AT&T Wireless 2006 Annual Report Download - page 65

Download and view the complete annual report

Please find page 65 of the 2006 AT&T Wireless annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

|

|

2006 AT&T Annual Report : :

63

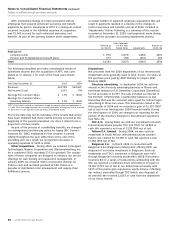

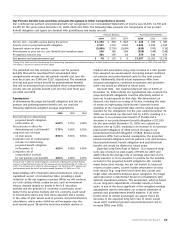

Included in the table above at December 31, 2005, was

$784 representing the remaining excess of the fair value over

the recorded value of debt in connection with the acquisition

of ATTC, of which $747 was included in our “Unamortized net

premium (discount)” and $37 was included in our “Current

maturities of long-term debt.” The excess is amortized over

the remaining lives of the underlying debt obligations.

At December 31, 2006, the aggregate principal amounts

of long-term debt and the corresponding weighted-average

interest rate scheduled for repayment for the years 2007

through 2011, excluding capitalized leases and the effect of

interest rate swaps, were $4,400 (5.5%), $3,895 (5.5%), $5,919

(4.9%), $2,253 (6.3%) and $7,485 (7.5%) with $27,911 (7.0%)

due thereafter. As of December 31, 2006 and 2005, we were

in compliance with all covenants and conditions of instruments

governing our debt. Substantially all of our outstanding long-

term debt is unsecured.

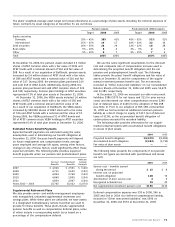

Financing Activities

Debt During 2006, debt repayments totaled $4,244 and

consisted of:

• $4,040 related to debt repayments with interest rates

ranging from 5.75% to 9.50%, which included $284

associated with unwinding an interest rate foreign currency

swap on our Euro-denominated debt (see Note 8).

• $148 related to called and put debt with interest rates

ranging from 6.35% to 9.5%.

• $56 related to scheduled principal payments on other

debt and repayments of other borrowings.

In May 2006, we received net proceeds of $1,491 from the

issuance of $1,500 of long-term debt consisting of $900 of

two-year floating rate notes and $600 of 6.80%, 30-year

bonds maturing in 2036.

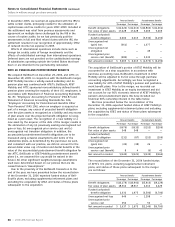

Debt maturing within one year consists of the following at

December 31:

2006 2005

Commercial paper $5,214 $ 320

Current maturities of long-term debt 4,414 4,027

Bank borrowings1 105 108

Total $9,733 $4,455

1

Primarily represents borrowings, the availability of which is contingent on the level of

cash held by some of our foreign subsidiaries.

The weighted-average interest rate on commercial paper debt

at December 31, 2006 and 2005 was 5.31% and 4.31%,

respectively.

In February 2007, we issued $3,200 of long-term debt

consisting of $1,500 principal amount of floating-rate notes due

in 2010, $1,200 principal amount of 6.375% notes due in 2056

and $500 principal amount of 5.625% notes notes due in 2016.

Credit Facility In July 2006, we replaced our three-year

$6,000 credit agreement with a five-year $6,000 credit

agreement with a syndicate of investment and commercial

banks. The current agreement will expire in July 2011. The

available credit under this agreement increased by an addi-

tional $4,000 when we completed our acquisition of BellSouth.

This incremental available credit is intended to replace Bell-

South’s $3,000 credit facility, which was terminated in January

2007. We have the right to request the lenders to further

increase their commitments (i.e., raise the available credit) up

to an additional $2,000, provided no event of default under the

credit agreement has occurred. We also have the right to

terminate, in whole or in part, amounts committed by the

lenders under this agreement in excess of any outstanding

advances; however, any such terminated commitments may

not be reinstated. Advances under this agreement may be

used for general corporate purposes, including support of

commercial paper borrowings and other short-term borrow-

ings. There is no material adverse change provision governing

the drawdown of advances under this credit agreement. This

agreement contains a negative pledge covenant, which

requires that, if at any time we or a subsidiary pledge assets or

otherwise permits a lien on its properties, advances under this

agreement will be ratably secured, subject to specified

exceptions. We must maintain a debt-to-EBITDA (earnings

before interest, income taxes, depreciation and amortization,

and other modifications described in the agreement) financial

ratio covenant of not more than three-to-one as of the last

day of each fiscal quarter for the four quarters then ended. We

are in compliance with all covenants under the agreement. We

had no borrowings outstanding under committed lines of credit

as of December 31, 2006 or 2005.

Defaults under the agreement, which would permit the

lenders to accelerate required payment, include nonpayment

of principal or interest beyond any applicable grace period;

failure by AT&T or any subsidiary to pay when due other debt

above a threshold amount that results in acceleration of that

debt (commonly referred to as “cross-acceleration”) or com-

mencement by a creditor of enforcement proceedings within

a specified period after a money judgment above a threshold

amount has become final; acquisition by any person of

beneficial ownership of more than 50% of AT&T common

shares or a change of more than a majority of AT&T’s directors

in any 24-month period other than as elected by the remain-

ing directors (commonly referred to as a “change-of-control”);

material breaches of representations in the agreement; failure

to comply with the negative pledge or debt-to-EBITDA ratio

covenants described above; failure to comply with other

covenants for a specified period after notice; failure by AT&T or

certain affiliates to make certain minimum funding payments

under ERISA; and specified events of bankruptcy or insolvency.

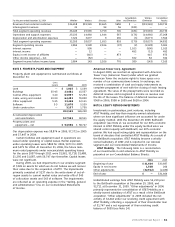

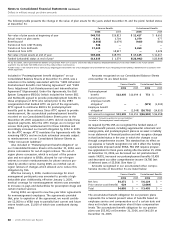

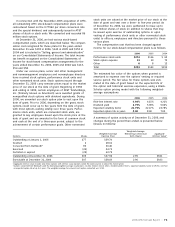

NOTE 8. FINANCIAL INSTRUMENTS

The carrying amounts and estimated fair values of our long-

term debt, including current maturities, and other financial

instruments, are summarized as follows at December 31:

2006 2005

Carrying Fair Carrying Fair

Amount Value Amount Value

Notes and debentures $54,266 $54,566 $30,027 $30,735

Commercial paper 5,214 5,214 320 320

Bank borrowings 105 105 108 108

AT&T Mobility

shareholder loan — — 4,108 4,108

Available-for-sale

equity securities 2,731 2,731 648 648

EchoStar note receivable 478 467 465 447

Preferred stock

of subsidiaries 43 43 43 43

The fair values of our notes and debentures were estimated

based on quoted market prices, where available, or on the net

present value method of expected future cash flows using