HSBC 2005 Annual Report Download - page 365

Download and view the complete annual report

Please find page 365 of the 2005 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

355 -

356

356 -

357

357 -

358

358 -

359

359 -

360

360 -

361

361 -

362

362 -

363

363 -

364

364 -

365

365 -

366

366 -

367

367 -

368

368 -

369

369 -

370

370 -

371

371 -

372

372 -

373

373 -

374

374 -

375

375 -

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

|

|

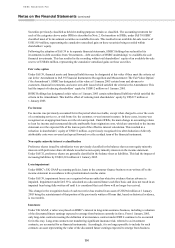

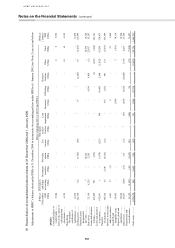

363

− historical loss experience in portfolios of similar risk characteristics (for example, by industry sector, loan

grade or product);

− the estimated period between impairment occurring and the loss being identified and evidenced by the

establishment of a specific provision against that loss; and

− management’s judgement as to whether the then economic and credit conditions were such that the actual

level of inherent loss was likely to be greater or less than that suggested by historical experience.

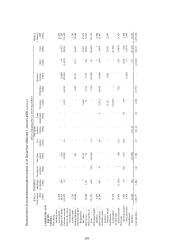

The estimated period between a loss occurring and its identification (as evidenced by the establishment of a

specific provision for that loss) was determined by local management for each identified portfolio.

Loans on which interest was being suspended and non-accrual loans

Loans were designated as non-performing as soon as management had doubts as to the ultimate collectibility of

principal or interest or when contractual payments of principal or interest were 90 days overdue. When a loan

was designated as non-performing, interest was not normally credited to the income statement and either interest

accruals ceased (‘non-accrual loans’) or interest was credited to an interest suspense account in the balance sheet

which was netted against the relevant loan (‘suspended interest’).

Within portfolios of low value, high volume, homogeneous loans, interest was normally suspended on facilities

90 days or more overdue. In certain operating subsidiaries, interest income on credit cards may have continued to

be included in earnings after the account was 90 days overdue, provided that a suitable provision was raised

against the portion of accrued interest which was considered to be irrecoverable.

The designation of a loan as non-performing and the suspension of interest could be deferred for up to 12 months

in either of the following situations:

− cash collateral was held covering the total of principal and interest due and the right of offset was legally

sound; or

− the value of any net realisable tangible security was considered more than sufficient to cover the full

repayment of all principal and interest due, and credit approval had been given to the rolling-up or

capitalisation of interest payments.

In certain subsidiaries, principally those in the UK and Hong Kong, interest on non-performing loans was

charged to the customer’s account provided that there was a realistic prospect of interest being paid at some

future date. However, the interest was not credited to the income statement but to an interest suspense account in

the balance sheet, which was netted against the relevant loan.

In other subsidiaries, when the probability of receiving interest payments was remote, interest was no longer

accrued and any suspended interest balance was written off.

On receipt of cash (other than from the realisation of security), the overall risk was re-evaluated and, if

appropriate, suspended or non-accrual interest was recovered and taken to the income statement. A specific

provision of the same amount as the interest receipt was then raised against the principal balance. Amounts

received from the realisation of security were applied to the repayment of outstanding indebtedness, with any

surplus used first to recover any specific provisions and then suspended interest.

Loans were not reclassified as accruing until interest and principal payments were up to date and future

payments were reasonably assured.

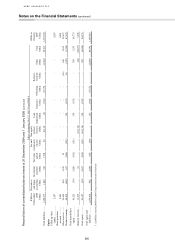

Loan write-offs

Loans (and the related provisions) were normally written off, either partially or in full, when there was no

realistic prospect of recovery of these amounts and when the proceeds from realising security had been received.

Trading assets and trading liabilities

Treasury bills, debt securities, equity shares and short positions in securities were included in ‘Trading assets’ or

‘Trading liabilities’ in the balance sheet at market value. Changes in the market value of these assets and

liabilities were recognised in the income statement as ‘Trading income’ as they arose. For liquid portfolios,

market values were determined by reference to independently sourced mid-market prices. In certain less liquid