Singapore Airlines 2003 Annual Report Download - page 107

Download and view the complete annual report

Please find page 107 of the 2003 Singapore Airlines annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

|

|

105

SIA Annual Report 02/03

Notes to the Financial Statements

31 March 2003

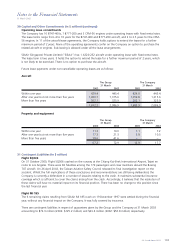

32 Financial Instruments (in $ million) (continued)

(g) Liquidity risk

At 31 March 2003, the Group had at its disposal cash and short-term deposits amounting to $819.9 million

(2002: $1,091.6 million). In addition, the Group has available short-term credit facilities of about $1,550.0

million (2002: $1,700.0 million).

The Group’s holdings of cash and short-term deposits, together with committed funding facilities and net cash

flow from operations, are expected to be sufficient to cover the cost of all firm aircraft deliveries due in the next

financial year. Any shortfall can be met by aircraft financing via structured leases, bank borrowings or public

market funding. Because of the necessity to plan aircraft orders well in advance of delivery, it is not economical

for the Group to have committed funding in place at present for all outstanding orders, many of which relate to

aircraft which will not be delivered for several years. The Group’s policies in this regard are in line with the

funding policies of other major airlines.

(h) Derivative financial instruments

The Group’s policy on the use of derivatives is not to trade in them but to use these instruments as hedges

against specific exposures.

As part of its management of treasury risks, the Group has entered into a number of forward foreign exchange

contracts to cover a portion of the surplus position in a variety of currencies. The Group uses forward contracts

purely as a hedging tool. It does not take positions in currencies with a view to make speculative gains from

currency movements. Similarly, the Group enters into interest rate swaps to manage interest rate risks on its

financial assets and liabilities, with the prior approval of the BFC or Boards of Subsidiaries. Other treasury

derivative instruments are considered on their merits as valid and appropriate risk management tools and require

the BFC’s approval before adoption.

The Group’s strategy for managing the risk on fuel price, as defined by BFC, aims to provide the Group with

protection against sudden and significant increases in jet fuel prices. In meeting these objectives, the fuel risk

management programme allows for the judicious use of approved instruments such as swaps and options with

approved counterparties and within approved credit limits.

As derivatives are used for the purpose of risk management, they do not expose the Group to market risk

because gains and losses on the derivatives offset losses and gains on the matching asset, liability, revenues or

costs being hedged. Moreover, counterparty credit risk is generally restricted to any hedging gain from time to

time, and not the principal amount hedged. Therefore the possibility of material loss arising in the event of non-

performance by a counterparty is considered to be unlikely.

The Group has a number of foreign exchange contracts outstanding as of 31 March 2003 that have been

entered into as a hedge of forecast sales denominated in UK Sterling Pound, Japanese Yen, Euro, Swiss Franc,

Australian Dollar, New Zealand Dollar, Indian Rupee, Hong Kong Dollar, Taiwan Dollar, Chinese Yuan, Korean

Won, Thai Baht, Philippines Peso and Canadian Dollar. The foreign exchange contracts provide for the Group to

sell these currencies at predetermined forward rates, buying either USD or SGD depending on forecast

requirements, with settlement dates that range from one month up to one year.

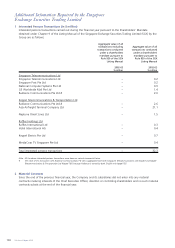

The Group had outstanding forward transactions to hedge foreign currencies and jet fuel purchases as follows:

The Group

31 March

2003 2002

Foreign currency contracts

6 months or less 524.4 268.6

Over 6 months to 24 months 363.0 314.4

887.4 583.0

Jet fuel swap/option contracts

6 months or less 399.5 304.3

Over 6 months to 24 months 233.9 176.8

633.4 481.1

(Losses)/gains not recognized in financial statements (33.4) 14.4