IHOP 2008 Annual Report Download - page 77

Download and view the complete annual report

Please find page 77 of the 2008 IHOP annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

|

|

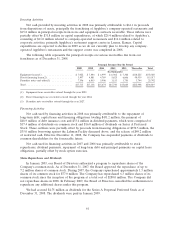

We believe the following critical accounting policies require us to make significant judgments and

estimates in the preparation of our consolidated financial statements:

Purchase Price Allocation

The purchase price for acquisitions is allocated to the identifiable tangible and intangible assets

acquired and liabilities assumed based on their respective fair values in accordance with Statement of

Financial Accounting Standards (‘‘SFAS’’) No. 141, Business Combinations (‘‘SFAS 141’’). The

determination of estimated fair values of identifiable intangible assets and certain tangible assets

requires significant estimates and assumptions, including but not limited to, determining the estimated

future cash flows, estimated useful lives of assets and appropriate discount rates. We believe the

estimated fair values assigned to the Applebee’s assets acquired and liabilities assumed are based on

reasonable assumptions. However, the fair value estimates for the purchase price allocation may change

during the allowable allocation period under SFAS 141, which is up to one year from the acquisition

date, if additional information becomes available that would require changes to our estimates.

Long-Lived Assets

We assess long-lived and intangible assets with finite lives for impairment when events or changes

in circumstances indicate that the carrying value of the assets may not be recoverable. We test

impairment using historical cash flows and other relevant facts and circumstances as the primary basis

for our estimates of future cash flows. We consider factors such as the number of years the restaurant

has been operated by us, sales trends, cash flow trends, remaining lease life, and other factors which

apply on a case-by-case basis. The analysis is performed at the individual restaurant level for indicators

of permanent impairment. Recoverability of the restaurant’s assets is measured by comparing the assets’

carrying value to the undiscounted cash flows expected to be generated over the assets’ remaining

useful life or remaining lease term, whichever is less. If the total expected undiscounted future cash

flows are less than the carrying amount of the assets, the carrying amount is written down to the

estimated fair value, and a loss resulting from impairment is recognized by charging to earnings. This

process requires the use of estimates and assumptions, which are subject to a high degree of judgment.

If these assumptions change in the future, we may be required to record impairment charges for these

assets.

Goodwill and Intangibles

Goodwill is recorded when the aggregate purchase price of an acquisition exceeds the estimated

fair value of the net identified tangible and intangible assets acquired. Intangible assets resulting from

the acquisition are accounted for using the purchase method of accounting and are estimated by

management based on the fair value of the assets received. Identifiable intangible assets are comprised

primarily of trademarks, trade names and franchise agreements. Identifiable assets are being amortized

over the period of estimated benefit using the straight-line method and estimated useful lives. Goodwill

and indefinite life intangible assets are not subject to amortization.

In accordance with SFAS No. 142, Goodwill and Other Intangible Assets (‘‘SFAS 142’’), goodwill has

been allocated to three reporting units, the IHOP franchised restaurants unit (‘‘IHOP unit’’),

Applebee’s company-operated restaurants unit (‘‘Applebee’s company unit’’) and Applebee’s franchised

restaurants unit (‘‘Applebee’s franchise unit’’). The significant majority of the Company’s goodwill

resulted from the November 29, 2007 acquisition of Applebee’s and has been allocated between the

two Applebee’s units. The Company tests goodwill and other indefinite life intangible assets for

impairment on an annual basis in the fourth quarter. The impairment test of goodwill of the two

Applebee’s units was performed as of October 31, 2008. The impairment test of the goodwill of the

IHOP unit was performed as of December 31, 2008, the date as of which the analysis has been

performed in prior years. In addition to the annual test of impairment, goodwill must be evaluated

63