HSBC 2005 Annual Report Download - page 387

Download and view the complete annual report

Please find page 387 of the 2005 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

377 -

378

378 -

379

379 -

380

380 -

381

381 -

382

382 -

383

383 -

384

384 -

385

385 -

386

386 -

387

387 -

388

388 -

389

389 -

390

390 -

391

391 -

392

392 -

393

393 -

394

394 -

395

395 -

396

396 -

397

397 -

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

|

|

385

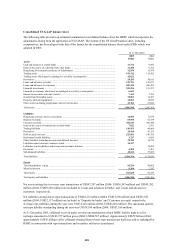

income and shareholders’ equity under US GAAP because, in the years presented, the extra cost deferral under

US GAAP exceeds the amortisation of previously deferred costs.

Securitisations

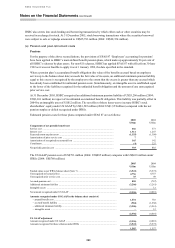

IFRSs

• The recognition of securitised assets is governed by a three-step process, which may be applied to the whole

asset, or a part of an asset:

− If the rights to the cash flows arising from securitised assets have been transferred to a third party, and all

the risks and rewards of the assets have been transferred, the assets concerned are derecognised.

− If the rights to the cash flows are retained by HSBC but there is a contractual obligation to pay them to

another party, the securitised assets concerned are derecognised if certain conditions are met such as, for

example, when there is no obligation to pay amounts to the eventual recipient unless an equivalent amount is

collected from the original asset.

− If some significant risks and rewards of ownership have been transferred, but some have also been retained,

it must be determined whether or not control has been retained. If control has been retained, HSBC

continues to recognise the asset to the extent of its continuing involvement; if not, the asset is derecognised.

US GAAP

• SFAS 140, ‘Accounting for Transfers and Servicing of Finance Assets and Extinguishments of Liabilities’,

requires that receivables that are sold to a special purpose entity (‘SPE’) and securitised can only be

derecognised and a gain or loss on sale recognised if the originator has surrendered control over the securitised

assets.

• Control is surrendered over transferred assets if and only if all of the following conditions are met:

− The transferred assets are put presumptively beyond the reach of the transferor and its creditors, even in

bankruptcy or other receivership.

− Each holder of interests in the transferee (i.e. holder of issued notes) has the right to pledge or exchange

their beneficial interests, and no condition constrains this right and provides more than a trivial benefit to the

transferor.

− The transferor does not maintain effective control over the assets through either an agreement that obligates

the transferor to repurchase or to redeem them before their maturity, or through the ability to unilaterally

cause the holder to return specific assets other than through a clean-up call.

• If these conditions are not met the securitised assets continue to be consolidated.

• When HSBC retains an interest in securitised assets, such as a servicing right or the right to residual cash flows

from the special purpose entity, HSBC recognises this interest at fair value on sale of the assets to the SPE.

Impact

• Gains on sale of assets to securitisation vehicles are recognised under US GAAP in cases when no such gain is

recognised under IFRSs. This results in higher US GAAP net income in periods in which there is significant

securitisation activity. Since early 2004, HSBC has reduced securitisation activity that results in ‘gain on sale’

accounting under US GAAP. As a result, net income is lower under US GAAP because the amortisation of

HSBC’s retained interest in previous securitisations exceeds the gains on new transactions where a gain is

recognised. The new transactions largely replenish short-term loan assets held by existing vehicles.

Consolidation of Special Purpose Entities or Variable Interest Entities

IFRSs

• Under the IASB’s Standards Interpretations Committee (‘SIC’) Interpretation 12 (‘SIC-12’), an SPE should be

consolidated when the substance of the relationship between an enterprise and the SPE indicates that the SPE is

controlled by that entity.