Xerox 2009 Annual Report Download - page 69

Download and view the complete annual report

Please find page 69 of the 2009 Xerox annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

|

|

67Xerox 2009 Annual Report

Notes to the Consolidated

Financial Statements

Dollars in millions, except per-share data and unless otherwise indicated.

Forecasted Purchases and Sales in Foreign Currency

We generally utilize forward foreign exchange contracts and purchased

option contracts to hedge these anticipated transactions. These

contracts generally mature in 12 months or less. A portion of these

contracts are designated as cash-flow hedges.

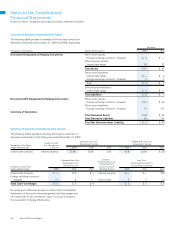

Summary of Foreign Exchange Hedging Positions

At December 31, 2009, we had outstanding forward exchange and

purchased option contracts with gross notional values of $2,093, which

is reflective of the amounts that are normally outstanding at any point

during the year.

The following is a summary of the primary hedging positions and

corresponding fair values held as of December 31, 2009:

Gross Fair Value

Notional Asset

Currency Hedged (Buy/Sell) Value (Liability)(1)

U.K. Pound Sterling/Euro $ 668 $ 6

Euro/U.S. Dollar 113 (2)

U.S. Dollar/Euro 225 3

Swedish Kronor/Euro 134 1

Swiss Franc/Euro 189 —

Japanese Yen/U.S. Dollar 237 (7)

Japanese Yen/Euro 186 1

Euro/U.K. Pound Sterling 24 —

U.S. Dollar/Canadian Dollar 20 —

All Other 297 (1)

Total Foreign Exchange Hedging $ 2,093 $ 1

(1) Represents the net receivable (payable) amount included in the Consolidated Balance

Sheet at December 31, 2009.

Foreign Currency Cash Flow Hedges

We designate a portion of our foreign currency derivative contracts

as cash flow hedges of our foreign currency-denominated inventory

purchases and sales. The changes in fair value for these contracts were

reported in Accumulated other comprehensive loss and reclassified

to Cost of sales and revenue in the period or periods during which the

related inventory was sold to a third party. No amount of ineffectiveness

was recorded in the Consolidated Statements of Income for these

designated cash flow hedges and all components of each derivative’s

gain or loss was included in the assessment of hedge effectiveness. As of

December 31, 2009, the net asset fair value of these contracts was $1.

Cash Flow Hedges

As of December 31, 2008, a pay fixed/receive variable interest rate

swap that was designated and accounted for as a cash flow hedge,

had a notional amount of $150 and a net liability fair value of $2.

The swap was structured to hedge the LIBOR interest rate of the floating

Senior Notes due 2009 by converting it from a variable rate instrument

to a fixed rate instrument. The swap matured in conjunction with the

repayment of the Senior Notes in December 2009. No ineffective

portion was recorded to earnings during 2009, 2008 or 2007 and

all components of the derivative gain or loss was included in the

assessment of hedged effectiveness.

Terminated Swaps

During the period from 2004 to 2009, we early-terminated several

interest rate swaps which had been designated as fair value hedges

of certain debt instruments. These terminated interest rate swaps

had an aggregate notional value of $4.0 billion. The associated net

fair value adjustments to the debt instruments are being amortized

to interest expense over the remaining term of the related notes. In

2009, 2008 and 2007, the amortization of these fair value adjustments

reduced interest expense by $17, $12 and $9, respectively, and we

expect to record a net decrease in interest expense of $133 in future

years through 2027.

Foreign Exchange Risk Management

We are a global company that is exposed to foreign currency exchange

rate fluctuations in the normal course of its business. As a part of

our foreign exchange risk management strategy, we use derivative

instruments, primarily forward contracts, to hedge certain foreign

currency exposures, thereby reducing volatility of earnings or protecting

fair values of assets and liabilities.

Foreign Currency-Denominated Assets and Liabilities

We generally utilize forward foreign exchange contracts to hedge

these exposures. Changes in the value of these currency derivatives

are recorded in earnings together with the offsetting foreign exchange

gains and losses on the underlying assets and liabilities.