Pitney Bowes 2008 Annual Report Download - page 45

Download and view the complete annual report

Please find page 45 of the 2008 Pitney Bowes annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

|

|

26

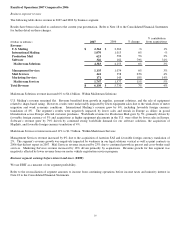

Sensitivity to changes in assumptions:

U.S. Pension Plan

• Discount rate – a 0.25% increase in the discount rate would decrease annual pension expense by approximately $2.8 million

and would lower the projected benefit obligation by $39.8 million.

• Rate of compensation increase – a 0.25% increase in the rate of compensation increase would increase annual pension

expense by approximately $2.5 million.

• Expected return on plan assets – a 0.25% increase in the expected return on assets of our principal plans would decrease

annual pension expense by approximately $3.8 million.

The following assumptions relate to our U.K. qualified pension plan, which is our largest foreign plan. We determine our discount

rate for the U.K. retirement benefit plan by using a model that discounts each year’s estimated benefit payments by an applicable spot

rate. These spot rates are derived from a yield curve created from a large number of high quality corporate bonds. Accordingly, our

discount rate assumption was 6.3% at December 31, 2008 and 5.8% at December 31, 2007. The rate of compensation increase

assumption reflects our actual experience and best estimate of future increases. Our estimate of the rate of compensation increase was

4.3% at December 31, 2008 and 4.7% at December 31, 2007. Our expected return on plan assets is determined based on historical

portfolio results, the plan’s asset mix and future expectations of market rates of return on the types of assets in the plan. Our expected

return on plan assets assumption was 7.25% in 2008 and 7.75% at December 31, 2007.

U.K. Pension Plan

• Discount rate – a 0.25% increase in the discount rate would decrease annual pension expense by approximately $2.0 million

and would lower the projected benefit obligation by $12.3 million.

• Rate of compensation increase – a 0.25% increase in the rate of compensation increase would increase annual pension

expense by approximately $0.7 million.

• Expected return on plan assets – a 0.25% increase in the expected return on assets of our principal plans would decrease

annual pension expense by approximately $0.9 million.

Delayed recognition principles

In accordance with SFAS No. 87, Employers’ Accounting for Pensions, actual pension plan results that differ from our assumptions

and estimates are accumulated and amortized over the estimated future working life of the plan participants and will therefore affect

pension expense recognized and obligations recorded in future periods. We also base our net pension expense primarily on a market

related valuation of plan assets. In accordance with this approach, we recognize differences between the actual and expected return on

plan assets primarily over a five-year period and as a result future pension expense will be impacted when these previously deferred

gains or losses are recorded. See the new accounting pronouncements below for the effect of SFAS No. 158, Employers’ Accounting

for Defined Pension and Other Post Retirement Plans an amendment of FASB Statements No. 87, 88, 106 and 132(R).

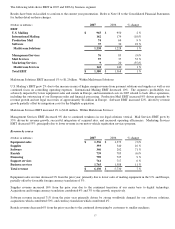

Investment related risks and uncertainties

We invest our pension plan assets in a variety of investment securities in accordance with our strategic asset allocation policy. The

composition of our U.S. pension plan assets at December 31, 2008 was approximately 50% equity securities, 39% fixed income

securities, 7% real estate investments and 4% private equity investments. The composition of our U.K. pension plan assets at

December 31, 2008 was approximately 63% equity securities, 33% fixed income securities and 4% cash. Investment securities are

exposed to various risks such as interest rate, market and credit risks. In particular, due to the level of risk associated with equity

securities, it is reasonably possible that changes in the values of such investment securities will occur and that such changes could

materially affect our future results.

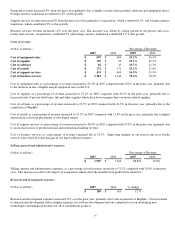

New Accounting Pronouncements

In June 2006, the Financial Accounting Standards Board (“FASB”) issued FASB Interpretation (FIN) No. 48, Accounting for

Uncertainty in Income Taxes (“FIN 48”), which supplements Statement of Financial Accounting Standard No. 109, Accounting for

Income Taxes, by defining the confidence level that a tax position must meet in order to be recognized in the financial statements. FIN

48 requires the tax effect of a position to be recognized only if it is “more-likely-than-not” to be sustained based solely on its technical

merits as of the reporting date. If a tax position is not considered more-likely-than-not to be sustained based solely on its technical

merits, no benefits of the position are recognized. This is a different standard for recognition than was previously required. The more-

likely-than-not threshold must continue to be met in each reporting period to support continued recognition of a benefit. At adoption,

companies adjusted their financial statements to reflect only those tax positions that were more-likely-than-not to be sustained as of

the adoption date. Any necessary adjustment was recorded directly to opening retained earnings in the period of adoption and reported

as a change in accounting principle. We adopted the provisions of FIN 48 on January 1, 2007 which resulted in a decrease to opening

retained earnings of $84.4 million, with a corresponding increase in our tax liabilities.