HSBC 2005 Annual Report Download - page 160

Download and view the complete annual report

Please find page 160 of the 2005 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

|

|

HSBC HOLDINGS PLC

Financial Review (continued)

158

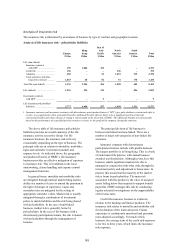

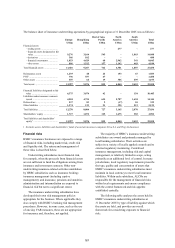

US dollar

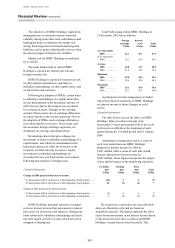

bloc

US$m

Rest of

Americas

bloc

US$m

Hong Kong

dollar

bloc

US$m

Rest of

Asia

bloc

US$m

Sterling

bloc

US$m

Euro

bloc

US$m

Total

US$m

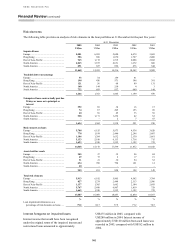

Change in 2006 projected net

interest income

+25 basis points shift in yield curves

at the beginning of each quarter. (448) 74 (18) 28 (47) (114) (525)

-25 basis points shift in yield curves

at the beginning of each quarter. 402 (72) 20 (39) 51 112 474

Change in 2005 projected net

interest income

+25 basis points shift in yield curves

at the beginning of each quarter. (500) 81 2 18 62 (160) (497)

-25 basis points shift in yield curves

at the beginning of each quarter. 637 (83) (104) (13) (70) 157 524

The interest rate sensitivities set out in the table

above are illustrative only and are based on

simplified scenarios. The figures represent the effect

of the pro forma movements in net interest income

based on the projected yield curve scenarios and the

Group’s current interest rate risk profile. This effect,

however, does not incorporate actions that would be

taken by Global Markets or in the business units to

mitigate the impact of this interest rate risk. In

reality, Global Markets seeks proactively to change

the interest rate risk profile to minimise losses and

optimise net revenues. The projections above also

assume that interest rates of all maturities move by

the same amount and, therefore, do not reflect the

potential impact on net interest income of some rates

changing while others remain unchanged. The

projections also make other simplifying assumptions,

including that all positions run to maturity.

The Group’s core exposure to changes in its net

interest income arising from movements in interest

rates falls into three areas: core deposit franchises,

HSBC Finance and Global Markets.

• Core deposit franchises: these are exposed to

changes in the value of the deposits raised and

spreads against wholesale funds; in a low

interest rate environment, the value of core

deposits increases as interest rates rise and

decreases as interest rates fall. This risk is,

however, asymmetrical in a very low interest

rate environment as there is limited room to

lower deposit pricing in the event of interest rate

reductions.

• HSBC Finance provides an offset to the

sensitivity effect of interest rate reductions on

the core deposit franchises. This arises from

having a substantially fixed rate, real estate

secured, lending portfolio funded to an extent

with interest rate sensitive short-term liabilities.

• Global Markets: the residual interest rate risk is

managed within Global Markets. This reflects

the Group’s policy of transferring all interest

rate risk, other than structural risk, to Global

Markets to be managed within defined limits

and with flexibility as to the instruments used.

The major drivers of the changes shown in the

projected effect of interest rate moves in the above

table are set out below.

• In the US dollar bloc, the rise in interest rates in

2005, coupled with an overall flattening of the

yield curve, led the Group to reduce its

sensitivity to falling rates, particularly with

respect to some retail products with embedded

optionality.

• In Hong Kong, the rise in interest rates during

the year improved the sensitivity to falling

interest rates as there was more room to lower

deposit pricing in the event of falling interest

rates.

• Global Markets decreased its exposure to US

dollar, Hong Kong dollar, and euro assets,

contributing to the decreased sensitivity in these

currencies to both rising and falling rates.

It can be seen from the above that projecting the

movement in net interest income from prospective

changes in interest rates is a complex interaction of

structural and managed exposures. In a rising rate

environment, the most critical exposures are those

managed within Global Markets.

Additionally, the Group considers a principal

risk to future net interest income to be a general

flattening of yield curves at a low level of interest

rates, as this reduces the value of the deposit

franchise and limits the opportunities within Global

Markets.