Advance Auto Parts 2009 Annual Report Download - page 104

Download and view the complete annual report

Please find page 104 of the 2009 Advance Auto Parts annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112

|

|

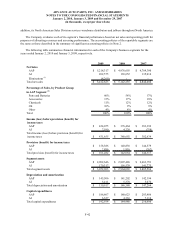

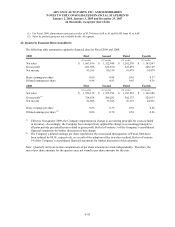

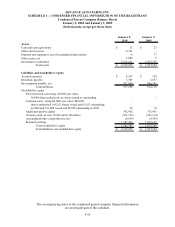

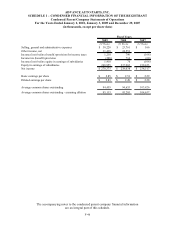

ADVANCE AUTO PARTS, INC.

SCHEDULE I – CONDENSED FINANCIAL INFORMATION OF THE REGISTRANT

Notes to the Condensed Parent Company Statements

January 2, 2010 and January 3, 2009

(in thousands, except per share data)

See Notes to the Consolidated Financial Statements for Additional Disclosures.

F-51

all activity through March 2, 2010 (the issuance date of the financial statements) and concluded that no subsequent

events have occurred, other than the Company’s subsequent repurchase of its common stock, that would require

recognition in the consolidated financial statements or disclosure in the related notes to the consolidated financial

statements.

In June 2008, the FASB Issued EITF No. 08-3, “Accounting by Lessees for Nonrefundable Maintenance

Deposits” (currently ASC Topic 840). EITF 08-3 requires that nonrefundable maintenance deposits paid by a lessee

under an arrangement accounted for as a lease be accounted for as a deposit asset until the underlying maintenance

is performed. When the underlying maintenance is performed, the deposit may be expensed or capitalized in

accordance with the lessee’s maintenance accounting policy. Upon adoption entities must recognize the effect of the

change as a change in accounting principle. The adoption of EITF 08-3 had no impact on the Company’s

consolidated financial statements.

In April 2008, the FASB issued FASB Staff Position No. FAS 142-3, “Determination of the Useful Life

of Intangible Assets” (currently ASC Topic 350), which amends the factors that must be considered in developing

renewal or extension assumptions used to determine the useful life over which to amortize the cost of a recognized

intangible asset under SFAS 142, “Goodwill and Other Intangible Assets.” The FSP requires an entity to consider its

own assumptions about renewal or extension of the term of the arrangement, consistent with its expected use of the

asset, and is an attempt to improve consistency between the useful life of a recognized intangible asset under SFAS

142 and the period of expected cash flows used to measure the fair value of the asset under SFAS 141, “Business

Combinations” (collectively now under ASC Topic 805). The Company adopted the provisions of FSP FAS 142-3

effective January 4, 2009. The adoption of the FSP had no impact on the Company’s consolidated financial

statements.

In December 2007, the FASB issued SFAS No. 141R, “Business Combinations” (collectively now under ASC

Topic 805), which replaces SFAS No. 141, “Business Combinations.” SFAS No. 141R, among other things,

establishes principles and requirements for how an acquirer entity recognizes and measures in its financial

statements the identifiable assets acquired, the liabilities assumed and any controlling interests in the acquired entity;

recognizes and measures the goodwill acquired in the business combination or a gain from a bargain purchase; and

determines what information to disclose to enable users of the financial statements to evaluate the nature and

financial effects of the business combination. Costs of the acquisition will be recognized separately from the

business combination. SFAS No. 141R applies to business combinations for fiscal years beginning after December

15, 2008. The Company will consider this standard when evaluating potential future transactions to which it would

apply.

In December 2009, the FASB issued ASU No. 2009-16, “Transfers and Servicing (Topic 860) Accounting for

Transfers of Financial Assets,” which amends the ASC for the issuance of SFAS No. 166, “Accounting for Transfers

of Financial Assets – an amendment of FASB Statement No. 140.” The amendments in this ASU clarifies the

requirements for isolation and limitations on portions of financial assets that are eligible for sale accounting and

requires enhanced disclosures about the risks that a transferor continues to be exposed to because of its continuing

involvement in transferred financial assets. ASU 2009-16 is effective for the Company’s fiscal year beginning after

November 15, 2009. The Company does not expect the adoption to have a material impact on its consolidated

financial statements.