Lexmark 2010 Annual Report Download - page 103

Download and view the complete annual report

Please find page 103 of the 2010 Lexmark annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

|

|

Company does not consider securities in its corporate debt portfolio to be other-than-temporarily impaired

at December 31, 2010.

Asset-backed and mortgage-backed securities

Credit losses for the asset-backed and mortgage-backed securities are derived by examining the

significant drivers that affect loan performance such as pre-payment speeds, default rates, and current

loan status. These drivers are used to apply specific assumptions to each security and are further divided

in order to separate the underlying collateral into distinct groups based on loan performance

characteristics. For instance, more weight is placed on higher risk categories such as collateral that

exhibits higher than normal default rates, those loans originated in high risk states where home

appreciation has suffered the most severe correction, and those loans which exhibit longer

delinquency rates. Based on these characteristics, collateral-specific assumptions are applied to build

a model to project future cash flows expected to be collected. These cash flows are then discounted at the

current yield used to accrete the beneficial interest, which approximates the effective interest rate implicit

in the bond at the date of acquisition for those securities purchased at par. The unrealized losses on the

Company’s remaining asset-backed and mortgage-backed securities are due to constraints in market

liquidity for certain portions of these sectors in which the Company has investments, and are not due to

credit quality. Because the Company does not intend to sell the securities before recovery of their net book

values, the Company does not consider the remainder of its asset-backed and mortgage-backed debt

portfolio to be other-than-temporarily impaired at December 31, 2010.

Government and Agency securities

The unrealized losses on the Company’s investments in government and agency securities are the result

of interest rate effects. Because the Company does not intend to sell the securities and it is not more likely

than not that the Company will be required to sell the securities before recovery of their net book values, the

Company does not consider these investments to be other-than-temporarily impaired at December 31,

2010.

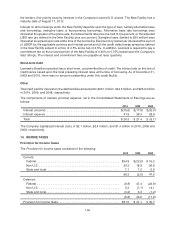

8. TRADE RECEIVABLES

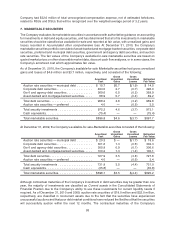

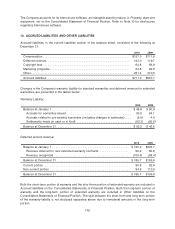

The Company’s trade receivables are reported in the Consolidated Statements of Financial Position net of

allowances for doubtful accounts and product returns. Trade receivables consisted of the following at

December 31:

2010 2009

Gross trade receivables . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $512.4 $458.6

Allowances . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . (32.8) (33.7)

Trade receivables, net . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $479.6 $424.9

In the U.S., the Company transfers a majority of its receivables to its wholly-owned subsidiary, Lexmark

Receivables Corporation (“LRC”), which then may transfer the receivables on a limited recourse basis to

an unrelated third party. The financial results of LRC are included in the Company’s consolidated financial

results since it is a wholly owned subsidiary. LRC is a separate legal entity with its own separate creditors

who, in a liquidation of LRC, would be entitled to be satisfied out of LRC’s assets prior to any value in LRC

becoming available for equity claims of the Company. The Company accounts for transfers of receivables

from LRC to the unrelated third party as a secured borrowing with the pledge of its receivables as collateral

since LRC has the ability to repurchase the receivables interests at a determinable price.

In October 2010, the agreement was amended by extending the term of the facility to September 30, 2011

and increasing the maximum capital availability under the trade receivables facility from $100 million to

$125 million. As of December 31, 2010 and December 31, 2009, there were no secured borrowings under

the facility.

97