Pep Boys 2007 Annual Report Download - page 85

Download and view the complete annual report

Please find page 85 of the 2007 Pep Boys annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

|

|

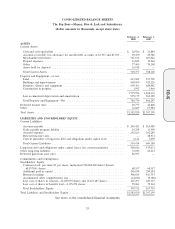

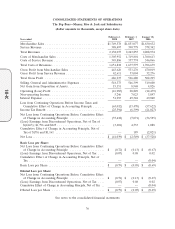

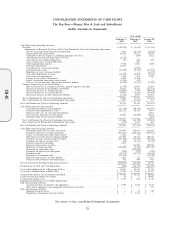

THE PEP BOYS—MANNY, MOE & JACK AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

Years ended February 2, 2008, February 3, 2007 and January 28, 2006

(dollar amounts in thousands, except share data)

NOTE 1—SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

BUSINESS The Pep Boys—Manny, Moe & Jack and subsidiaries (the ‘‘Company’’) is engaged

principally in the retail sale of automotive parts and accessories, automotive maintenance and service

and the installation of parts through a chain of stores. The Company currently operates stores in 35

states and Puerto Rico.

FISCAL YEAR END The Company’s fiscal year ends on the Saturday nearest to January 31.

Fiscal year 2007, which ended February 2, 2008, was comprised of 52 weeks, fiscal year 2006, which

ended February 3, 2007, was comprised of 53 weeks and fiscal year 2005, which ended January 28,

2006, was comprised of 52 weeks.

PRINCIPLES OF CONSOLIDATION The consolidated financial statements include the accounts

of the Company and its wholly owned subsidiaries. All intercompany balances and transactions have

been eliminated.

USE OF ESTIMATES The preparation of the Company’s consolidated financial statements in

conformity with accounting principles generally accepted in the United States of America necessarily

requires management to make estimates and assumptions that affect the reported amounts of assets

and liabilities and disclosure of contingent assets and liabilities at the date of the consolidated financial

statements and the reported amounts of revenues and expenses during the reporting period. Actual

results could differ from those estimates.

MERCHANDISE INVENTORIES Merchandise inventories are valued at the lower of cost or

market. Cost is determined by using the last-in, first-out (LIFO) method. An actual valuation of

inventory under the LIFO method can be made only at the end of each fiscal year based on inventory

and costs at that time. Accordingly, interim LIFO calculations must be based on management’s

estimates of expected fiscal year-end inventory levels and costs. If the first-in, first-out (FIFO) method

of costing inventory had been used by the Company, inventory would have been $555,188 and $600,035

as of February 2, 2008 and February 3, 2007, respectively. During fiscal 2007 and 2006, the effect of

LIFO layer liquidations on gross profit was immaterial.

The Company also records valuation adjustments for potentially excess and obsolete inventories

based on current inventory levels, the historical analysis of product sales and current market conditions.

The nature of the Company’s inventory is such that the risk of obsolescence is minimal and excess

inventory has historically been returned to the Company’s vendors for credit. The Company records

those valuation adjustments when less than full credit is expected from a vendor or when market is

lower than recorded costs. The valuation adjustments are revised, if necessary, on a quarterly basis for

adequacy. The Company’s inventory is recorded net of valuation adjustments for these matters which

were $11,167 and $13,462 as of February 2, 2008 and February 3, 2007, respectively.

During the third quarter of fiscal 2007, the Company recorded a $32,803 inventory impairment for

the discontinuance and planned exit of certain non-core merchandise products adopted as one of the

initial steps in the Company’s five-year strategic plan. The impairment charge reduced the carrying

value of the discontinued merchandise from $74,080 to $41,277. The carrying value of the discontinued

merchandise will be evaluated quarterly as compared to the estimated sell through that was utilized in

determining the impairment. The inventory impairment was recorded in cost of merchandise sales on

39

10-K