Lexmark 2010 Annual Report Download - page 82

Download and view the complete annual report

Please find page 82 of the 2010 Lexmark annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

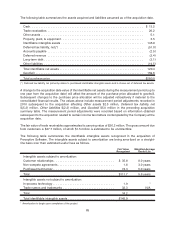

|

|

separate units of accounting. Under the amended guidance, arrangement consideration will be allocated

at the inception of the arrangement to all deliverables on the basis of their relative selling price. When

applying this method, an entity must adhere to the selling price hierarchy; that is, the selling price used for

each deliverable will be based on vendor-specific objective evidence (“VSOE”) if available, third-party

evidence (“TPE”) if vendor-specific objective evidence is not available, or estimated selling price if neither

VSOE nor TPE is available. The vendor’s best estimate of selling price is the price at which the vendor

would transact if the deliverable were sold by the vendor regularly on a standalone basis and should take

into consideration market conditions and entity-specific factors. ASU 2009-13 requires transition

disclosures in the year of adoption and also expands ongoing disclosure requirements for multiple-

deliverable arrangements, requiring qualitative and quantitative information about a vendor’s revenue

arrangements, significant judgments made in applying the guidance, and changes in judgment or

application of the guidance that may significantly affect the timing or amount of revenue recognition.

The new guidance under the ASU must be applied either on a prospective basis to revenue arrangements

entered into or materially modified in the year 2011 or on a retroactive basis. Early adoption is allowed

under the transition guidance of the ASU.

In October 2009, the FASB issued ASU No. 2009-14, Software (Topic 985): Certain Revenue

Arrangements That Include Software Elements (“ASU 2009-14”). ASU 2009-14 contains amendments

to the ASC that change the accounting model for revenue arrangements that include both tangible

products and software elements. Specifically, the ASU modifies the scope of existing software revenue

guidance such that tangible products containing software components and nonsoftware components that

function together to deliver the tangible product’s essential functionality are no longer in scope. The

amendments also require that hardware components of a tangible product containing software

components always be excluded from software revenue guidance. Furthermore, if the software

contained on the tangible product is essential to the tangible product’s functionality, the software is

excluded from software revenue guidance as well. This exclusion would include undelivered elements that

relate to the software that is essential to the tangible product’s functionality. The ASU provides various

factors to consider when determining whether the software and nonsoftware components function

together to deliver the product’s essential functionality. These changes would remove the requirement

to have VSOE of selling price of the undelivered elements sold with a software-enabled tangible product

and could likely increase the ability to separately account for the sale of these products from the

undelivered elements in an arrangement. ASU 2009-14 also provides guidance on how to allocate

consideration when an arrangement includes deliverables that are within the scope of software

revenue guidance (“software deliverables”) and deliverables that are not (“nonsoftware deliverables”).

The consideration must be allocated to the software deliverables as a group and the nonsoftware

deliverables based on the relative selling price method described in ASU 2009-13. The consideration

allocated to the software deliverables group would be subject to further separation and allocation based on

the software revenue guidance. Furthermore, if an undelivered element relates to both a deliverable within

the scope of the software revenue guidance and deliverable not in scope of the software revenue guidance,

the undelivered element must be bifurcated into a software deliverable and a nonsoftware deliverable. An

entity must adopt the amendments in ASU 2009-14 in the same period and using the same transition

method that it uses to adopt the amendments included in ASU 2009-13.

The Company is in the final stages of assessing the financial and operational implications of ASU 2009-13.

The Company enters into various types of multiple-element arrangements and, in many cases, used the

residual method to allocate arrangement consideration under the existing guidance. The elimination of the

residual method for nonsoftware deliverables and required use of the relative selling price method will

result in the Company allocating any discount over all of the deliverables rather than recognizing the entire

discount up front with the delivered items. This change is not expected to have a material impact on the

Company’s financial results based on the preliminary analysis performed to date. The Company has

developed a process that uses stand alone sales data or a cost plus methodology in order to determine

best estimate of selling price for deliverables in which neither VSOE nor TPE is available. Lexmark also

believes that the changes to software revenue guidance from ASU 2009-14 will not have a material impact

to its financial statements today; however, the new guidance may be of greater importance to the Company

76