Quest Diagnostics 2015 Annual Report Download - page 35

Download and view the complete annual report

Please find page 35 of the 2015 Quest Diagnostics annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

|

|

31

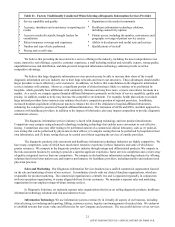

The clinical testing business is highly competitive, and if we fail to provide an appropriately priced level of service or

otherwise fail to compete effectively it could have a material adverse effect on our revenues and profitability.

The clinical testing business remains a fragmented and highly competitive industry. We primarily compete with three

types of clinical testing providers: other commercial clinical laboratories, hospital-affiliated laboratories and physician-office

laboratories. We also compete with other providers, including anatomic pathology practices and large physician group

practices. Hospitals generally maintain on-site laboratories to perform testing on their patients (inpatient or outpatient). In

addition, many hospitals compete with commercial clinical laboratories for outreach (non-hospital patients) testing. Hospitals

may seek to leverage their relationships with community clinicians and encourage the clinicians to send their outreach testing

to the hospital's laboratory. In addition, hospitals that own physician practices may require the practices to refer testing to the

hospital's laboratory. In recent years, there has been a trend of hospitals acquiring physician practices, and as a result, an

increased percentage of physician practices are owned by hospitals. As a result of this affiliation between hospitals and

community clinicians, we compete against hospital-affiliated laboratories primarily based on quality and scope of service as

well as pricing. Increased hospital acquisitions of physician practices enhance clinician ties to hospital-affiliated laboratories

and may strengthen their competitive position. The formation of ACOs and IDNs, and their approach to contracts with

healthcare providers, in addition to the impact of informatics, also may increase competition to provide diagnostic information

services.

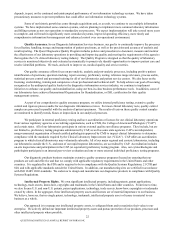

The diagnostic information services industry also is faced with changing technology and new product introductions.

Competitors may compete using advanced technology, including technology that enables more convenient or cost-effective

testing. Competitors also may offer testing to be performed outside of a commercial clinical laboratory, such as (1) point-of-

care testing that can be performed by physicians in their offices; (2) complex testing that can be performed by hospitals in their

own laboratories; and (3) home testing that can be carried out without requiring the services of outside providers.

Government payers, such as Medicare and Medicaid, have taken steps to reduce the utilization and reimbursement of

healthcare services, including clinical testing services.

We face efforts by government payers to reduce utilization of and reimbursement for diagnostic information services.

We expect efforts to reduce reimbursements, to impose more stringent cost controls and to reduce utilization of clinical test

services will continue.

From time to time, Congress has legislated reductions in, or frozen updates to, the Medicare Clinical Laboratory Fee

Schedule. In addition, CMS has adopted policies limiting or excluding coverage for clinical tests that we perform. We also

provide physician services which are reimbursed by Medicare under a physician fee schedule, which is subject to adjustment on

an annual basis. In recent years, reductions in the Medicare Physician Fee Schedule for anatomic pathology services adversely

impacted our business relative to the business of some of our competitors whose anatomic pathology business was not as

sizable as ours. Medicaid reimbursement varies by state and is subject to administrative and billing requirements and budget

pressures. The 2010 federal healthcare reform legislation includes further provisions that are designed to control utilization and

payment levels.

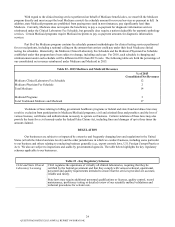

In addition, over the last several years, the federal government has continued to expand its contracts with private

health insurance plans for Medicare beneficiaries, called “Medicare Advantage” programs, and has encouraged such

beneficiaries to switch from the traditional programs to the private programs. There has been continued growth of health

insurance plans offering Medicare Advantage programs, and of beneficiary enrollment in these programs. Also in recent years,

states have mandated that Medicaid beneficiaries enroll in private managed care arrangements. Recently, state budget pressures

have encouraged states to consider several courses of action that may impact our business, such as delaying payments, reducing

reimbursement, restricting coverage eligibility, denying claims and service coverage restrictions.

From time to time, the federal government has considered whether competitive bidding could be used to provide

clinical testing services for Medicare beneficiaries at attractive rates while maintaining quality and access to care. Congress

periodically considers cost-saving initiatives as part of its deficit reduction discussions. These initiatives have included

coinsurance for clinical testing services, co-payments for clinical testing and further laboratory fee schedule reductions.

2014 U.S. federal legislation, the Protecting Access to Medicare Act of 2014, is impacting the clinical testing industry.

Key parts of this legislation included provisions that provide for the establishment of an advisory panel and a market-based

process to rebase the Clinical Laboratory Fee Schedule, developing a new fee schedule and limiting reductions in that fee

schedule. If this process does not recognize the value that clinical testing services bring to the healthcare system, our business

can be materially adversely impacted.

QUEST DIAGNOSTICS 2015 ANNUAL REPORT ON FORM 10-K