Lexmark 2011 Annual Report Download - page 88

Download and view the complete annual report

Please find page 88 of the 2011 Lexmark annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

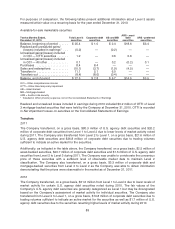

|

|

regards to certain equipment deliverables, thus consideration was allocated using the residual method.

Under the new guidance, if VSOE or TPE is not determinable, the Company utilizes its best estimate of

selling price in order to allocate consideration for those deliverables.

The Company uses its best estimate of selling price when allocating the transaction price for most of its

deliverables. Best estimate of selling price for the Company’s product deliverables is determined by

utilizing a weighted average price approach. Best estimate of selling price for the Company’s service

deliverables is determined by utilizing a cost plus margin approach. These approaches are described

further in the paragraphs below.

The Company’s method for determining management’s best estimate of selling price for products starts

with a review of historical standalone sales data. Prior sales are grouped by product and key data

points utilized such as the average unit price and the weighted average price in order to incorporate

the frequency of each product sold at any given price. Due to the large number of product offerings,

products are then grouped into common product categories (families) incorporating similarities in

function and use and a BESP discount is determined by common product category. This discount is

then applied to product list price to arrive at a product BESP. This method is performed and applied at

a geography level in order to incorporate variances in product pricing across worldwide boundaries.

The Company does not typically sell its services on a standalone basis, thus a best estimate of selling

price for services is determined using a cost plus margin approach. The Company typically uses third

party suppliers to provide the services component of its multiple element arrangements, thus the cost

of services is that which is invoiced to the Company. A margin is applied to the cost of services in order

to determine a best estimate of selling price, and is primarily determined by considering third party

prices of similar services to consumers and geographic factors. In the absence of third party data the

Company considers other factors such as historical margins and margins on similar deals as well as

cost drivers that could affect future margins.

For multiple deliverable arrangements that involve capital leases or the upfront purchase of hardware

equipment, the use of best estimate of selling price could result in the Company recognizing a larger

portion of revenue earlier in the contract life when compared to using the residual method under prior

guidance. This difference in the timing of revenue recognition did not have a material impact to the

Company’s 2011 consolidated financial statements and is not expected to materially impact the

Company’s financial statements for new or materially modified arrangements. Additionally, there will be

little to no effect on the timing of revenue recognition from the use of a best estimate of selling price for

operating leases or for the services and supplies components of multiple deliverable arrangements as

revenue for deliverables in these arrangements is recognized ratably or as services are performed.

With respect to the new software guidance, the modification did not result in a change in the amounts

or timing of revenue recognition for the Company’s multiple deliverable arrangements that contain

software components. Software included within the equipment component that was considered

incidental under the previous guidance will continue to be accounted for as part of the sale of the

equipment under the amended guidance. Software that is not considered incidental and does not

function together with the non-software components to deliver the equipment’s essential functionality

will continue to be accounted for under the industry-specific software revenue recognition guidance.

The residual method of allocating arrangement consideration is still permitted under the industry-

specific software revenue recognition guidance.

Accounting Standards Updates Recently Issued But Not Yet Effective

In May 2011, the FASB issued ASU No. 2011-04, Fair Value Measurement (Topic 820): Amendments

to Achieve Common Fair Value Measurement and Disclosure Requirements in U.S. GAAP and IFRSs

(“ASU 2011-04”). ASU 2011-04 changes certain fair value measurement principles and clarifies the

84