Xerox 2008 Annual Report Download - page 84

Download and view the complete annual report

Please find page 84 of the 2008 Xerox annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

-

96

-

97

-

98

-

99

-

100

|

|

Notes to the Consolidated

Financial Statements

(in millions, except per share data and

unless otherwise indicated)

Although realization is not assured, we have concluded that it is

more-likely-than-not that the deferred tax assets for which a

valuation allowance was determined to be unnecessary, will be

realized in the ordinary course of operations based on the available

positive and negative evidence, including scheduling of deferred

tax liabilities and projected income from operating activities. The

amount of the net deferred tax assets considered realizable,

however, could be reduced in the near term if actual future income

or income tax rates are lower than estimated, or if there are

differences in the timing or amount of future reversals of existing

taxable or deductible temporary differences.

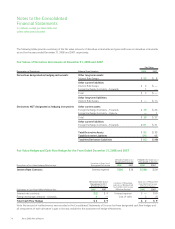

At December 31, 2008, we had tax credit carryforwards of $552

available to offset future income taxes, of which $213 are

available to carryforward indefinitely while the remaining $339 will

begin to expire, if not utilized, in 2009. We also had net operating

loss carryforwards for income tax purposes of $345 that will expire

in 2009 through 2024, if not utilized, and $2.3 billion available to

offset future taxable income indefinitely.

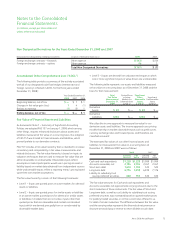

Note 16 – Contingencies

Brazil Tax and Labor Contingencies

Our Brazilian operations are involved in various litigation matters

and have received or been the subject of numerous governmental

assessments related to indirect and other taxes as well as disputes

associated with former employees and contract labor. The tax

matters, which comprise a significant portion of the total

contingencies, principally relate to claims for taxes on the internal

transfer of inventory, municipal service taxes on rentals and gross

revenue taxes. We are disputing these tax matters and intend to

vigorously defend our position. Based on the opinion of legal

counsel and current reserves for those matters deemed probable of

loss, we do not believe that the ultimate resolution of these

matters will materially impact our results of operations, financial

position or cash flows. The labor matters principally relate to claims

made by former employees and contract labor for the equivalent

payment of all social security and other related labor benefits, as

well as consequential tax claims, as if they were regular employees.

Following our assessment of the most recent trend in the outcomes

of these matters, we reassessed the probable estimated loss and,

as a result, recorded an additional reserve of $36 in 2008. As of

December 31, 2008, the total amounts related to the unreserved

portion of the tax and labor contingencies, inclusive of any related

interest, amounted to approximately $839, with the decrease from

December 31, 2007 balance of $1.1 billion primarily related to

currency partially offset by the additional reserve. In connection

with the above proceedings, customary local regulations may

require us to make escrow cash deposits or post other security of

up to half of the total amount in dispute. As of December 31, 2008

we had $167 of escrow cash deposits for matters we are disputing

and there are liens on certain Brazilian assets with a net book value

of $30 and additional letters of credit of approximately $88.

Generally, any escrowed amounts would be refundable and any

liens would be removed to the extent the matters are resolved in

our favor. We routinely assess all these matters as to probability of

ultimately incurring a liability against our Brazilian operations and

record our best estimate of the ultimate loss in situations where we

assess the likelihood of an ultimate loss as probable.

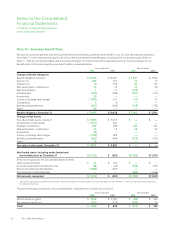

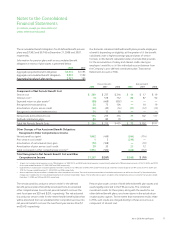

Legal Matters

As more fully discussed below, we are involved in a variety of

claims, lawsuits, investigations and proceedings concerning

securities law, intellectual property law, environmental law,

employment law and the Employee Retirement Income Security

Act (“ERISA”). We determine whether an estimated loss from a

contingency should be accrued by assessing whether a loss is

deemed probable and can be reasonably estimated. We assess our

potential liability by analyzing our litigation and regulatory matters

using available information. We develop our views on estimated

losses in consultation with outside counsel handling our defense in

these matters, which involves an analysis of potential results,

assuming a combination of litigation and settlement strategies.

Should developments in any of these matters cause a change in

our determination as to an unfavorable outcome and result in the

need to recognize a material accrual, or should any of these

matters result in a final adverse judgment or be settled for

significant amounts, they could have a material adverse effect on

our results of operations, cash flows and financial position in the

period or periods in which such change in determination, judgment

or settlement occurs.

The following is a summary of significant developments in

litigation matters:

•Carlson v. Xerox Corporation, et al. – settlement reached,

approved by the district court and paid.

•In re Xerox Corp. ERISA Litigation – settlement reached and

preliminary court approval granted.

•Florida State Board of Administration, et al v. Xerox

Corporation, et al. – settlement reached and paid.

•National Union Fire Insurance Company v. Xerox

Corporation, et al. – settlement reached and payment made to

Xerox.

•Digwamaje et al. v. IBM et al. – amended complaint drops

Xerox as a defendant.

•Warren, et al. v. Xerox Corporation – settlement received final

court approval and was paid.

82 Xerox 2008 Annual Report