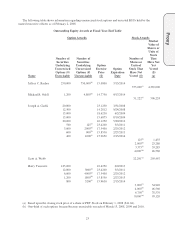

Pep Boys 2007 Annual Report Download - page 41

Download and view the complete annual report

Please find page 41 of the 2007 Pep Boys annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

|

|

A -

2

recommendation to the Board as to the inclusion of the Company’s audited financial statements and assessment of

internal controls in the Company’s Annual Report on Form 10-K.

After consulting with each member of the Committee, the Committee Chair will review the Company's Form 10-

Qs and any Form 8-K which includes financial statements with management and, if appropriate, the Director of

Internal Audit and/or the independent registered public accounting firm.

In connection with all such reviews, the Committee will also review the corresponding (i) proceedings of the

Corporate Accountability Committee in support of the SEC’s required CEO and CFO certifications and (ii)

management representation letters to the independent registered public accounting firm.

4.2 Proxy Statement. To prepare and publish an annual Committee report in the Company's proxy statement.

4.3 Internal Controls Over Financial Reporting. To review with management, the internal audit function and

the independent registered public accounting firm the Company’s policies and procedures to seek assurance as to

the adequacy of the Company’s internal controls over financial reporting. Annually, the Committee shall review the

Company’s plan for documenting and testing the Company’s internal controls and, at least quarterly, shall review

the Company’s progress against such plan and the results of such testing.

4.4 Press Releases. To discuss with management and the independent registered public accounting firm, as

appropriate, earnings press releases and any other press releases which contain previously non-public material

financial information. The Committee shall review all such releases with management prior to their release to the

public.

4.5 Independent Registered Public Accounting Firm. To select the independent registered public accounting

firm to examine the Company's accounts, controls and financial statements and to ask the full Board to seek the

shareholders’ ratification of such selection at each Annual Meeting of Shareholders. The Committee shall have the

sole authority and responsibility to select, evaluate, compensate and oversee the work of any registered public

accounting firm engaged for the purpose of preparing or issuing an audit report or performing other audit, review or

attest services for the Company (including resolution of disagreements between management and the registered

public accounting firm regarding financial reporting). The independent registered public accounting firm and each

such registered public accounting firm will report directly to the Committee. The Committee shall have the sole

authority to approve all audit engagement fees and terms and the Committee must pre-approve any audit and non-

audit service provided to the Company by the Company's independent registered public accounting firm.

To obtain and review at least annually a formal written report from the independent registered public accounting

firm delineating (i) the auditing firm's internal quality-control procedures and (ii) any material issues raised within

the preceding five years by the auditing firm's internal quality-control reviews, by peer reviews of the firm or by any

governmental or other inquiry or investigation relating to any audit conducted by the firm. The Committee will also

review steps taken by the auditing firm to address any findings in any of the foregoing reviews. Also, in order to

assess the independence of the independent registered public accounting firm, the committee will review at least

annually all relationships between the independent registered public accounting firm and the Company.

To set policies for the hiring of employees or former employees of the Company's independent registered public

accounting firm.

To ensure that the lead audit partners assigned by the Company's independent registered public accounting firm

to the Company, as well as the audit partner responsible for reviewing the Company's audit shall be changed at least

every five years.

To consider whether there should be regular rotation of the independent audit firm to assure continuing

independence of the independent registered public accounting firm.

The Committee shall have the authority to dismiss the independent registered public accounting firm if it deems

necessary at any time.

Proxy