UPS 2012 Annual Report Download - page 34

Download and view the complete annual report

Please find page 34 of the 2012 UPS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

|

|

22

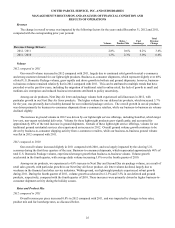

Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operation

Overview

The U.S. economic expansion has continued at a slow-to-moderate pace through the end of 2012. Continued growth in

retail sales, particularly among e-commerce retailers, has provided for expansion in the overall U.S. small package delivery

market; however, recent weakness in manufacturing activity, combined with the uneven nature of the overall economic

recovery, has negatively impacted the small package delivery market. Given these trends, our products most aligned with

business-to-consumer shipments have experienced the strongest growth, while our business-to-business volume continues to

lag overall GDP growth.

Outside of the U.S., economic growth has slowed considerably due to volatility in world markets and fiscal austerity

measures, particularly in Europe. This slower global economic growth has created an environment in which customers are

more likely to trade-down from premium express products to standard delivery products. Additionally, the uneven nature of

economic growth worldwide has led to shifting trade patterns whereby transcontinental trade is being pressured, but intra-

regional trade is continuing to grow. These circumstances have led us to adjust our air capacity and cost structure in our

transportation network to the prevailing volume mix levels. Our broad portfolio of product offerings and the flexibilities

inherent in our transportation network have helped us adapt to these changing trends.

While the worldwide economic environment has been challenging in 2012, we have continued to undertake initiatives to

improve yield management, increase operational efficiency and contain costs across all segments. Continued deployment of

technology improvements should lead to further gains in our operational efficiency, flexibility and reliability, thus restraining

cost increases and improving margins. In our International Package segment, we have adjusted our air network and utilized

newly constructed or expanded operating facilities to improve time-in-transit for shipments in each region. We have also

continued to optimize our aircraft network to leverage the new route authority we have gained over the last several years and to

take full advantage of faster growing trade lanes. Additionally, in the first quarter of 2012, we acquired Kiala S.A., which will

expand our service offerings for business-to-consumer deliveries in Europe.

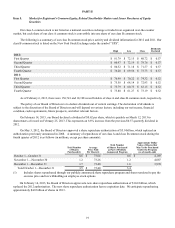

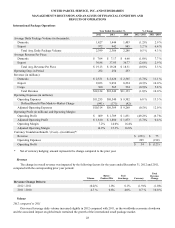

Our consolidated results are presented in the table below:

Year Ended December 31, % Change

2012 2011 2010 2012 / 2011 2011 / 2010

Revenue (in millions) $ 54,127 $ 53,105 $ 49,545 1.9 % 7.2%

Operating Expenses (in millions) 52,784 47,025 43,904 12.2 % 7.1%

Operating Profit (in millions) $ 1,343 $ 6,080 $ 5,641 (77.9)% 7.8%

Operating Margin 2.5% 11.4% 11.4%

Average Daily Package Volume (in thousands) 16,295 15,797 15,574 3.2 % 1.4%

Average Revenue Per Piece $ 10.82 $ 10.82 $ 10.24 — % 5.7%

Net Income (in millions) $ 807 $ 3,804 $ 3,338 (78.8)% 14.0%

Basic Earnings Per Share $ 0.84 $ 3.88 $ 3.36 (78.4)% 15.5%

Diluted Earnings Per Share $ 0.83 $ 3.84 $ 3.33 (78.4)% 15.3%

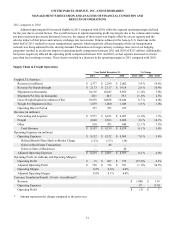

Items Affecting Comparability

The year-over-year comparisons of our financial results are affected by the following items (in millions):

Year Ended December 31,

2012 2011 2010

Operating Expenses:

Defined Benefit Plans Mark-to-Market Charge $ 4,831 $ 827 $ 112

Multiemployer Pension Plan Withdrawal Charge 896 — —

Restructuring Charge — — 98

Gains on Sales of Businesses — — (20)

Gains on Real Estate Transactions — (33)(109)

Income Tax Expense (Benefit) from the Items Above (2,145)(287) —

Charge for Change in Tax Filing Status for German Subsidiary — — 76