressive rise in personal

indebtedness, bankruptcies and delinquencies over

the course of 2005, HSBC revised credit scorecards,

adopted positive credit reference data, further

centralised underwriting, and expanded its

origination and collection analytics and efforts. As a

result, there were indicators in the second half of the

year that the credit quality of more recent unsecured

lending vintages had improved.

Personal lending in Hong Kong remained

subdued in 2005. The mortgage market remained

intensely competitive, with competitors offering very

low rates, along with up-front cash incentives to

attract new mortgage business. Overall mortgage

balances, excluding the reduction in balances under

the GHOS, which remained suspended, were broadly

flat compared with December 2004. Credit quality

continued to improve, with consumers benefiting

from employment levels and rising property prices,

with a notable reduction in the level of negative

equity on mortgage balances.

In contrast with Hong Kong, personal lending in

the Rest of Asia-Pacific grew strongly in most

countries in 2005, boosted by a series of mortgage

and credit card campaigns during the year and

growth in the card base, which added 1.6 million

cards, to reach 6.3 million cards in issue at the end of

2005.

Growth was also notable in Brazil, where

marketing and new product launches contributed to

growth of 44 per cent in personal unsecured lending,

as consumer sentiment improved with economic

growth. Credit quality deteriorated, notably in the

consumer finance business, however, actions taken

to mitigate this, notably through tightening

underwriting, delivered an improvement in the

fourth quarter.

Elsewhere, credit quality remained relatively

stable, although HSBC continued to monitor

carefully those portfolios that possess the greatest

potential for future economic stress. Delinquency

and loss trends differed across jurisdictions,

reflecting these varied conditions.

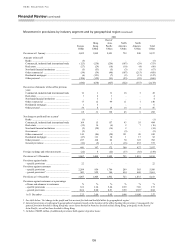

Non-traditional lending

In response to customer demand, HSBC offers

interest only residential mortgage loans in more

developed markets. These loans allow customers to

pay only accruing interest for a period of time, and

provide customers with the repayment flexibility

inherent in the structures of such products. An

increasing number of customers prefer to make one-

off, or irregular capital reduction payments through

the lifetime of such loans, reflecting their individual

income patterns.

HSBC underwrites and prices these loans in a

manner appropriate to compensate for their risk by

ensuring, for example, that loan-to-value ratios are

more conservative than for traditional mortgage

lending. HSBC does not offer loans which are

designed to expose customers to the risk of negative

amortisation.