Quest Diagnostics 2015 Annual Report Download - page 25

Download and view the complete annual report

Please find page 25 of the 2015 Quest Diagnostics annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

|

|

21

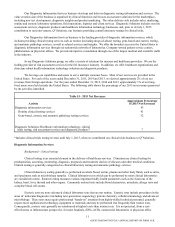

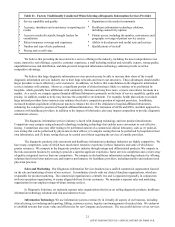

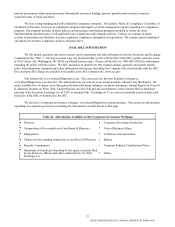

Table 21 - Factors Traditionally Considered When Selecting a Diagnostic Information Services Provider

Service capability and quality Reputation in the medical community

Accuracy, timeliness and consistency in reporting test

results

Healthcare information technology solutions,

including connectivity options

Access to medical/scientific thought leaders for

consultation

Patient access, including the number, convenience and

geographic coverage of patient service centers

Patient insurance coverage and experience Ability to develop new and useful tests and services

Number and type of tests performed Qualifications of its staff

Pricing and overall value

We believe that providing the most attractive service offering in the industry, including the most comprehensive test

menu, innovative test offerings, a positive customer experience, a staff including medical and scientific experts, strong quality,

unparalleled access and distribution, and data-powered integrated information technology solutions provide us with a

competitive advantage.

We believe that large diagnostic information services providers may be able to increase their share of the overall

diagnostic information services industry due to their large networks and lower cost structures. These advantages should enable

larger providers to more effectively serve customers. In addition, we believe that consolidation in the diagnostic information

services industry will continue. However, a significant portion of clinical testing is likely to continue to be performed by

hospitals, which generally have affiliations with community clinicians and may have more, or more convenient, locations in a

market. As a result, we compete against hospital-affiliated laboratories primarily on the basis of service capability, quality and

pricing. In addition, market activity may increase the competitive environment. For example, health plan actions to exclude

large national providers from contracts may enhance the relative competitive position of regional providers. In addition,

increased hospital acquisitions of physician practices enhance the ties of the clinicians to hospital-affiliated laboratories,

enhancing the competitive position of hospital-affiliated laboratories. The formation of ACOs and IDNs, and their approach to

contracts with healthcare providers, in addition to the impact of informatics, also may impact competition to provide diagnostic

information services.

The diagnostic information services industry is faced with changing technology and new product introductions.

Competitors may compete using advanced technology, including technology that enables more convenient or cost-effective

testing. Competitors also may offer testing to be performed outside of a commercial clinical laboratory, such as (1) point-of-

care testing that can be performed by physicians in their offices; (2) complex testing that can be performed by hospitals in their

own laboratories; and (3) home testing that can be carried out without requiring the services of outside providers.

The diagnostic products, risk assessment and healthcare information technology industries are highly competitive. We

have many competitors, some of which have much more extensive experience in these industries and some of which have

greater resources. We compete in the diagnostic products industry through unique and differentiated products. We compete in

the risk assessment business by seeking to provide a superior applicant experience, faster services completion and a wider array

of quality, integrated services than our competitors. We compete in the healthcare information technology industry by offering

solutions that foster better patient care and improve performance for healthcare providers, including smaller and medium sized

physician practices.

Sales and Marketing. Our Diagnostic Information Services business has a unified commercial organization focused

on the sale and marketing of most of our services. It coordinates closely with our clinical franchise organizations, which are

responsible for product marketing. The commercial organization is centrally led, and is organized regionally, in conjunction

with our operations organization, to ensure aligned delivery for our customers. We maintain a separate sales and marketing

organization for our employer drugs-of-abuse testing services.

In Diagnostic Solutions, we maintain separate sales organizations that focus on selling diagnostic products, healthcare

information technology solutions and risk assessment services.

Information Technology. We use information systems extensively in virtually all aspects of our business, including

clinical testing, test ordering and reporting, billing, customer service, logistics and management of medical data. We endeavor

to establish systems that create value and efficiencies for our Company and customers. The successful delivery of our services

QUEST DIAGNOSTICS 2015 ANNUAL REPORT ON FORM 10-K