Singapore Airlines 2003 Annual Report Download - page 106

Download and view the complete annual report

Please find page 106 of the 2003 Singapore Airlines annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

|

|

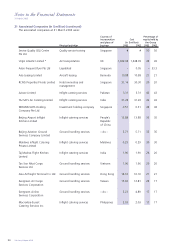

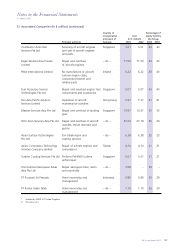

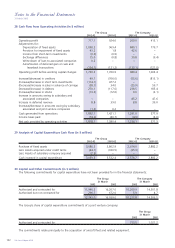

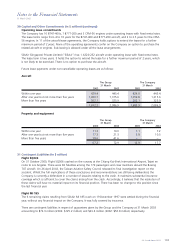

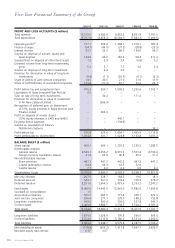

32 Financial Instruments (in $ million)

(a) Financial risk management objectives and policies

The Group operates globally and generates revenue in various currencies. The Group’s airline operations carry

certain financial and commodity risks, including the effects of changes in jet fuel prices, foreign currency

exchange rates, interest rates and the market value of its investments. The Group’s overall risk management

approach is to moderate the effects of such volatility on its financial performance.

Financial risk management policies are periodically reviewed and approved by the Board Finance Committee

("BFC").

(b) Jet fuel price risk

The Group’s earnings are affected by changes in the price of jet fuel. The Group manages this fuel price risk by

using swaps and options contracts and hedging up to 24 months forward. A change in price of one US cent per

American gallon of jet fuel affects the Group’s annual fuel costs by US$13.1 million. This is before accounting

for US Dollar ("USD") exchange rate movements and changes in volume of fuel consumed.

(c) Foreign currency risk

The Group is exposed to the effects of foreign exchange rate fluctuations because of its foreign currency

denominated operating revenues and expenses. For the financial year ended 31 March 2003 these accounted

for 78.4% of total revenue (79.3% in 2001-02) and 51.2% of total operating expenses (53.5% in 2001-02).

The Group’s largest exposures are from USD, UK Sterling Pound, Japanese Yen, Euro, Swiss Franc, Australian

Dollar, New Zealand Dollar, Indian Rupee, Hong Kong Dollar, Taiwan Dollar, Chinese Yuan, Korean Won, Thai

Baht and Malaysian Ringgit. The Group generates a surplus in all of these currencies, and a deficit in USD. The

deficit in USD is attributable to capital expenditure, leasing costs and fuel costs – all conventionally denominated

and payable in USD.

The Group manages its foreign exchange exposure by a policy of matching, as far as possible, receipts and

payments in each individual currency. Surpluses of convertible currencies are sold, as soon as practicable, for

USD and SGD. The Group also uses forward foreign currency contracts to hedge a portion of its future foreign

exchange exposure.

(d) Interest rate risk

The Group’s earnings are also affected by changes in interest rates due to the impact such changes have on

interest income and expense from short-term deposits and other interest-bearing financial assets and liabilities.

The Group’s interest-bearing financial liabilities with maturities above one year have predominantly fixed rates of

interest or are hedged by matching interest-bearing financial assets. In the latter case, interest rate swaps are

used to convert interest income into the same floating interest rate basis as interest expense.

At 31 March 2003, the Group had interest rate swap agreements in place with notional amounts ranging

from $50.8 million to $70.2 million whereby it pays a fixed rate of interest and receives a variable rate linked

to LIBOR. These swaps are used to protect a portion of long-term liabilities from exposure to fluctuations in

interest rates.

The Group’s short-term deposits and other interest-bearing financial assets and liabilities are predominantly

denominated in SGD and USD.

(e) Market price risk

The Group owned $454.6 million (2002: $461.2 million) in quoted equity and non-equity investments at

31 March 2003. The estimated market value of these investments was $522.9 million (2002: $505.1 million)

at 31 March 2003.

The market risk associated with these investments is the potential loss resulting from a decrease in market prices.

(f) Counterparty risk

Surplus funds are invested in interest-bearing bank deposits and other high quality short-term liquid

investments. Counterparty risks are managed by limiting aggregated exposure on all outstanding financial

instruments to any individual counterparty, taking into account its credit rating. Such counterparty exposures are

regularly reviewed, and adjusted as necessary. This mitigates the risk of material loss arising in the event of non-

performance by counterparties.

104 SIA Annual Report 02/03

Notes to the Financial Statements

31 March 2003