HSBC 2005 Annual Report Download - page 379

Download and view the complete annual report

Please find page 379 of the 2005 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

369 -

370

370 -

371

371 -

372

372 -

373

373 -

374

374 -

375

375 -

376

376 -

377

377 -

378

378 -

379

379 -

380

380 -

381

381 -

382

382 -

383

383 -

384

384 -

385

385 -

386

386 -

387

387 -

388

388 -

389

389 -

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

|

|

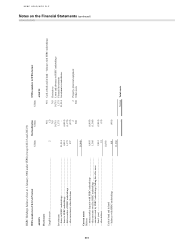

377

were expensed in the years for which they were granted. 2005 bonuses will be expensed over the vesting period

under both IFRSs and US GAAP. Net income was, therefore, higher under US GAAP in 2005.

• IFRSs and US GAAP are now largely aligned and this transition difference will be eliminated over the next few

years.

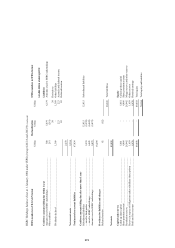

Goodwill, purchase accounting and intangible assets

IFRSs

• Prior to 1998, goodwill under UK GAAP was written off against equity. HSBC did not elect to reinstate this

goodwill on its balance sheet upon transition to IFRSs. From 1 January 1998 to 31 December 2003, goodwill

was capitalised and amortised over its useful life. The carrying amount of goodwill existing at 31 December

2003 under UK GAAP was carried forward under the transition rules of IFRS 1 from 1 January 2004, subject to

certain adjustments.

• IFRS 3 ‘Business Combinations’ requires that goodwill should not be amortised but should be tested for

impairment at least annually at the reporting unit level by applying a test based on recoverable amounts.

• Quoted securities issued as part of the purchase consideration are valued for the purpose of determining the cost

of the acquisition at their market price on the date the transaction is completed.

US GAAP

• Up to 30 June 2001, goodwill acquired was capitalised and amortised over its useful life, which could not exceed

25 years. The amortisation of previously acquired goodwill ceased with effect from 31 December 2001.

• Quoted securities issued as part of the purchase consideration are fair valued for the purpose of determining the

cost of acquisition at their average market price over a reasonable period before and after the date on which the

terms of the acquisition are agreed and announced.

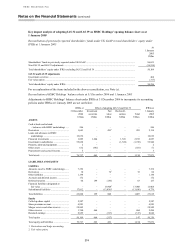

Impact

• Total goodwill and shareholders’ equity are both higher under US GAAP than under IFRSs because, under US

GAAP, (i) pre-1998 goodwill is included on the balance sheet and (ii) the amortisation of goodwill ceased on

31 December 2001 compared with 31 December 2003 under IFRSs.

• However, goodwill on the acquisition of HSBC Finance in March 2003 is lower under US GAAP than under

IFRSs. This is principally the result of differences in the accounting for securitisations and intangibles. Under

IFRSs, previously recognised gains on the sale of assets to securitisation vehicles are eliminated and the

securitised assets are recognised on balance sheet. However, because HSBC elected not to restate business

combinations prior to 1 January 2004 on transition to IFRSs, a significant amount of intangible assets arising on

acquisition were not recognised for IFRSs purposes. Under US GAAP, recognition of these assets was required.

• Offsetting this was the recognition of a deferred tax liability under US GAAP in respect of these intangibles and

gains on sale of securitised assets.

• The effect of these items was further offset by the higher value under US GAAP of HSBC shares issued as part

of the purchase consideration. The HSBC share price fell between the time of the announcement of the

acquisition in November 2002 and its completion in March 2003, so the average price under US GAAP

exceeded the price on the date of acquisition under IFRSs.

Property

IFRSs

• Under the transition rules of IFRS 1, HSBC elected to freeze the value of all its properties held for its own use at

their 1 January 2004 valuations, their ‘deemed cost’ under IFRSs. They will not be revalued in the future. Assets

held at historical or deemed cost are depreciated except for freehold land.

• Investment properties are carried at current market values with gains or losses thereon recognised in net income

for the period. Investment properties are not depreciated.