UPS 2012 Annual Report Download - page 66

Download and view the complete annual report

Please find page 66 of the 2012 UPS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

|

|

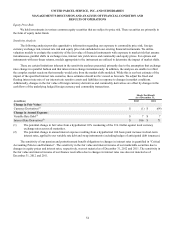

UNITED PARCEL SERVICE, INC. AND SUBSIDIARIES

MANAGEMENT'S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND

RESULTS OF OPERATIONS

54

Equity Price Risk

We hold investments in various common equity securities that are subject to price risk. These securities are primarily in

the form of equity index funds.

Sensitivity Analysis

The following analysis provides quantitative information regarding our exposure to commodity price risk, foreign

currency exchange risk, interest rate risk and equity price risk embedded in our existing financial instruments. We utilize

valuation models to evaluate the sensitivity of the fair value of financial instruments with exposure to market risk that assume

instantaneous, parallel shifts in exchange rates, interest rate yield curves and commodity and equity prices. For options and

instruments with non-linear returns, models appropriate to the instrument are utilized to determine the impact of market shifts.

There are certain limitations inherent in the sensitivity analyses presented, primarily due to the assumption that exchange

rates change in a parallel fashion and that interest rates change instantaneously. In addition, the analyses are unable to reflect

the complex market reactions that normally would arise from the market shifts modeled. While this is our best estimate of the

impact of the specified interest rate scenarios, these estimates should not be viewed as forecasts. We adjust the fixed and

floating interest rate mix of our interest rate sensitive assets and liabilities in response to changes in market conditions.

Additionally, changes in the fair value of foreign currency derivatives and commodity derivatives are offset by changes in the

cash flows of the underlying hedged foreign currency and commodity transactions.

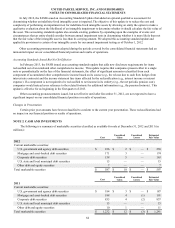

Shock-Test Result

As of December 31,

(in millions) 2012 2011

Change in Fair Value:

Currency Derivatives(1) $(1) $ (64)

Change in Annual Expense:

Variable Rate Debt(2) $ 7 $ 7

Interest Rate Derivatives(2) $ 106 $ 71

(1) The potential change in fair value from a hypothetical 10% weakening of the U.S. Dollar against local currency

exchange rates across all maturities.

(2) The potential change in annual interest expense resulting from a hypothetical 100 basis point increase in short-term

interest rates, applied to our variable rate debt and swap instruments (excluding hedges of anticipated debt issuances).

The sensitivity of our pension and postretirement benefit obligations to changes in interest rates is quantified in “Critical

Accounting Policies and Estimates”. The sensitivity in the fair value and interest income of our marketable securities due to

changes in equity prices and interest rates, respectively, was not material as of December 31, 2012 and 2011. The sensitivity in

the fair value and interest income of our finance receivables due to changes in interest rates was also not material as of

December 31, 2012 and 2011.