HSBC 2005 Annual Report Download - page 402

Download and view the complete annual report

Please find page 402 of the 2005 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

392 -

393

393 -

394

394 -

395

395 -

396

396 -

397

397 -

398

398 -

399

399 -

400

400 -

401

401 -

402

402 -

403

403 -

404

404 -

405

405 -

406

406 -

407

407 -

408

408 -

409

409 -

410

410 -

411

411 -

412

412 -

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

|

|

HSBC HOLDINGS PLC

Notes on the Financial Statements (continued)

400

does not recognise a gain in a secured financing transaction. At 31 December 2005, secured financings of

US$18.2 billion included in long-term debt were secured by US$25.6 billion of customer loans.

Prior to the third quarter of 2004, HSBC sold MasterCard and Visa private label, personal non-credit card and

vehicle finance loans in various securitisation transactions. HSBC continues to service and receive servicing fees

on the outstanding balance of these securitised loans and retains rights to future cash flows arising from the loans

after the investors receive their contractual return. HSBC has also, in certain cases, retained other subordinated

interests in these securitisations. These transactions result in the recording of interest-only strip receivables,

which represent the value of the future residual cash flows from securitised loans. The investors and the

securitisation trusts have only limited recourse to HSBC assets for failure of debtors to pay. That recourse is

limited to HSBC’s rights to future cash flows and any subordinated interest retained. Servicing assets and

liabilities are not recognised in conjunction with securitisations since HSBC receives adequate compensation

relative to current market rates to service the loans sold.

Securitisation-related revenue includes income associated with the current and prior period securitisation of

loans with limited recourse structured as sales under US GAAP. Such income includes gains on sales, net of the

estimate of probable credit losses under the recourse provisions, servicing income and excess spread relating to

those loans.

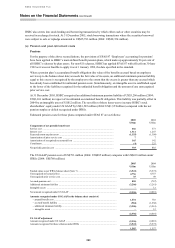

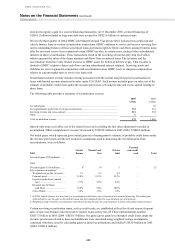

The following table provides a summary of securitisation revenue:

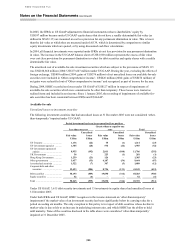

2005 2004

US$m US$m

Net initial gains ....................................................................................................................... –25

Net replenishment gains from revolving securitisations .......................................................... 154 414

Servicing revenue and excess spread ....................................................................................... 212 569

Other ....................................................................................................................................... 6–

Total securitisation revenue ..................................................................................................... 372 1,008

Interest-only strip receivables, net of the related losses and excluding the fair value adjustment recorded in

accumulated ‘Other comprehensive income’ decreased by US$258 million in 2005 (2004: US$466 million).

Net initial gains, which represent gross initial gains net of management’s estimate of probable credit losses under

the recourse provisions, and the key economic assumptions used in measuring the net initial gains from

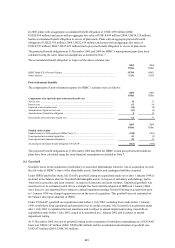

securitisations, were as follows:

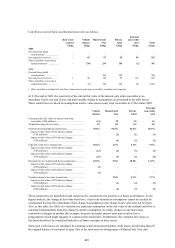

2005

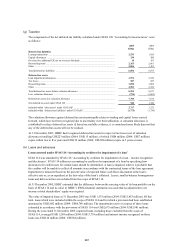

Vehicle

finance

MasterCard/

Visa

Private

label

Personal

non-credit

card Total

Net initial gains (US$ millions) ........ –––––

2004

Net initial gains (US$ millions) ........ 61145–25

Key economic assumptions2

Weighted average life (in years) ... 2.1 0.3 0.4 –

Payment speed .............................. 35.0% 93.5% 93.5% –

Expected credit losses (annual

rate) .......................................... 5.7% 4.9% 4.8% –

Discount rate for future

cash flows ................................ 10.0% 9.0% 10.0% –

Cost of funds ................................ 3.0% 1.5% 1.4% –

1In 2004, vehicle finance was involved in a securitisation which later was restructured as a secured financing. The initial gain

reflected above was the gain on the initial transaction that remained after the securitisation was restructured.

2Weighted average rates for securitisations entered into during the year for securitisations of loans with similar characteristics.

Certain revolving securitisation trusts, such as credit cards, are established at fixed levels and require frequent

sales of new loan balances into the trusts to replace loans as they run off. These replenishments totalled

US$17.5 billion in 2005 (2004: US$30.3 billion). Net gains (gross gains less estimated credit losses under the

recourse provisions) related to these replenishments were calculated using weighted average assumptions

consistent with those used for calculating gains on initial securitisations, and totalled US$154 million in 2005

(2004: US$414 million).