HSBC 2005 Annual Report Download - page 158

Download and view the complete annual report

Please find page 158 of the 2005 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

|

|

HSBC HOLDINGS PLC

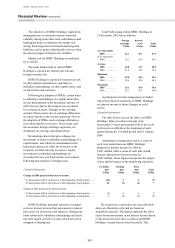

Financial Review (continued)

156

Non-trading (Audited IFRS 7 information)

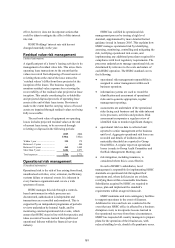

The principal objective of market risk management

of non-trading portfolios is to optimise net interest

income.

Market risk in non-trading portfolios arises

principally from mismatches between the future

yield on assets and their funding cost, as a result of

interest rate changes. Analysis of this risk is

complicated by having to make assumptions on

optionality in certain product areas, for example,

mortgage prepayments, and from behavioural

assumptions regarding the economic duration of

liabilities which are contractually repayable on

demand, for example, current accounts. The

prospective change in future net interest income

from non-trading portfolios will be reflected in the

current realisable value of these positions, should

they be sold or closed prior to maturity. In order to

manage this risk optimally, market risk in non-

trading portfolios is transferred to Global Markets or

to separate books managed under the supervision of

the local ALCO.

The transfer of market risk to books managed by

Global Markets or supervised by ALCO is usually

achieved by a series of internal deals between the

business units and these books. When the

behavioural characteristics of a product differ from

its contractual characteristics, the behavioural

characteristics are assessed to determine the true

underlying interest rate risk. Local ALCOs regularly

monitor all such behavioural assumptions and

interest rate risk positions, to ensure they comply

with interest rate risk limits established by the Group

Management Board.

As noted above, in certain cases, the non-linear

characteristics of products cannot be adequately

captured by the risk transfer process. For example,

both the flow from customer deposit accounts to

alternative investment products and the precise

prepayment speeds of mortgages will vary at

different interest rate levels. In such circumstances,

simulation modelling is used to identify the impact

of varying scenarios on valuations and net interest

income.

Once market risk has been consolidated in

Global Markets or ALCO-managed books, the net

exposure is typically managed through the use of

interest rate swaps within agreed limits.

The principal non-trading risks which are not

included in VAR for Global Markets (see ‘Value at

risk’ above) are detailed below.

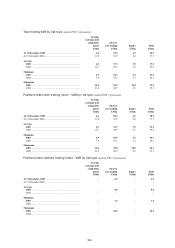

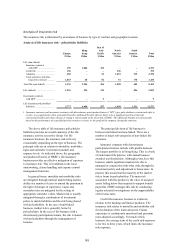

Market risk within HSBC Finance primarily

arises from mismatches between future

behaviouralised asset yields and their funding costs.

This mismatch mainly comes from the fact that asset

yields are predominantly fixed and relatively

insensitive to market movements in interest rates,

whereas the related wholesale funding and its

associated derivatives are more sensitive to such

movements. This non-trading risk is principally

managed by controlling the sensitivity of projected

net interest income under varying interest rate

scenarios: see ‘Net interest income’ below.

VAR limits are set to control the total market

risk exposure of HSBC Finance. The VAR as at

31 December 2005 was US$13.5 million (2005

average: US$13.4 million; 2005 minimum:

US$6.2 million; 2005 maximum: US$41.6 million),

compared with US$9.1 million at 31 December 2004

(2004 average: US$16.1 million; 2004 minimum:

US$4.1 million; 2004 maximum: US$31.9 million).

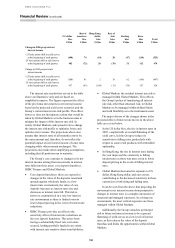

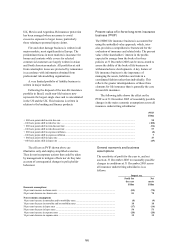

Market risk arising in the prime residential

mortgage business of HSBC Bank USA is primarily

managed by a specialist function within the business,

under guidelines established by HSBC Bank USA’s

ALCO. A range of risk management tools is applied

to hedge the sensitivity arising from movements in

interest rates. The key element of market risk within

the US prime mortgage business relates to the

prepayment options embedded in US mortgages,

which affect the sensitivity of the value of mortgage

servicing rights (‘MSRs’) to interest rate movements

and the net interest margin on mortgage assets.

MSRs represent the economic value of the right to

receive fees for performing specified residential

mortgage servicing activities. They are sensitive to

interest rate movements because lower rates

accelerate the prepayment speed of the underlying

mortgages and therefore reduce the value of the

MSRs. The reverse is true for rising rates. HSBC

uses a combination of interest rate-sensitive

derivatives and debt securities to help protect the

economic value of MSRs. An accounting asymmetry

can arise in this area because the derivatives used to

hedge the economic exposure arising from MSRs are

always measured at fair value, but the MSRs

themselves are measured for accounting purposes at

the lower of amortised cost and valuation. It is,

therefore, possible for an economically hedged

position not to be shown as such in the accounts,

when the hedge shows a loss but the MSR cannot be

revalued above cost to reflect the related profit.

HSBC’s policy again is to hedge the economic risk.

VAR limits are set to control the exposure to

MSRs and MSR hedges. The VAR on MSRs and

MSR hedges at 31 December 2005 was

US$3.9 million (2005 average: US$3.2 million; 2005

minimum: US$2.4 million; 2005 maximum: