Advance Auto Parts 2009 Annual Report Download - page 103

Download and view the complete annual report

Please find page 103 of the 2009 Advance Auto Parts annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112

|

|

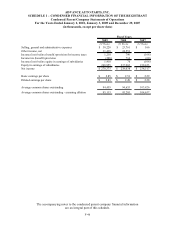

ADVANCE AUTO PARTS, INC.

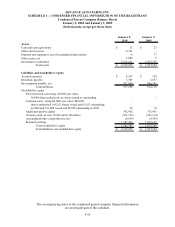

SCHEDULE I – CONDENSED FINANCIAL INFORMATION OF THE REGISTRANT

Notes to the Condensed Parent Company Statements

January 2, 2010 and January 3, 2009

(in thousands, except per share data)

See Notes to the Consolidated Financial Statements for Additional Disclosures.

F-50

New Accounting Pronouncements

In June 2009, the Financial Accounting Standards Board, or FASB, approved the FASB Accounting Standards

Codification, or ASC, as the single source of authoritative nongovernmental GAAP. All existing accounting standard

guidance issued by the FASB, American Institute of Certified Public Accountants, Emerging Issues Task Force and

related literature, excluding guidance from the Securities and Exchange Commission, or SEC, has been superseded

by the ASC. All other non-grandfathered, non-SEC accounting literature not included in the ASC has become non-

authoritative. The ASC did not change GAAP, but instead introduced a new structure that combines all authoritative

standards into a comprehensive, topically organized online database. The ASC was effective for interim or annual

periods ending after September 15, 2009.

Accordingly, the Company adopted the ASC as of October 10, 2009 as provided by Accounting Standards

Update, or ASU, No. 2009-01, “Topic 105 – Generally Accepted Accounting Principles – amendments based on

Statement of Financial Accounting Standards No. 168, The FASB Accounting Standards Codification TM and the

Hierarchy of Generally Accepted Accounting Principles.” As a result of this adoption, previous references to new

accounting standards and literature are no longer applicable. In the current quarter financial statements, the

Company has provided references to both new and old guidance to assist in understanding the impacts of recently

adopted accounting literature, particularly for guidance adopted since the beginning of the current fiscal year but

prior to the ASC.

Effective October 10, 2009, the Company adopted ASU No. 2009-05, “Fair Value Measurements and

Disclosures (ASC Topic 820): Measuring Liabilities at Fair Value.” This ASU provides amendments to ASC Topic

820-10, “Fair Value Measurements and Disclosures – Overall,” for the fair value measurement of liabilities. It

provides clarification that in circumstances in which a quoted price in an active market for the identical liability is

not available, a reporting entity is required to measure fair value using (a) a valuation technique that uses the quoted

price of the identical liability when traded as an asset or quoted prices for similar liabilities and/or (b) an income

approach valuation technique or a market approach valuation technique, consistent with the principles of ASC Topic

820. The adoption did not have a significant impact on the Company’s consolidated financial statements.

Effective July 18, 2009 (the Company’s second quarter), the Company adopted FSP No. FAS 157-4,

“Determining Fair Value When the Volume and Level of Activity for the Asset or Liability Have Significantly

Decreased and Identifying Transactions That Are Not Orderly” (currently included in ASC Topic 820-10-65-4).

This FSP provides guidance for estimating the fair value of an asset or liability when the volume and level of

activity for the asset or liability have significantly decreased, as well as guidance on identifying circumstances that

indicate a transaction is not orderly. It also requires disclosure in interim and annual periods of the inputs and

valuation techniques used to measure fair value and a discussion of changes in valuation techniques and related

inputs, if any, during the period. The adoption had no significant impact on the Company’s consolidated financial

statements.

Effective July 18, 2009 (the Company’s second quarter), the Company adopted FSP No. FAS 107-1 and

APB 28-1, “Interim Disclosures about Fair Value of Financial Instruments” (currently included in ASC Topic 825-

10-65-1). This FSP amends SFAS No. 107, “Disclosures about Fair Value of Financial Instruments,” to require

disclosures about fair value of financial instruments for interim reporting periods as well as in annual financial

statements. This FSP also requires disclosure about the methods and significant assumptions used to estimate the fair

value of financial instruments and changes in those methods and significant assumptions, if any, during the period.

The adoption had no impact on the Company’s consolidated financial statements other than the additional

disclosures.

Effective July 18, 2009 (the Company’s second quarter), the Company adopted SFAS No. 165, “Subsequent

Events” (currently ASC Topic 855-10). This statement sets forth general standards of accounting for and disclosure

of events that occur after the balance sheet date but before financial statements are issued. The Company evaluated