AT&T Wireless 2006 Annual Report Download - page 69

Download and view the complete annual report

Please find page 69 of the 2006 AT&T Wireless annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

|

|

2006 AT&T Annual Report : :

67

In subsequent periods, net periodic pension and postemploy-

ment cost for BellSouth, BellSouth’s 40% economic interest in

AT&T Mobility and ATTC will exclude any amortization of either

the unrecognized loss or the unrecognized prior service cost

existing at the date of the merger. However, the funding of

these plans is not directly affected by the mergers. The basis

of funding, over time, will reflect the past amendments and

losses that underlie those amounts. As they are reflected in

the funding process, contributions will, in some periods,

exceed the net pension cost, and that will reduce the liability

(unfunded accrued pension cost) recognized at the date of

acquisition.

Pension Benefits

Substantially all of our U.S. employees are covered by one of

our noncontributory pension and death benefit plans. Many of

our management employees participate in pension plans that

have a traditional pension formula (i.e., a stated percentage

of employees’ adjusted career income) and a frozen cash

balance or defined lump sum formula. Effective January 15,

2005, the management pension plan for those employees was

amended to freeze benefit accruals previously earned under a

cash balance formula. Each employee’s existing cash balance

continues to earn interest at a variable annual rate. After this

change, those management employees, at retirement, may

elect to receive the portion of their pension benefit derived

under the cash balance or defined lump sum as a lump sum

or an annuity. The remaining pension benefit, if any, will be

paid as an annuity if its value exceeds a stated monthly

amount. ATTC, BellSouth and AT&T Mobility management

employees participate in cash balance pension plans. Non-

management employees’ pension benefits are generally

calculated using one of two formulas; benefits are based on a

flat dollar amount per year according to job classification or

are calculated under a cash balance plan that is based on an

initial cash balance amount and a negotiated, annual pension

band and interest credits. Most nonmanagement employees

can elect to receive their pension benefits in either a lump

sum payment or an annuity.

At December 31, 2006, certain defined pension plans

formerly sponsored by ATTC and AT&T Mobility were merged

in to the AT&T Pension Benefit Plan.

Postretirement Benefits

We provide certain medical, dental and life insurance benefits

to certain retired employees under various plans and accrue

actuarially determined postretirement benefit costs as active

employees earn these benefits.

Obligations and Funded Status

For defined benefit pension plans, the benefit obligation is the

“projected benefit obligation,” the actuarial present value, as

of the measurement date, of all benefits attributed by the

pension benefit formula to employee service rendered to that

date. The amount of benefit to be paid depends on a number

of future events incorporated into the pension benefit formula,

including estimates of the average life of employees/survivors

and average years of service rendered. It is measured based

on assumptions concerning future interest rates and future

employee compensation levels.

For postretirement benefit plans, the benefit obligation is

the “accumulated postretirement benefit obligation,” the

actuarial present value as of a date of all future benefits

attributed under the terms of the postretirement benefit plan

to employee service rendered to that date.

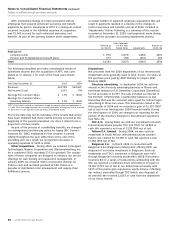

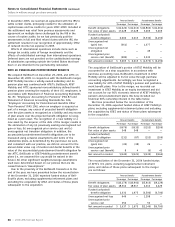

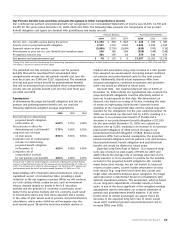

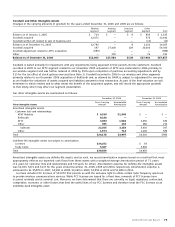

The following table presents this reconciliation and shows the change in the projected benefit obligation for the years ended

December 31:

Pension Benefits Postretirement Benefits

2006 2005 2006 2005

Benefit obligation at beginning of year $46,176 $28,189 $35,225 $25,114

Service cost – benefits earned during the period 1,050 804 435 390

Interest cost on projected benefit obligation 2,507 1,725 1,943 1,496

Amendments — (2) — (442)

Actuarial loss (gain) (1,499) 1,182 (3,386) 613

Special termination benefits 25 15 2 2

Curtailments — — — (77)

Benefits paid (3,958) (2,679) (1,772) (1,234)

Transferred from AT&T Mobility 635 — 209 —

Transferred from BellSouth 11,013 — 11,461 —

Transferred from ATTC — 16,942 — 9,129

Other — — 20 234

Benefit obligation at end of year $55,949 $46,176 $44,137 $35,225