HSBC 2005 Annual Report Download - page 171

Download and view the complete annual report

Please find page 171 of the 2005 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

176 -

177

177 -

178

178 -

179

179 -

180

180 -

181

181 -

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

|

|

169

The interest rate sensitivities set out above are

illustrative only and employ simplified scenarios.

They are based on US$8,068 million of interest-

bearing securities held by insurance underwriting

subsidiaries at 31 December 2005 and

US$3,350 million of insurance liabilities under

insurance contracts and long-term investment

contracts issued. The sensitivities do not incorporate

actions that could be taken by management to

mitigate the effect of the interest rate movements,

nor do they take account of consequential changes in

policyholder behaviour.

The majority of interest rate exposure arises

within insurance underwriting subsidiaries in the

UK, the US and Hong Kong.

HSBC’s insurance underwriting subsidiaries are

also exposed to the risk that the yield on assets held

may fall short of the return guaranteed on certain

contracts issued to policyholders. This investment

return guarantee risk is managed by matching assets

held to liability requirements. In addition, a

provision is established when analysis indicates that,

over the life of the contracts, the returns from the

designated assets may not be adequate to cover the

related liabilities.

The guarantees offered to policyholders in

respect of certain insurance products are divided into

broad categories as follows:

• annuities in payment;

• deferred annuities: these consist of two phases –

the savings and investing phase, and the

retirement income phase;

• annual return: the investment return credited to

the policyholder every year (referred to as a

‘hard’ guarantee), or the average annual

investment return credited to the policyholder

over the life of the policy to its maturity or

surrender (referred to as a ‘soft’ guarantee) is

guaranteed to be no lower than a specified rate;

• capital: policyholders are guaranteed to receive

back no less than the premiums paid less

expenses, or a cash payment or series of cash

payments whose amounts are at least equal to

those defined within the policy; and

• market performance: policyholders receive an

investment return which is guaranteed to be

within a prescribed range of average investment

returns earned by predetermined market

participants on the specified product.

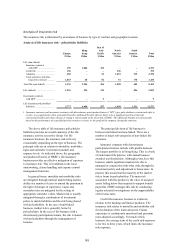

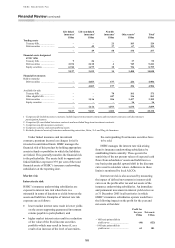

The table below shows, in respect of each

category of guarantee, the total reserves established

for guaranteed products, the range of investment

returns implied by the guarantees, and the range of

current yields of the investment portfolios supporting

the guarantees.

Reserve

Investment

returns implied

by guarantee1Current yields

US$m % %

Annuities in payment .................................................................................... 1,063 0.0 – 4.2% 4.0 – 13.0%

Deferred annuities ........................................................................................ 408 0.0 – 6.0% 6.1 – 8.6%

Deferred annuities ........................................................................................ 674 6.0 – 9.0% 5.7%

Annual return ............................................................................................... 4,362 0.0 – 3.0% 3.5 – 5.6%

Annual return ............................................................................................... 581 3.0 – 6.0% 3.5 – 11.5%

Capital .......................................................................................................... 1,168 0.0% 2.9 – 5.6%

Market performance2 .................................................................................... 2,938 n/a n/a

1The above table excludes guarantees from associate insurance companies Erisa, S.A. and Ping An Insurance.

2There is no specific investment return implied by market performance guarantees because the guarantees are expressed as lying within

prescribed ranges of average market returns.

The Group manages the annuities, annual return

and capital guarantees by seeking to match the

exposure predominantly with bonds which are

producing a return at least equal to the investment

return implied by the guarantee. Provision is made

for any anticipated shortfall, generally calculated by

recourse to stress testing of the likely outcomes.

The main risk arising from these guarantees is

reinvestment risk, which arises primarily when the

duration of the policy extends beyond the maturity

dates of the bonds. Future reinvestment yields may

be less than the investment rates implied by the

guarantee.

A certain number of these products have been

discontinued to new business; this includes the

deferred annuity portfolio in HSBC Finance, where

the current portfolio yield is less than the guarantee

and highlighted in the above table. For this block of

business, a purchase accounting reserve was made at

the time of the acquisition of HSBC Finance to

mitigate the impact of the disparity in yields. In