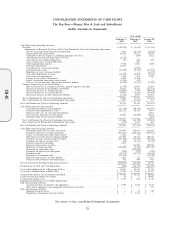

Pep Boys 2007 Annual Report Download - page 93

Download and view the complete annual report

Please find page 93 of the 2007 Pep Boys annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

|

|

THE PEP BOYS—MANNY, MOE & JACK AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Continued)

Years ended February 2, 2008, February 3, 2007 and January 28, 2006

(dollar amounts in thousands, except share data)

In June 2006, the Financial Accounting Standards Board (FASB) issued Financial Interpretation

No. 48, ‘‘Accounting for Uncertainty in Income Taxes’’ (FIN 48), which clarifies the accounting for

uncertainty in income taxes recognized in a company’s financial statements in accordance with the

FASB Statement of Financial Accounting Standards (SFAS) No. 109, ‘‘Accounting for Income Taxes.’’

The interpretation prescribes a recognition threshold and measurement attribute criteria for the

financial statement recognition and measurement of a tax position taken or expected to be taken in a

tax return. The interpretation also provides guidance on derecognition, classification, interest and

penalties, accounting in interim periods, disclosure and transition.

The Company adopted the provisions of FIN 48 on February 4, 2007. In connection with the

adoption, the Company recorded a net decrease to retained earnings of $155 and reclassified certain

previously recognized deferred tax attributes as FIN 48 liabilities. The amount of unrecognized tax

benefits including $734 of interest at February 4, 2007 was $7,126 of which 2,244 would impact the

Company’s tax rate, if recognized. At February 2, 2008, the amount of the unrecognized tax benefit was

$3,847. For additional information, see Note 14, ‘‘Income Taxes.’’

In September 2006, the FASB issued SFAS No. 157, ‘‘Fair Value Measurements’’ (SFAS 157).

SFAS 157 defines the term fair value, establishes a framework for measuring it within generally

accepted accounting principles and expands disclosures about its measurements. In February 2008, the

FASB issued Staff Position No. FAS 157-2 (FSP No.157-2), ‘‘Effective Date of FASB Statement

No. 157,’’ that defers the effective date of SFAS 157 for one year for certain nonfinancial assets and

nonfinancial liabilities. The Company anticipates the adoption of SFAS 157 in fiscal 2008 for financial

assets and financial liabilities will not have a material effect on the Company’s financial statements.

SFAS 157 is effective for certain nonfinancial assets and nonfinancial liabilities for financial statements

issued for fiscal years beginning after November 15, 2008. The Company is currently evaluating the

impact SFAS No. 157 will have on its consolidated financial statements beginning in fiscal 2009.

In September 2006, the FASB issued SFAS No. 158, ‘‘Employers’ Accounting for Defined Benefit

Pension and Other Postretirement Plans- an Amendment of FASB Statements No. 87, 88, 106 and

132(R)’’ (SFAS 158). SFAS No. 158 requires entities to:

• Recognize on its balance sheet the funded status (measured as the difference between the fair

value of plan assets and the benefit obligation) of pension and other postretirement benefit

plans;

• Recognize, through comprehensive income, certain changes in the funded status of a defined

benefit and post retirement plan in the year in which the changes occur;

• Measure plan assets and benefit obligations as of the end of the employer’s fiscal year; and

• Disclose additional information.

The Company adopted the requirement to recognize the funded status of a benefit plan and the

additional disclosure requirements at February 3, 2007. The requirement to measure plan assets and

benefit obligations as of the date of the employer’s fiscal year-end is effective for fiscal years ending

after December 15, 2008. At February 2, 2008, the Company has adopted the SFAS No.158

requirement to measure plan assets and benefit obligations as of the date of the Company’s fiscal year

end. In accordance with SFAS 158, the change of measurement date from a calendar year to the

Company’s fiscal year resulted in a net charge to Retained Earnings of $189 and a credit to

47

10-K