HSBC 2005 Annual Report Download - page 78

Download and view the complete annual report

Please find page 78 of the 2005 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

|

|

HSBC HOLDINGS PLC

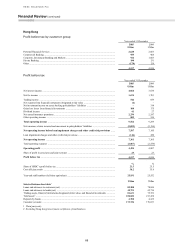

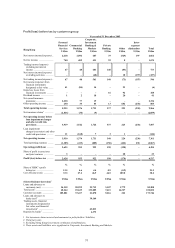

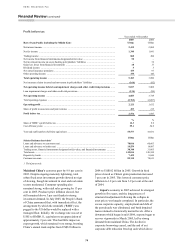

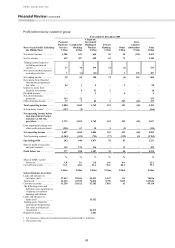

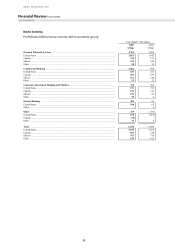

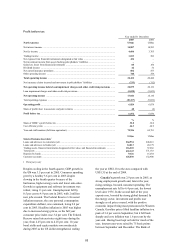

Financial Review (continued)

76

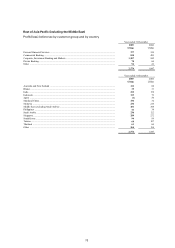

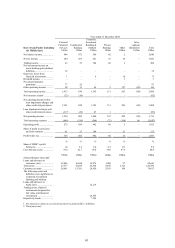

6.3 million, representing an increase of 34 per cent

over 2004. In India, the number of cards in

circulation exceeded one million for the first time.

Higher card balances led to higher net interest

income in Indonesia, India, Taiwan, Malaysia and the

Philippines.

Net fee income grew by 46 per cent to

US$419 million, largely attributable to strong sales

of investment and insurance products, and increased

account service fees. Credit card fee incomes rose,

driven by the strong growth in cardholder spending.

Commissions from sales of unit trusts and funds

under management were particularly strong in

Singapore, India and Taiwan. Sales of investment

products, comprising unit trusts, bonds and structured

notes, grew by 43 per cent to US$6.5 billion,

generating a 56 per cent increase in fee income. The

launch of over 217 tranches of structured notes and

deposit products in 11 countries across the region

achieved total sales of US$952 million. Total funds

under management rose by 33 per cent or

US$7.2 billion, led by increased marketing activity

and the considerable focus placed on wealth

management services during the year. HSBC Bank

Malaysia maintained its position as the leading

international institutional unit trust agent in the

country. Brokerage and custody fees grew,

particularly in Australia, where a 13 per cent rise

reflected increased stock market activity.

HSBC continued to emphasise the expansion of

its insurance business across the region. The number

of policies in force increased by 27 per cent and

revenues grew by 16 per cent.

Loan impairment charges and other credit risk

provisions doubled compared with 2004. This was

due to the non-recurrence of a release of a general

provision in Malaysia in 2004, and a sharp rise in

credit card provisions in Taiwan, reflecting

deteriorating credit conditions. Growth in personal

unsecured lending and credit cards across the region

contributed further to the increased charge.

Operating expenses increased by 29 per cent to

US$1,245 million in support of business growth.

HSBC spent considerable amounts in the region

enhancing its existing infrastructure in order to

benefit fully from the opportunities presented by the

Asian growth economies. Staff costs of

US$469 million rose by 23 per cent, as employee

numbers increased to support business growth and to

increase sales and wealth management activities.

Performance-related remuneration costs were also

higher as a result of the strong growth in profitability.

Marketing costs rose as major campaigns were

run to support product promotions in mortgages,

credit cards, insurance and investment products.

Continued emphasis was placed on brand awareness

in order to generate additional business and reinforce

HSBC’s position as the world’s local bank across the

region, and this further increased costs. Various

growth initiatives required investment in technology,

and the development of new distribution channels

resulted in higher IT costs. Other expenses, including

professional fees and communications costs, rose in

support of business expansion.

Increased contributions from HSBC’s

investments in Bank of Communications and

Industrial Bank in mainland China, together with

record earnings from The Saudi British Bank,

contributed to strong growth in profit from

associates.

Commercial Banking reported a pre-tax profit

of US$818 million, 45 per cent higher than that

delivered in 2004. The increase was mainly due to

higher net interest income as growth in customer

numbers and strong credit demand to fund

infrastructure investment drove balance sheet growth.

Higher contributions from Bank of Communications

and Industrial Bank in China, as well as a strong

performance in The Saudi British Bank, produced

higher income from associates. Lending balances

increased by 16 per cent, exceeded by a 24 per cent

rise in deposits.

Net interest income increased by 33 per cent to

US$631 million, reflecting growth in the Middle

East, Singapore, mainland China, Indonesia and

Taiwan. In the Middle East, strong regional

economies and significant government backed

infrastructure and property projects, principally in the

United Arab Emirates, contributed to a 37 per cent

growth in lending balances and a 42 per cent increase

in customer account balances. Higher trade flows

generated a 25 per cent increase in net interest

income from trade services, while higher interest

rates raised liability spreads by 118 basis points. A

new Amanah term investment product was launched

in May 2005, attracting US$120 million of deposits,

principally from new customers seeking Shariah-

compliant investment opportunities.

In mainland China, strong economic growth,

expansion of the branch network and the recruitment

of additional sales staff resulted in a 39 per cent

increase in lending balances. Deposit balances also

benefited from economic growth, increasing by

38 per cent, while deposit spreads widened by

76 basis points following increases in US interest

rates.

In Singapore, interest rate rises prompted

increased demand for savings products and