HSBC 2005 Annual Report Download - page 164

Download and view the complete annual report

Please find page 164 of the 2005 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

|

|

HSBC HOLDINGS PLC

Financial Review (continued)

162

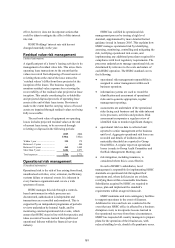

Reputational risk management

(Unaudited information)

The safeguarding of HSBC’s reputation is of

paramount importance to its continued prosperity

and is the responsibility of every member of staff.

Reputational risks can arise from social, ethical or

environmental issues, or as a consequence of

operational risk events. As a banking group, HSBC’s

good reputation depends upon the way in which it

conducts its business, but it can also be affected by

the way in which clients, to whom it provides

financial services, conduct themselves.

Reputational risks are considered and assessed

by the Board, the Group Management Board, the

Risk Management Meeting, subsidiary company

boards, board committees and/or senior management

during the formulation of policy and the

establishment of HSBC standards. Standards on all

major aspects of business are set for HSBC and for

individual subsidiaries, businesses and functions.

These policies, which are an integral part of the

internal control systems, are communicated through

manuals and statements of policy and are

promulgated through internal communications and

training. The policies set out operational procedures

in all areas of reputational risk, including money

laundering deterrence, environmental impact, anti-

corruption measures and employee relations.

Management in all operating entities is required

to establish a strong internal control structure to

minimise the risk of operational and financial failure,

and to ensure that a full appraisal of reputational

implications is made before strategic decisions are

taken. The Group Internal Audit function monitors

compliance with policies and standards.

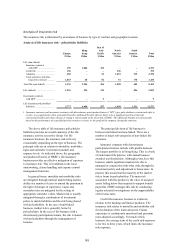

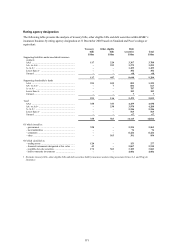

Risk management of insurance

operations

(Forms part of the audited financial statements)

Insurance risk

Within its service proposition, HSBC offers its

personal and commercial customers a wide range of

insurance products, many of which complement

other bank and consumer finance products.

Both life and non-life insurance is underwritten.

Underwriting occurs in nine countries through 27

licensed insurers, principally in the UK, Hong Kong,

Mexico, Brazil, the US and Argentina.

Life insurance contracts include participating

business (with discretionary participation features)

such as endowments and pensions, credit life

business in respect of income and payment

protection, annuities, term assurance and critical

illness covers.

Non-life insurance contracts include motor, fire

and other damage, accident, repayment protection

and a limited amount of commercial and liability

business.

The principal insurance risk faced by HSBC is

that the costs of claims combined with acquisition

and administration costs may exceed the aggregate

amount of premiums received and investment

income. HSBC manages its insurance risks through

the application of formal underwriting, reinsurance

and claims procedures. These procedures are

designed also to ensure compliance with regulations.

The Group’s overall approach to insurance risk

is to maintain a good diversification of insurance

business by type and geography, and to focus on

risks that are straightforward to manage and

frequently are directly related to the underlying

banking activity (for example, with credit life

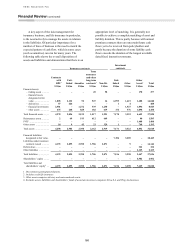

products). The following tables provide an analysis

of the insurance risk exposures by geography and by

type of business. These tables demonstrate the

Group’s diversification of risk and the strong

emphasis on personal lines. Personal lines tend to be

higher volume and with lower individual value than

commercial lines, which further diversifies the risk.

Separate tables are provided for life and non-life

business, reflecting their very distinct risk

characteristics. Life business tends to be longer term

than non-life and also frequently involves an element

of savings and investment in the premium. For this

reason, the life insurance risk table provides an

analysis of the insurance liabilities as the best

available overall measure of the insurance exposure.

By contrast for non-life business, the table uses

written premium as representing the best available

measure of risk exposure.

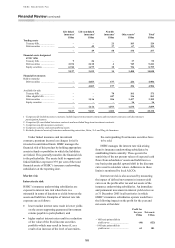

Both life and non-life business insurance risks

are controlled through a combination of local and

central procedures and policies. These include a

centralised approach to the authorisation to write

certain classes of business, with restrictions applying

particularly to commercial and liability non-life

business. For life business in particular, use is also

made of ALCOs in order to monitor the risk

exposures. Market risk limits are also applied

centrally as an additional control over the extent of

insurance risk that is retained.

As indicated in the specific comments relating

to particular classes, use is also made of reinsurance

as a means of further mitigating exposure, in

particular to aggregations as a result of catastrophe

risk.