HSBC 2005 Annual Report Download - page 119

Download and view the complete annual report

Please find page 119 of the 2005 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

|

|

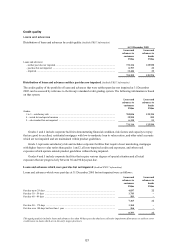

117

subsidiary, management includes a Chief Credit and

Risk Officer who reports to the local Chief

Executive Officer on credit-related issues. All Chief

Credit and Risk Officers have a functional reporting

line to the Group General Manager, Group Credit

and Risk. Each operating company is responsible for

the quality and performance of its credit portfolios

and for monitoring and controlling all credit risks in

its portfolios, including those subject to central

approval by Group Credit and Risk. This includes

managing its own risk concentrations by market

sector, geography and product. Local systems are in

place throughout the Group to enable operating

companies to control and monitor exposures by

customer and counterparty.

Special attention is paid to problem loans. When

appropriate, specialist units are established by

HSBC’s operating companies to provide customers

with support in order to help them avoid default

wherever possible, thereby maximising recoveries

for HSBC.

Regular audits of operating companies’ credit

processes are undertaken by HSBC’s Internal Audit

function. Audits include a consideration of the

completeness and adequacy of credit manuals and

lending guidelines; an in-depth analysis of a

representative sample of accounts; an overview of

homogeneous portfolios of similar assets to assess

the quality of the loan book and other exposures; and

a check that Group standards and policies are

adhered to in the extension and management of

credit facilities. Individual accounts are reviewed to

ensure that risk grades are appropriate, that credit

and collection procedures have been properly

followed and that, when an account or portfolio

evidences deterioration, impairment allowances are

raised in accordance with the Group’s established

processes. Internal Audit discuss with management

risk ratings they consider to be inappropriate, and

their subsequent recommendations for revised grades

must then be assigned to the facilities concerned.

Collateral and other credit enhancements

Loans and advances (Audited IFRS 7 information)

When appropriate, operating companies are required

to implement guidelines on the acceptability of

specific classes of collateral or credit risk mitigation,

and determine valuation parameters. Such

parameters are expected to be conservative,

reviewed regularly and supported by empirical

evidence. Security structures and legal covenants are

subject to regular review to ensure that they continue

to fulfil their intended purpose and remain in line

with local market practice. While collateral is an

important mitigant to credit risk, it is HSBC’s policy

to establish that loans are within the customer’s

capacity to repay rather than to rely excessively on

security. In certain cases, depending on the

customer’s standing and the type of product,

facilities may be unsecured. The principal collateral

types are as follows:

• in the personal sector, mortgages over

residential properties;

• in the commercial and industrial sector, charges

over business assets such as premises, stock and

debtors;

• in the commercial real estate sector, charges

over the properties being financed; and

• in the financial sector, charges over financial

instruments such as debt securities and equities

in support of trading facilities.

Other securities (Audited IFRS 7 information)

Collateral held as security for financial assets other

than loans and advances is determined by the nature

of the instrument. Debt securities, treasury and other

eligible bills are generally unsecured with the

exception of asset backed securities and similar

instruments, which are secured by pools of financial

assets.

The ISDA Master Agreement is HSBC’s

preferred agreement for documenting derivatives

activity. It provides the contractual framework

within which dealing activity across a full range of

over-the-counter (‘OTC’), products is conducted and

contractually binds both parties to apply close-out

netting across all outstanding transactions covered

by an agreement, if either party defaults or following

other pre-agreed termination events. It is common

for the parties to execute a Credit Support Annex

(‘CSA’) in conjunction with the ISDA Master

Agreement, a practice HSBC encourages. Under a

CSA, collateral is passed between the parties to

mitigate the market contingent counterparty risk

inherent in the outstanding positions.

Settlement risk arises in any situation where a

payment in cash, securities or equities is made in the

expectation of a corresponding receipt in cash,

securities or equities. Daily Settlement Limits are

established for each counterparty, to cover the

aggregate of all settlement risk arising from HSBC’s

investment banking and markets transactions on any

single day. Settlement risk on many transactions,

particularly those involving securities and equities, is

substantially mitigated when effected via Assured

Payment Systems, or on a delivery versus payment

basis.