NetSpend 2014 Annual Report Download - page 17

Download and view the complete annual report

Please find page 17 of the 2014 NetSpend annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

|

|

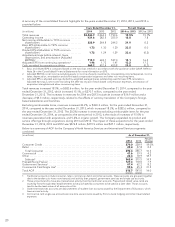

A summary of the Company’s critical accounting estimates applicable to the reportable operating segments

follows:

Allowance for Doubtful Accounts and Billing Adjustments

The Company estimates the allowance for doubtful accounts. When estimating the allowance, the Company

takes into consideration such factors as its knowledge of the financial position of specific clients, the industry and

size of its clients, the overall composition of its accounts receivable aging, prior experience with specific

customers of accounts receivable write-offs and prior history of allowances in proportion to the overall receivable

balance. This analysis includes an ongoing and continuous communication with its largest clients and those

clients with past due balances. A financial decline of any one of the Company’s large clients could have a material

adverse effect on collectability of receivables and thus the adequacy of the allowance for doubtful accounts. If

the actual collectability of clients’ accounts is not consistent with the Company’s estimates, bad debt expense,

which is recorded in selling, general and administrative expenses, may be materially different than was initially

recorded. The Company’s experience and extensive data accumulated historically indicates that these estimates

have proven reliable over time.

The Company estimates allowances for billing adjustments for potential billing discrepancies. When estimating

the allowance for billing adjustments, the Company considers its overall history of billing adjustments, as well as

its history with specific clients and known disputes. If the actual adjustments to clients’ billing are not consistent

with the Company’s estimates, billing adjustments, which are recorded as a reduction of revenues in the

Company’s Consolidated Statements of Income, may be materially different than was initially recorded. The

Company’s experience and extensive data accumulated historically indicates that these estimates have proven

reliable over time. The allowance for doubtful accounts and billing adjustments on the Company’s Consolidated

Balance Sheet as of December 31, 2014 was approximately $5.2 million.

Contract Acquisition Costs

In evaluating contract acquisition costs for recoverability, expected cash flows are estimated by management.

The Company evaluates the carrying value of contract acquisition costs associated with each customer for

impairment on the basis of whether these costs are fully recoverable from either contractual minimum fees

(conversion costs) or from expected undiscounted net operating cash flows of the related contract (cash

incentives paid). The determination of expected undiscounted net operating cash flows requires management to

make estimates. If the actual cash flows are not consistent with the Company’s estimates, a material impairment

charge may result and net income may be materially different than was initially recorded.

These costs may become impaired with the loss of a contract, the financial decline of a client, termination of

conversion efforts after a contract is signed, or diminished prospects for current clients. Note 11 in the

Consolidated Financial Statements contains a discussion of contract acquisition costs. The net carrying value of

contract acquisition costs on the Company’s Consolidated Balance Sheet as of December 31, 2014 was

$236.3 million.

Software Development Costs

In evaluating software development costs for recoverability, expected cash flows are estimated by management.

The Company evaluates the unamortized capitalized costs of software development as compared to the net

realizable value of the software product, which is determined by expected undiscounted net operating cash

flows. The amount by which the unamortized software development costs exceed the net realizable value is

written off in the period that such determination is made. If the actual cash flows are not consistent with the

Company’s estimates, a material write-off may result and net income may be materially different than was initially

recorded. Assumptions and estimates about future cash flows and remaining useful lives of software are complex

and subjective. They can be affected by a variety of factors, including industry and economic trends, changes in

the Company’s business strategy and changes in the internal forecasts. Note 9 in the Consolidated Financial

Statements contains a discussion of internally developed software costs. The net carrying value of internally

developed software on the Company’s Consolidated Balance Sheet as of December 31, 2014 was $100.5 million.

14