HSBC 2005 Annual Report Download - page 383

Download and view the complete annual report

Please find page 383 of the 2005 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

373 -

374

374 -

375

375 -

376

376 -

377

377 -

378

378 -

379

379 -

380

380 -

381

381 -

382

382 -

383

383 -

384

384 -

385

385 -

386

386 -

387

387 -

388

388 -

389

389 -

390

390 -

391

391 -

392

392 -

393

393 -

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

|

|

381

terminated, the qualifying derivative was immediately marked to market and any gain or loss arising was taken

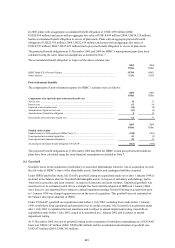

to the income statement.

US GAAP

• The accounting under SFAS 133 ‘Accounting for derivative instruments and hedging activities’ is generally

consistent with that under IAS 39, which HSBC has followed in its IFRSs reporting from 1 January 2005, as

described above. However, specific assumptions regarding hedge effectiveness under US GAAP are not

permitted by IAS 39.

• The requirements of SFAS 133 have been effective from 1 January 2001.

• The US GAAP ‘shortcut method’ permits an assumption of zero ineffectiveness in hedges of interest rate risk

with an interest rate swap provided specific criteria have been met. IAS 39 does not permit such an assumption,

requiring a measurement of actual ineffectiveness at each designated effectiveness testing date.

• In addition, IFRSs allow greater flexibility in the designation of the hedged item. Under US GAAP, all

contractual cash flows must form part of the designated relationship, whereas IAS 39 permits the designation of

identifiable benchmark interest cash flows only.

• Certain issued structured notes are classified as trading liabilities under IFRSs, but not under US GAAP. Under

IFRSs, these notes will be held at fair value, with changes in fair value reflected in the income statement. Under

US GAAP, if the embedded derivative is not ‘clearly and closely related’ to the host contract, the embedded

derivative will be bifurcated and measured at fair value, the host contract will be measured at amortised cost, and

changes in both will be reflected in the income statement. If the embedded derivative is clearly and closely

related to the host contract, the issued note will be held at amortised cost in its entirety, with changes in the

amortised cost reflected in the income statement.

• Under US GAAP, derivatives receivable and payable with the same counterparty may be reported net on the

balance sheet when there is an executed ISDA Master Netting Arrangement covering enforceable jurisdictions.

These contracts do not meet the requirements for offset under IAS 32 and hence are presented gross on the

balance sheet under IFRSs.

Impact

• HSBC’s North American subsidiaries continue to follow the ‘shortcut method’ of hedge effectiveness testing for

certain transactions in their US GAAP reporting. Alternative hedge effectiveness testing methodologies are

sought under IFRSs for these hedging relationships.

• Apart from certain subsidiaries in North America, HSBC has chosen not to adopt hedge accounting for US

GAAP purposes as this would require a designated hedged item inconsistent with the approach adopted under

IFRSs. Qualifying IAS 39 hedging derivatives have been measured at fair value with the gain or loss recognised

in net income for US GAAP purposes.

Designation of financial assets and liabilities at fair value through profit and loss

IFRSs

• Under IAS 39, a financial instrument, other than one held for trading, is classified in this category if it meets the

criteria set out below, and is so designated by management. An entity may designate financial instruments at fair

value where the designation:

− eliminates or significantly reduces a measurement or recognition inconsistency that would otherwise arise

from measuring financial assets or financial liabilities or recognising the gains and losses on them on

different bases; or

− applies to a group of financial assets, financial liabilities or a combination of both that is managed and its

performance evaluated on a fair value basis, in accordance with a documented risk management or

investment strategy, and where information about that group of financial instruments is provided internally

on that basis to management; or

− relates to financial instruments containing one or more embedded derivatives that significantly modify the

cash flows resulting from those financial instruments.