Pep Boys 2007 Annual Report Download - page 94

Download and view the complete annual report

Please find page 94 of the 2007 Pep Boys annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

|

|

THE PEP BOYS—MANNY, MOE & JACK AND SUBSIDIARIES

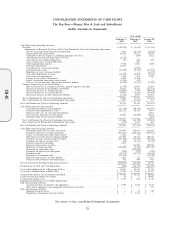

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Continued)

Years ended February 2, 2008, February 3, 2007 and January 28, 2006

(dollar amounts in thousands, except share data)

Accumulated Other Comprehensive Loss of $123. This net charge to Retained Earnings represents the

after-tax pension expense for the period from January 1, 2008 to February 2, 2008.

In February 2007, the FASB issued SFAS No. 159, ‘‘The Fair Value Option for Financial Assets

and Financial Liabilities.’’ SFAS No. 159 permits entities to choose to measure many financial

instruments and certain other items at fair value. SFAS 159 is effective for fiscal years beginning after

November 15, 2007. The Company has not chosen to measure any asset or liability using SFAS 159.

In March 2007, the EITF reached a consensus on Issue Number 06-10, ‘‘Accounting for Deferred

Compensation and Postretirement Benefit Aspects of Collateral Assignment Split-Dollar Life Insurance

Arrangements’’ (EITF 06-10). EITF 06-10 provides guidance to help companies determine whether a

liability for the postretirement benefit associated with a collateral assignment split-dollar life insurance

arrangement should be recorded in accordance with either SFAS No. 106, ‘‘Employers’ Accounting for

Postretirement Benefits Other Than Pensions’’ (if, in substance, a postretirement benefit plan exists), or

Accounting Principles Board Opinion No. 12 (if the arrangement is, in substance, an individual

deferred compensation contract). EITF 06-10 also provides guidance on how a company should

recognize and measure the asset in a collateral assignment split-dollar life insurance contract.

EITF 06-10 is effective for fiscal years beginning after December 15, 2007, although early adoption is

permitted. The Company anticipates the adoption of EITF 06-10 will result in a $1,855 pretax charge to

retained earnings on February 3, 2008.

In June 2007, the FASB ratified EITF Issue Number 06-11, ‘‘Accounting for Income Tax Benefits

of Dividends on Share-Based Payment Awards’’ (EITF 06-11). EITF 06-11 applies to share-based

payment arrangements with dividend protection features that entitle employees to receive (a) dividends

on equity-classified nonvested shares, (b) dividend equivalents on equity-classified nonvested share

units, or (c) payments equal to the dividends paid on the underlying shares while an equity-classified

share option is outstanding, when those dividends or dividend equivalents are charged to retained

earnings under SFAS No. 123(R), ‘‘Share-Based Payment,’’ and result in an income tax deduction for

the employer. A consensus was reached that a realized income tax benefit from dividends or dividend

equivalents that are charged to retained earnings and are paid to employees for equity-classified

non-vested equity shares, non-vested equity share units, and outstanding equity share options should be

recognized as an increase in additional paid-in capital. EITF 06-11 is effective prospectively for the

income tax benefits that result from dividends on equity-classified employee share-based payment

awards that are declared in fiscal years beginning after December 15, 2007, and interim periods within

those fiscal years. The Company has determined that the effects of EITF 06-11 will have an immaterial

impact on its consolidated financial statements beginning in fiscal 2008.

In December 2007, the FASB issued SFAS No. 141R, ‘‘Business Combinations,’’ which replaces

SFAS No. 141, ‘‘Business Combinations.’’ SFAS No. 141R, among other things, establishes principles

and requirements for how an acquirer entity recognizes and measures in its financial statements the

identifiable assets acquired, the liabilities assumed and any controlling interests in the acquired entity;

recognizes and measures the goodwill acquired in the business combination or a gain from a bargain

purchase; and determines what information to disclose to enable users of the financial statements to

evaluate the nature and financial effects of the business combination. Costs of the acquisition will be

recognized separately from the business combination. SFAS No. 141R applies prospectively, except for

taxes, to business combinations for which the acquisition date is on or after the beginning of the first

annual reporting period on or after December 15, 2008.

48

10-K