Lexmark 2011 Annual Report Download - page 72

Download and view the complete annual report

Please find page 72 of the 2011 Lexmark annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

|

|

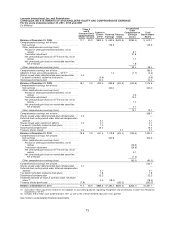

Item 7A. QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK

MARKET RISK SENSITIVITY

The market risk inherent in the Company’s financial instruments and positions represents the potential

loss arising from adverse changes in interest rates and foreign currency exchange rates.

Interest Rates

At December 31, 2011, the fair value of the Company’s senior notes was estimated at $696.6 million

based on the prices the bonds have recently traded in the market as well as the overall market

conditions on the date of valuation. The fair value of the senior notes exceeded the carrying value as

recorded in the Consolidated Statements of Financial Position at December 31, 2011 by approximately

$47.3 million. Market risk is estimated as the potential change in fair value resulting from a hypothetical

10% adverse change in interest rates and amounts to approximately $9.5 million at December 31,

2011.

At December 31, 2010, the fair value of the Company’s senior notes was estimated at $693.8 million

based on the prices the bonds have recently traded in the market as well as the overall market

conditions on the date of valuation. The fair value of the senior notes exceeded the carrying value as

recorded in the Consolidated Statements of Financial Position at December 31, 2010 by approximately

$44.7 million. Market risk is estimated as the potential change in fair value resulting from a hypothetical

10% adverse change in interest rates and amounted to approximately $12.7 million at December 31,

2010.

See the section titled “LIQUIDITY AND CAPITAL RESOURCES — Investing Activities:” in Item 7 of

this report for a discussion of the Company’s auction rate securities portfolio which is incorporated

herein by reference.

Foreign Currency Exchange Rates

Foreign currency exposures arise from transactions denominated in a currency other than the

functional currency of the Company or the respective foreign currency of each of the Company’s

subsidiaries. The primary currencies to which the Company was exposed on a transaction basis as of

the end of the fourth quarter include the Euro, the Canadian dollar, the Swiss franc, the Singapore

dollar, the British pound, the Japanese yen, the Hong Kong dollar and the Australian dollar. The

Company primarily hedges its transaction foreign exchange exposures with foreign currency forward

contracts with maturity dates of approximately three months or less. The potential loss in fair value at

December 31, 2011 for such contracts resulting from a hypothetical 10% adverse change in all foreign

currency exchange rates is approximately $4.8 million. This loss would be mitigated by corresponding

gains on the underlying exposures. The potential gain in fair value at December 31, 2010 for such

contracts resulting from a hypothetical 10% adverse change in all foreign currency exchange rates was

approximately $15.2 million. This gain would have been mitigated by corresponding losses on the

underlying exposures.

68