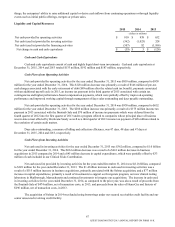

Quest Diagnostics 2015 Annual Report Download - page 70

Download and view the complete annual report

Please find page 70 of the 2015 Quest Diagnostics annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

|

|

66

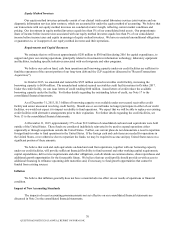

Quantitative and Qualitative Disclosures About Market Risk

We address our exposure to market risks, principally the market risk of changes in interest rates, through a controlled

program of risk management that includes the use of derivative financial instruments. We do not hold or issue derivative

financial instruments for speculative purposes. We seek to mitigate the variability in cash outflows that result from changes in

interest rates by maintaining a balanced mix of fixed-rate and variable-rate debt obligations. In order to achieve this objective,

we have entered into interest rate swaps. Interest rate swaps involve the periodic exchange of payments without the exchange

of underlying principal or notional amounts. Net settlements are recognized as an adjustment to interest expense. We believe

that our exposures to foreign exchange impacts and changes in commodity prices are not material to our consolidated financial

condition or results of operations.

At December 31, 2015 and 2014, the fair value of our debt was estimated at approximately $3.7 billion and $4.2

billion, respectively, using quoted active market prices and yields for the same or similar types of borrowings, taking into

account the underlying terms of the debt instruments. At December 31, 2015 and 2014, the estimated fair value exceeded the

carrying value of the debt by $82 million and $416 million, respectively. A hypothetical 10% increase in interest rates

(representing 39 basis points and 45 basis points at December 31, 2015 and 2014, respectively) would potentially reduce the

estimated fair value of our debt by approximately $112 million and $108 million at December 31, 2015 and 2014, respectively.

Borrowings under our secured receivables credit facility and our senior unsecured revolving credit facility are subject

to variable interest rates. Interest on our secured receivables credit facility is based on rates that are intended to approximate

commercial paper rates for highly rated issuers plus a spread. Interest on our senior unsecured revolving credit facility is

subject to a pricing schedule that can fluctuate based on changes in our credit ratings. As such, our borrowing cost under this

credit arrangement will be subject to both fluctuations in interest rates and changes in our credit ratings. At December 31,

2015, the borrowing rates under these debt instruments were: for our secured receivables credit facility, 0.96%; and for our

senior unsecured revolving credit facility, LIBOR plus 1.125%. At December 31, 2015, the weighted average LIBOR was

0.4%. As of December 31, 2015, there were no borrowings outstanding under our $600 million secured receivables credit

facility or under our $750 million senior unsecured revolving credit facility.

The notional amount of fixed-to-variable interest rate swaps at both December 31, 2015 and 2014 was $1.2 billion.

The aggregate fair value of the fixed-to-variable interest rate swaps that are in an asset position was $23 million at

December 31, 2015. The aggregate fair value of the fixed-to-variable interest rate swaps that are in a liability position was $6

million at December 31, 2015. There were no forward starting interest rate swaps outstanding at December 31, 2015. The

notional amount of forward starting interest rate swaps at December 31, 2014 was $150 million.

Based on our net exposure to interest rate changes, a hypothetical 10% change to the variable interest rate component

of our variable rate indebtedness (representing 3 basis points) would not impact annual interest expense materially, assuming no

changes to the debt outstanding at December 31, 2015. A hypothetical 10% change in the forward one-month LIBOR curve

(representing a 18 basis point change in the weighted average yield) would potentially change the fair value of our derivative

assets by $8 million. A hypothetical 10% change in the forward one-month LIBOR curve (representing a 15 basis point change

in the weighted average yield) would potentially change the fair value of our derivative liabilities by $4 million.

For further details regarding our outstanding debt and our financial instruments and hedging activities, see Notes 13

and 14, respectively, to the consolidated financial statements.

Risk Associated with Investment Portfolio

Our investment portfolio includes equity investments comprised primarily of strategic equity holdings in privately and

publicly held companies. These securities are exposed to price fluctuations and are generally concentrated in the life sciences

industry. The carrying value of our equity investments (excluding investments accounted for under the equity method) was $14

million at December 31, 2015.

We regularly evaluate the fair value measurements of our equity investments to determine if losses in value are other

than temporary and if an impairment loss has been incurred. The evaluation considers whether the security has the ability to

recover and, if so, the estimated recovery period. Other factors that are considered in this evaluation include the amount of the

other-than-temporary decline and its duration, the issuer’s financial condition and short-term prospects and whether the market

decline was caused by overall economic conditions or conditions specific to the individual security.

We do not hedge our equity price risk. The impact of an adverse movement in equity prices on our holdings in

privately held companies cannot be easily quantified, as our ability to realize returns on investments depends on, among other

QUEST DIAGNOSTICS 2015 ANNUAL REPORT ON FORM 10-K