Lexmark 2010 Annual Report Download - page 81

Download and view the complete annual report

Please find page 81 of the 2010 Lexmark annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

|

|

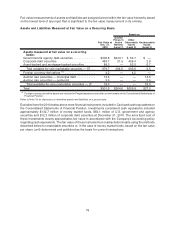

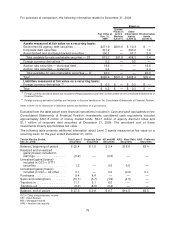

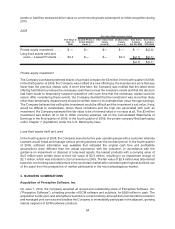

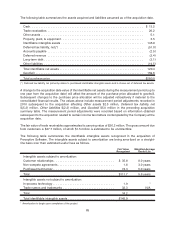

Recent Accounting Pronouncements:

In January 2010, the FASB issued Accounting Standards Update (“ASU”) No. 2010-06, Fair Value

Measurements and Disclosures (Topic 820): Improving Disclosures about Fair Value Measurements

(“ASU 2010-06”) which requires new disclosures and clarifies existing disclosures required under current

fair value guidance. Under the new guidance, a reporting entity must disclose separately gross transfers in

and gross transfers out of Levels 1, 2, and 3 and describe the reasons for the transfers. A reporting entity

must also disclose and consistently follow its policy for determining when transfers between levels are

recognized. The new guidance also requires separate presentation of purchases, sales, issuances, and

settlements rather than net presentation in the Level 3 reconciliation. ASU 2010-06 also requires that the

fair values of derivative assets and liabilities be presented on a gross basis except for the Level 3

reconciliation which may be presented on a net or a gross basis. The ASU also makes clear the

appropriate level of disaggregation for fair value disclosures, which is generally by class of assets and

liabilities, as well as clarifies the requirement to provide disclosures about valuation techniques and inputs

for both recurring and nonrecurring fair value measurements that fall under Level 2 or Level 3. The new

disclosure requirements were effective for the Company in the first quarter of 2010 with the exception of the

requirement to separately disclose purchases, sales, issuances, and settlements which will be effective in

the first quarter of 2011. The Company elected to provide all of the disclosures, including those not

required until 2011, starting in the first quarter of 2010 as permitted under the guidance.

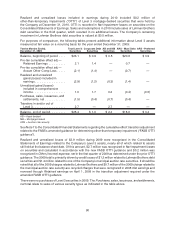

In July 2010, the FASB issued ASU No. 2010-20, Receivables (Topic 310): Disclosures about the Credit

Quality of Financing Receivables and the Allowance for Credit Losses (“ASU 2010-20”). The amendments

in ASU 2010-20 require enhanced disclosures regarding the nature of credit risk in a company’s financing

receivables and how that risk is analyzed. Disclosures required by ASU 2010-20 include credit quality

indicators, non-accrual and past due information, and modifications of financing receivables. Sales-type

and direct financing capital leases are in scope of the new requirements though trade accounts receivable

that arose from the sale of goods or services and have contractual maturities of one year or less are

specifically excluded. Under ASU 2010-20, end of period disclosures were effective for year-end 2010 and

disclosures regarding activity will be effective starting in the first quarter of 2011. The amendments of ASU

2010-20 have no impact on the Company’s consolidated financial results as these changes relate only to

disclosures. Because the Company’s financing receivables are not material to its Consolidated

Statements of Financial Position, the disclosures required under ASU 2010-20 have been omitted

from the Notes to Consolidated Financial Statements with the exception of certain accounting policy

disclosures which describe how the Company assesses and monitors credit risk associated with its

financing receivables.

In January, 2011, the FASB issued ASU No. 2011-01, Receivables (Topic 310): Deferral of the Effective

Date of Disclosures about Troubled Debt Restructurings in Update No. 2010-20 (“ASU 2011-01”). The

amendments in ASU 2011-01 delay the effective date of the disclosures about troubled debt restructurings

in ASU 2010-20 until pending guidance for determining what constitutes a troubled debt restructuring is

completed. The delay was effective upon issuance of ASU 2011-01.

Accounting Standards Issued But Not Yet Effective

In October 2009, the FASB issued ASU No. 2009-13, Revenue Recognition (Topic 605): Multiple-

Deliverable Revenue Arrangements (“ASU 2009-13”). ASU 2009-13 contains amendments to the ASC

that address how to determine whether a multiple-deliverable arrangement contains more than one unit of

accounting and how to measure and allocate arrangement consideration to the separate units of

accounting in the arrangement. The ASU removes the requirement that there be objective and reliable

evidence of fair value of the undelivered item(s) in order to recognize the delivered item(s) as separate

unit(s) of accounting. Under the amended guidance, the delivered item(s) will be considered separate units

of accounting if both the delivered item(s) have value to the customer on a standalone basis and delivery or

performance of the undelivered item(s) is considered probable and substantially in the control of the

vendor when the arrangement includes a general right of return relative to the delivered item. ASU 2009-13

eliminates the use of the residual method when measuring and allocating arrangement consideration to

75