Xerox 2009 Annual Report Download - page 53

Download and view the complete annual report

Please find page 53 of the 2009 Xerox annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

|

|

51Xerox 2009 Annual Report

Notes to the Consolidated

Financial Statements

Dollars in millions, except per-share data and unless otherwise indicated.

Land, Buildings and Equipment and Equipment on Operating Leases

Land, buildings and equipment are recorded at cost. Buildings and

equipment are depreciated over their estimated useful lives. Leasehold

improvements are depreciated over the shorter of the lease term or

the estimated useful life. Equipment on operating leases is depreciated

to estimated salvage value over the lease term. Depreciation is

computed using the straight-line method. Significant improvements

are capitalized and maintenance and repairs are expensed. Refer to

Note 5 – Inventories and Equipment on Operating Leases, Net and

Note 6 – Land, Buildings and Equipment, Net for further discussion.

Internal Use Software

We capitalize direct costs associated with developing, purchasing or

otherwise acquiring software for internal use and amortize these costs

on a straight-line basis over the expected useful life of the software,

beginning when the software is implemented. Useful lives of the

software generally vary from three to seven years. Amortization expense

was $53, $50 and $76 for the years ended December 31, 2009, 2008

and 2007, respectively. Capitalized costs were $354 and $288 as of

December 31, 2009 and 2008, respectively.

Goodwill and Other Intangible Assets

Goodwill is tested for impairment annually or more frequently if an

event or circumstance indicates that an impairment loss may have

been incurred. Application of the goodwill impairment test requires

judgment, including the identification of reporting units, assignment

of assets and liabilities to reporting units, assignment of goodwill to

reporting units and determination of the fair value of each reporting

unit. We estimate the fair value of each reporting unit using a discounted

cash flow methodology. This requires us to use significant judgment

including estimation of future cash flows, which is dependent on internal

forecasts, estimation of the long-term rate of growth for our business,

the useful life over which cash flows will occur, determination of our

weighted average cost of capital and relevant market data.

Other intangible assets primarily consist of assets obtained in connection

with business acquisitions, including installed customer base and

distribution network relationships, patents on existing technology and

trademarks. We apply an impairment evaluation whenever events or

changes in business circumstances indicate that the carrying value of

our intangible assets may not be recoverable. Other intangible assets

are amortized on a straight-line basis over their estimated economic

lives. We believe that the straight-line method of amortization reflects

an appropriate allocation of the cost of the intangible assets to earnings

in proportion to the amount of economic benefits obtained annually

by the Company. Refer to Note 8 – Goodwill and Intangible Assets, Net

for further information.

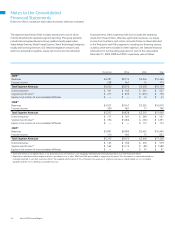

Restricted Cash and Investments

As more fully discussed in Note 16 – Contingencies, various litigation

matters in Brazil require us to make cash deposits as a condition of

continuing the litigation. In addition, several of our secured financing

arrangements and other contracts require us to post cash collateral

or maintain minimum cash balances in escrow. These cash amounts

are classified in our Consolidated Balance Sheets based on when the

cash will be contractually or judicially released (refer to Note 10 –

Supplementary Financial Information for classification of amounts).

At December 31, 2009 and 2008, such restricted cash amounts

were as follows:

December 31,

2009 2008

Tax and other litigation deposits in Brazil $ 240 $ 167

Escrow and cash collections related to receivable

sales and secured borrowing arrangements 29 16

Other restricted cash 20 20

Total Restricted Cash and Investments $ 289 $ 203

Provisions for Losses on Uncollectible Receivables

The provisions for losses on uncollectible trade and finance receivables

are determined principally on the basis of past collection experience

applied to ongoing evaluations of our receivables and evaluations of

the default risks of repayment.

Allowances for doubtful accounts as of December 31, 2009 and 2008

were as follows:

December 31,

2009 2008

Allowance for doubtful accounts receivables $ 148 $ 131

Allowance for doubtful finance receivables $ 222 $ 198

Inventories

Inventories are carried at the lower of average cost or market. Inventories

also include equipment that is returned at the end of the lease term.

Returned equipment is recorded at the lower of remaining net book

value or salvage value. Salvage value consists of the estimated market

value (generally determined based on replacement cost) of the

salvageable component parts, which are expected to be used in the

remanufacturing process. We regularly review inventory quantities

and record a provision for excess and/or obsolete inventory based

primarily on our estimated forecast of product demand, production

requirements and servicing commitments. Several factors may influence

the realizability of our inventories, including our decision to exit a

product line, technological changes and new product development.

The provision for excess and/or obsolete raw materials and equipment

inventories is based primarily on near-term forecasts of product demand

and include consideration of new product introductions, as well as

changes in remanufacturing strategies. The provision for excess and/or

obsolete service parts inventory is based primarily on projected servicing

requirements over the life of the related equipment populations.