NetSpend 2014 Annual Report Download - page 18

Download and view the complete annual report

Please find page 18 of the 2014 NetSpend annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

|

|

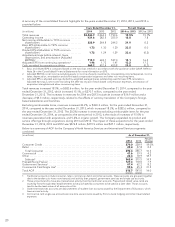

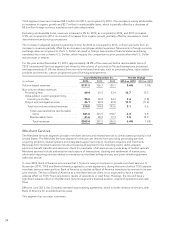

Acquisitions — Purchase Price Allocation

TSYS’ purchase price allocation methodology requires the Company to make assumptions and to apply judgment

to estimate the fair value of acquired assets and liabilities. TSYS estimates the fair value of assets and liabilities

based upon appraised market values, the carrying value of the acquired assets and widely accepted valuation

techniques, including discounted cash flows and market multiple analyses. Management determines the fair value

of fixed assets and identifiable intangible assets such as developed technology or customer relationships, and

any other significant assets or liabilities. TSYS adjusts the purchase price allocation, as necessary, up to one year

after the acquisition closing date as TSYS obtains more information regarding asset valuations and liabilities

assumed. Unanticipated events or circumstances may occur which could affect the accuracy of the Company’s fair

value estimates, including assumptions regarding industry economic factors and business strategies, and result in

an impairment or a new allocation of purchase price.

Given its history of acquisitions, TSYS may allocate part of the purchase price of future acquisitions to contingent

consideration as required by generally accepted accounting principles (GAAP) for business combinations. The fair

value calculation of contingent consideration will involve a number of assumptions that are subjective in nature

and which may differ significantly from actual results. TSYS may experience volatility in its earnings to some

degree in future reporting periods as a result of these fair value measurements.

Goodwill

In evaluating for impairment, discounted net cash flows for future periods are estimated by management. In

accordance with the provisions of GAAP, goodwill is required to be tested for impairment at least annually. The

combination of the income approach utilizing the discounted cash flow (DCF) method and the market approach,

utilizing readily available market valuation multiples, is used to estimate the fair value. Under the DCF method,

the fair value of the asset reflects the present value of the projected earnings that will be generated by each asset

after taking into account the revenues and expenses associated with the asset, the relative risk that the cash flows

will occur, the contribution of other assets, and an appropriate discount rate to reflect the value of invested

capital. Cash flows are estimated for future periods based on historical data and projections provided by

management. If the actual cash flows are not consistent with the Company’s estimates, a material impairment

charge may result and net income may be materially different than was initially recorded. Note 7 in the

Consolidated Financial Statements contains a discussion of goodwill. The net carrying value of goodwill on the

Company’s Consolidated Balance Sheet as of December 31, 2014 was $1.5 billion.

Long-lived Assets and Intangibles

In evaluating long-lived assets and intangibles for recoverability, expected undiscounted net operating cash flows

are estimated by management. The Company reviews long-lived assets, such as property and equipment and

intangibles subject to amortization, including contract acquisition costs and certain computer software, for

impairment whenever events or changes in circumstances indicate that the carrying amount of an asset may not

be recoverable. Recoverability of assets to be held and used is measured by a comparison of the carrying amount

of an asset to estimated undiscounted future cash flows expected to be generated by the asset. If the actual cash

flows are not consistent with the Company’s estimates, a material impairment charge may result and net income

may be materially different than was initially recorded.

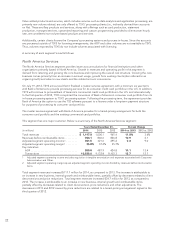

Revenue Recognition

The Company recognizes revenues in accordance with the provisions of GAAP, which sets forth guidance as to

when revenue is realized or realizable and earned when all of the following criteria are met: (1) persuasive

evidence of an arrangement exists; (2) delivery has occurred or services have been performed; (3) the seller’s

price to the buyer is fixed or determinable; and (4) collectability is reasonably assured.

The Company evaluates its contractual arrangements that provide services to clients through a bundled sales

arrangement in accordance with the provisions of GAAP to determine whether an arrangement involving more

than one deliverable (a multiple element arrangement) contains more than one unit of accounting and how the

arrangement consideration should be measured and allocated to the separate units of accounting.

15