ADT 2001 Annual Report Download - page 53

Download and view the complete annual report

Please find page 53 of the 2001 ADT annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

|

|

51

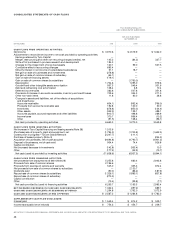

LONG-LIVED ASSETS

The Company periodically evaluates the net realizable value of

long-lived assets, including property, plant and equipment, rely-

ing on a number of factors including operating results, business

plans, economic projections and anticipated future cash flows.

An impairment in the carrying value of an asset is recognized

when the fair value of the asset is less than its carrying value.

IMPAIRED LOANS

Impaired loans include primarily large loans that are placed on

non-accrual status or any troubled debt restructuring. Loan

impairment is defined as any shortfall between the estimated

value and the recorded investment in the loan, with the esti-

mated value determined using the fair value of the collateral, if

the loan is collateral dependent, or the present value of expected

future cash flows discounted at the loan’s effective interest rate.

SECURITIZATIONS

Pools of assets are originated and sold to independent trusts

which, in turn, issue securities to investors backed by the asset

pools. Tyco Capital retains the servicing rights and participates

in certain cash flows from the pools. The present value of

expected net cash flows that exceeds the estimated cost of serv-

icing is recorded at the time of sale as a “retained interest.”

Tyco Capital’s retained interests in securitized assets are

included in other assets. Subsequent to the recording of retained

interests, Tyco Capital reviews such values on an asset by asset

basis at least as often as quarterly. Fair values of retained inter-

ests are calculated utilizing current and anticipated credit

losses, prepayment speeds and discount rates and are then com-

pared to the respective carrying values. Losses, representing the

excess of carrying value over estimated current fair market

value, are recorded as impairments and are recognized as a

charge to operations. Unrealized gains are not credited to cur-

rent earnings but are reflected in shareholders’ equity as part of

other comprehensive income.

SHARE PREMIUM AND CONTRIBUTED SURPLUS

In accordance with the Bermuda Companies Act of 1981, when

Tyco issues shares for cash at a premium to their par value, the

resulting premium is credited to a share premium account, a

non-distributable reserve. When Tyco issues shares in exchange

for shares of another company, the excess of the fair value of the

shares acquired over the par value of the shares issued by Tyco

is credited, where applicable, to contributed surplus, which is,

subject to certain conditions, a distributable reserve.

REVENUE RECOGNITION

In December 1999, the Securities and Exchange Commission

(“SEC”) issued Staff Accounting Bulletin No. 101 (“SAB 101”),

“Revenue Recognition in Financial Statements.” In SAB 101, the

SEC staff expressed its views regarding the appropriate recogni-

tion of revenue with respect to a variety of circumstances, some

of which are relevant to the Company. As required, the Company

adopted SAB 101 in the fourth quarter of Fiscal 2001 retroactive

to the beginning of the fiscal year and is now recognizing

revenues from the installation of security systems and defer-

ring the associated direct incremental costs over the estimated

customer lives.

Revenue from the sale of products is recognized according

to the terms of the sales arrangement, which is generally upon

shipment. Revenue from the sale of services is recognized as

services are rendered. Subscriber billings for services not yet

rendered are deferred and taken into income as earned, and the

deferred element is included in accrued expenses and other cur-

rent liabilities or other long-term liabilities, as appropriate.

Contract sales for the installation of fire protection systems,

underwater cable systems and other construction related pro-

jects are recorded on the percentage-of-completion method.

Profits recognized on contracts in process are based upon esti-

mated contract revenue and related cost to completion. Revi-

sions in cost estimates as contracts progress have the effect of

increasing or decreasing profits in the current period. Provisions

for anticipated losses are made in the period in which they first

become determinable.

At September 30, 2001, accounts receivable included

retainage provisions of $100.7 million, of which $73.7 million

remained unbilled. At September 30, 2000, accounts receivable

included retainage provisions of $58.6 million, of which

$2.0 million remained unbilled. These retention provisions

relate primarily to fire protection and electronics contracts and

become due upon contract completion and acceptance. Of the

balance of $100.7 million at September 30, 2001, $44.7 million is

expected to be collected during Fiscal 2002.

Finance income includes interest on loans, the accretion of

income on direct financing leases, and rents on operating leases.

Related origination and other nonrefundable fees and direct

origination costs are deferred and amortized as an adjustment

of finance income over the contractual life of the transactions.

Income on finance receivables other than leveraged leases is rec-

ognized on an accrual basis commencing in the month of origi-

nation using methods that generally approximate the interest

method. Leveraged lease income is recognized on a basis calcu-

lated to achieve a constant after-tax rate of return for periods in

which Tyco Capital has a positive investment in the transaction,

net of related deferred tax liabilities. Rental income on operat-

ing leases is recognized on an accrual basis.

The accrual of finance income on commercial and consumer

finance receivables is generally suspended and an account is

placed on non-accrual status when payment of principal or

interest is contractually delinquent for 90 days or more, or ear-

lier when, in the opinion of management, full collection of all

principal and interest due is doubtful.

LEASE FINANCING

Direct financing leases are recorded at the aggregate future

minimum lease payments plus estimated residual values less