HSBC 2005 Annual Report Download - page 79

Download and view the complete annual report

Please find page 79 of the 2005 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

|

|

77

consequently deposit balances grew by 13 per cent,

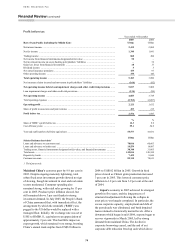

while deposit spreads increased by 13 basis points.

Lending balances rose by 27 per cent, following the

selective recruitment of more experienced

relationship managers and a reorganisation of

customers into key industrial sectors to provide

greater focus on identifying service opportunities.

Asset spreads decreased by 42 basis points as a result

of competitive pressures and market liquidity.

In Taiwan, a loyalty campaign designed to

increase deposits, together with higher current

account income and an increase in deposit spreads,

contributed to an 80 per cent increase in net interest

income. In Mauritius, net interest income doubled as

a result of liability balance growth. In India,

increased trade contributed to higher trade services

net interest income and strong economic growth led

to higher demand for credit. This resulted in lending

balances increasing by 72 per cent, while customer

acquisition increased average current account

balances by 37 per cent. Liability spreads widened by

73 basis points following interest rate rises. In

Indonesia, increased sales efforts and a more focused

approach to customer relationship management

contributed to an 84 per cent growth in asset balances

and a 66 per cent increase in net interest income.

Net fee income of US$307 million was 15 per

cent higher than in 2004. In the Middle East,

increased trade flows led to a 17 per cent increase in

trade services income, while current account income

increased by 80 per cent, benefiting from the

introduction of new cash management capabilities.

Short-term IPO loan funding reflecting, in part,

robust regional capital market, also contributed to a

40 per cent increase in net fee income. In mainland

China, a 31 per cent increase in trade customers and a

significant rise in imports led to higher trade services

income, while a 49 per cent increase in current

account customers and higher lending fees also

contributed to an 8 per cent increase in fee income.

Increased lending, current account and trade

activities raised net fee income by 30 per cent in

Indonesia. A number of sites, including Vietnam and

Thailand, also reported strong growth, driven by the

success of HSBC’s strategy of focusing on business

opportunities involving international trade.

There was a net release of loan impairment

charges of US$67 million, following net charges in

2004. Credit quality in the Middle East improved. In

mainland China there was a significant reduction in

loan impairment charges as higher collective

impairment charges were more than offset by the

release of allowances against a small number of

accounts and the non-recurrence of a significant

charge against a single customer in 2004. In India,

strong economic growth led to improved credit

quality, while in Malaysia, Singapore and Indonesia,

credit quality improved significantly although

releases of impairment charges were lower than in

2004.

Operating expenses were 27 per cent higher than

last year, broadly in line with revenue growth. In the

Middle East, the recruitment of sales and support

staff substantially increased income, leading to

higher incentive payments. In mainland China,

revenue growth was driven by branch expansion,

increased sales and support staff and higher

marketing expenditure. In Malaysia, the direct sales

teams were expanded and business banking units

were extended to all branches in support of the

bank’s growth strategy, resulting in a 16 per cent

increase in costs.

In India, the recruitment of additional sales staff

boosted customer facing staff by 85 per cent in 2005.

In South Korea, staff recruitment and heightened

marketing activity supported HSBC’s four recently

established commercial banking centres, contributing

to an increase in costs. Higher costs throughout the

rest of the region largely reflected increases in sales

and support staff and initiatives to support business

expansion.

Increased income from associates reflected

strong performance in The Saudi British Bank and

gains on the sale of HSBC’s stake in MISR

International, an Egyptian Bank. Income from the

bank’s strategic investments in China, Bank of

Communications and Industrial Bank, which were

acquired in 2004, also increased.

Corporate, Investment Banking and Markets

reported a pre-tax profit of US$1,207 million, an

increase of 22 per cent compared with 2004. HSBC’s

progress in this region was marked by positive

revenue trends across most countries, with strong

growth being reported in the Middle East, Malaysia,

South Korea, India and mainland China.

Operating income rose by 25 per cent to

US$1,769 million. Higher Corporate and Institutional

Banking revenues reflected a 53 per cent increase in

lending balances in mainland China, a result of

strong demand for corporate credit, primarily from

the industrial and technology sector. Deposit

balances increased by 36 per cent and, together with

a 40 basis point rise in deposit spreads, this also

contributed to the growth in revenues.

HSBC’s operations in the Middle East reported a

63 per cent rise in customer advances, primarily due

to strong demand for corporate credit, driven by

government spending on regional infrastructure