HSBC 2005 Annual Report Download - page 132

Download and view the complete annual report

Please find page 132 of the 2005 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

|

|

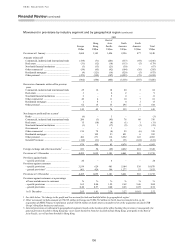

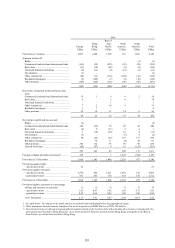

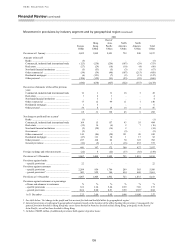

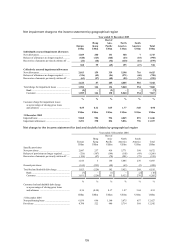

HSBC HOLDINGS PLC

Financial Review (continued)

130

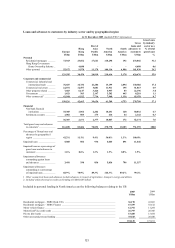

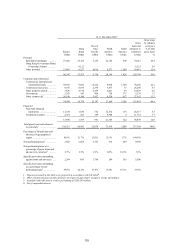

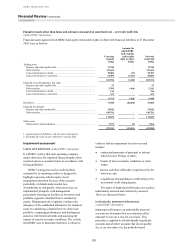

Financial assets other than loans and advances measured at amortised cost – net total credit risk

(Audited IFRS 7 information)

Financial assets against which HSBC had legally enforceable rights to offset with financial liabilities at 31 December

2005 were as follows:

Carrying

amount

Amount for

which HSBC

had a legally

enforceable

right to offset1

Net total

credit risk2

US$m US$m US$m

Trading assets

Treasury and other eligible bills ............................................................... 12,746 –12,746

Debt securities .......................................................................................... 117,659 –117,659

Loans and advances to banks ................................................................... 29,806 (19) 29,787

Loans and advances to customers ............................................................. 52,495 (7,411) 45,084

212,706 (7,430) 205,276

Financial assets designated at fair value

Treasury and other eligible bills ............................................................... 53 –53

Debt securities .......................................................................................... 5,705 (464) 5,241

Loans and advances to banks ................................................................... 124 –124

Loans and advances to customers ............................................................. 631 –631

6,513 (464) 6,049

Derivatives ................................................................................................... 73,928 (46,060) 27,868

Financial investments

Treasury and other similar bills ................................................................ 25,042 –25,042

Debt securities .......................................................................................... 149,781 –149,781

174,823 –174,823

Other assets

Endorsements and acceptances ................................................................. 7,973 (9) 7,964

475,943 (53,963) 421,980

1 Against financial liabilities with the same counterparty.

2Excluding the value of any collateral or security held.

Impairment assessment

Loans and advances (Audited IFRS 7 information)

It is HSBC’s policy that each operating company

makes allowance for impaired loans promptly when

required and on a consistent basis in accordance with

Group guidelines.

HSBC’s rating process for credit facilities

extended by its operating entities is designed to

highlight exposures which require closer

management attention because of their greater

probability of default and potential loss.

Amendments to risk grades, when necessary, are

implemented promptly, with management

particularly focusing on facilities to borrowers and

portfolio segments classified below satisfactory

grades. Management also regularly evaluates the

adequacy of the established allowances for impaired

loans by conducting a detailed review of the loan

portfolio, comparing performance and delinquency

statistics with historical trends and assessing the

impact of current economic conditions. The criteria

that HSBC uses to determine that there is objective

evidence that an impairment loss has occurred

include:

• contractual payments of principal or interest

which become 90 days overdue;

• breach of loan covenants, conditions or other

terms;

• known cash flow difficulties experienced by the

borrower; and

• a significant downgrading in credit rating set by

an external credit rating agency.

Two types of impairment allowance are in place:

individually assessed and collectively assessed.

These are discussed below.

Individually assessed allowances

(Audited IFRS 7 information)

Impairment allowances on individually assessed

accounts are determined by an evaluation of the

exposure to loss on a case-by-case basis. This

procedure is applied to all individually significant

accounts and all other accounts that do not qualify

for, or are not subject to, the portfolio-based