HSBC 2005 Annual Report Download - page 143

Download and view the complete annual report

Please find page 143 of the 2005 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

|

|

141

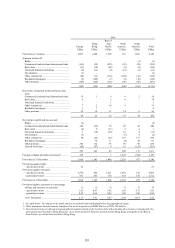

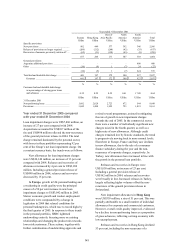

Year ended 31 December 2001

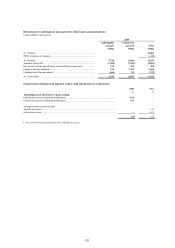

Europe

US$m

Hong Kong

US$m

Rest of

Asia-Pacific

US$m

North

America

US$m

South

America

US$m

Total

US$m

Specific provisions

New provisions ................................................... 802 449 577 392 346 2,566

Release of provisions no longer required ............ (260) (212) (268) (42) (35) (817)

Recoveries of amounts previously written off .... (65) (31) (138) (43) (8) (285)

477 206 171 307 303 1,464

General provisions

Argentine additional provision ........................... ––––600 600

Other .................................................................. (36) (9) 1 (7) 24 (27)

(36) (9) 1 (7) 624 573

Total bad and doubtful debt charge .................... 441 197 172 300 927 2,037

Customer ........................................................ 441 197 172 300 927 2,037

%%%%%%

Customer bad and doubtful debt charge

as a percentage of closing gross loans

and advances ................................................. 0.32 0.29 0.52 0.41 17.80 0.64

US$m US$m US$m US$m US$m US$m

31 December 2001

Non-performing loans ........................................ 3,682 2,028 2,723 672 544 9,649

Provisions ........................................................... 3,045 1,408 1,952 723 1,033 8,161

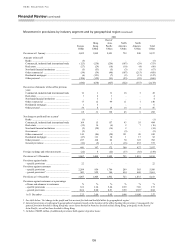

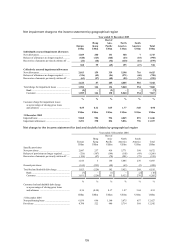

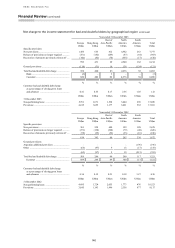

Year ended 31 December 2005 compared

with year ended 31 December 2004

Loan impairment charges were US$7,860 million, an

increase of 27 per cent compared with 2004.

Acquisitions accounted for US$107 million of the

rise and US$498 million reflected the non-recurrence

of the general provision release in 2004. The total

charge remained dominated by the personal sector,

with losses in these portfolios representing 92 per

cent of the Group’s net loan impairment charge. On

a constant currency basis, the trends were as follows:

New allowances for loan impairment charges

were US$10,140 million, an increase of 13 per cent

compared with 2004. Releases and recoveries of

allowances increased by 4 per cent to US$2,280

million. Including a general provision release of

US$498 million in 2004, releases and recoveries

decreased by 15 per cent.

In Europe, growth in UK personal lending and

a weakening in credit quality were the principal

causes of a 50 per cent increase in new loan

impairment charges to US$3,042 million in 2005.

Slower economic growth and weaker employment

conditions were compounded by a change in

legislation in 2004 that relaxed conditions for

personal bankruptcies, which rose to record highs by

the final quarter of 2005. In response to these trends

in the personal portfolio, HSBC tightened

underwriting controls, focusing more on existing

relationships and changing the product mix towards

lower risk customers. These actions, together with

further centralisation of underwriting approvals and

revised reward programmes, assisted in mitigating

the rate of growth in new impairment charges

towards the end of 2005. In the commercial sector,

there were a number of individually significant new

charges raised in the fourth quarter, as well as a

higher rate of new allowances. Although credit

charges remained low by historic standards, the trend

is progressively moving back to more normal levels.

Elsewhere in Europe, France and Italy saw declines

in new allowances, due to the sale of a consumer

finance subsidiary during the year and the non-

recurrence of corporate charges, respectively. In

Turkey, new allowances have increased in line with

the growth in the personal loan portfolio.

Releases and recoveries in Europe were

US$1,058 million, an increase of 23 per cent.

Including a general provision release of

US$162 million in 2004, releases and recoveries

were broadly in line. Increased releases in Turkey,

largely reflecting higher volumes offset the non-

recurrence of the general provision release in

Switzerland.

New impairment allowances in Hong Kong

were US$359 million, a rise of 51 per cent. This was

partially attributable to a small number of individual

allowances for corporate and commercial customers.

However, overall credit quality improved, evidenced

by a decline in non-performing loans as a proportion

of gross advances, reflecting a strong economy with

low unemployment.

Releases and recoveries in Hong Kong declined

53 per cent, including the non-recurrence of a