Pitney Bowes 2008 Annual Report Download - page 65

Download and view the complete annual report

Please find page 65 of the 2008 Pitney Bowes annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

|

|

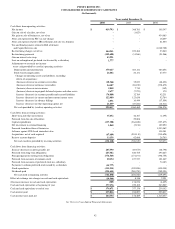

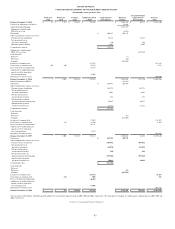

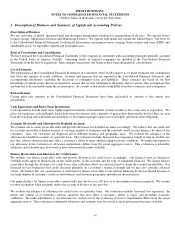

PITNEY BOWES INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

(Tabular dollars in thousands, except per share data)

46

Impairment Review for Long-Lived Assets

Long-lived assets are reviewed for impairment on an annual basis or whenever events or changes in circumstances indicate that the

carrying amount may not be fully recoverable. If such a change in circumstances occurs, the related estimated future undiscounted

cash flows expected to result from the use of the asset and its eventual disposition are compared to the carrying amount. If the sum of

the expected cash flows is less than the carrying amount, we record an impairment charge. The impairment charge is measured as the

amount by which the carrying amount exceeds the fair value of the asset. The fair values of impaired long-lived assets are determined

using probability weighted expected cash flow estimates, quoted market prices when available and appraisals as appropriate in

accordance with SFAS No. 144, Accounting for the Impairment or Disposal of Long-Lived Assets. See Note 14 to the Consolidated

Financial Statements for further details.

Retirement Plans

In accordance with SFAS No. 87, Employers’ Accounting for Pensions, and SFAS No. 106, Employers’ Accounting for Postretirement

Benefits Other Than Pensions, actual results that differ from our assumptions and estimates are accumulated and amortized over the

estimated future working life of the plan participants and will therefore affect pension expense recognized in future periods. Net

pension expense is based primarily on current service costs, interest costs and the returns on plan assets. In accordance with this

approach, differences between the actual and expected return on plan assets are recognized over a five-year period. In accordance

with SFAS No. 158, Employers’ Accounting for Defined Pension and Other Post Retirement Plans an amendment to FASB Statements

No. 87, 88, 106 and 132(R), we recognize the overfunded or underfunded status of pension and other postretirement benefit plans on

the balance sheet. Under SFAS No. 158, gains and losses, prior service costs and credits, and any remaining transition amounts under

SFAS No. 87 and SFAS No. 106 that have not yet been recognized in net periodic benefit costs are recognized in accumulated other

comprehensive income, net of tax, until they are amortized as a component of net periodic benefit cost. We use a measurement date of

December 31 for all of our retirement plans. See Note 13 to the Consolidated Financial Statements for further details.

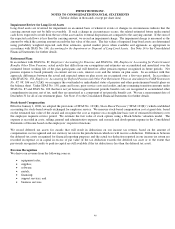

Stock-based Compensation

Effective January 1, 2006, we adopted the provisions of SFAS No. 123(R), Share-Based Payment (“SFAS 123(R)”) which established

accounting for stock-based awards exchanged for employee service. We measure stock-based compensation cost at grant date, based

on the estimated fair value of the award, and recognize the cost as expense on a straight-line basis (net of estimated forfeitures) over

the employee requisite service period. We estimate the fair value of stock options using a Black-Scholes valuation model. The

expense is recorded in costs; selling, general and administrative expense; and research and development expense in the Consolidated

Statements of Income based on the employees’ respective functions.

We record deferred tax assets for awards that will result in deductions on our income tax returns, based on the amount of

compensation cost recognized and our statutory tax rate in the jurisdiction in which we will receive a deduction. Differences between

the deferred tax assets recognized for financial reporting purposes and the actual tax deduction reported in our income tax return are

recorded in expense or in capital in excess of par value (if the tax deduction exceeds the deferred tax asset or to the extent that

previously recognized credits to paid-in-capital are still available if the tax deduction is less than the deferred tax asset).

Revenue Recognition

We derive our revenue from the following sources:

• equipment sales;

• supplies;

• software;

• rentals;

• financing;

• support services; and

• business services.