HTC 2015 Annual Report Download - page 128

Download and view the complete annual report

Please find page 128 of the 2015 HTC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

|

|

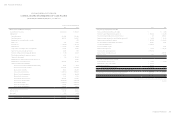

Financial information

Financial information

252

253

allowance account are recognized in profit or loss.

c. Derecognition of financial assets

The Company derecognizes a financial asset only when

the contractual rights to the cash flows from the asset

expire, or when it transfers the financial asset and

substantially all the risks and rewards of ownership of the

asset to another party.

On derecognition of a financial asset in its entirety, the

difference between the asset's carrying amount and the

sum of the consideration received and receivable and the

cumulative gain or loss that had been recognized in other

comprehensive income and accumulated in equity is

recognized in profit or loss.

Equity instruments

Debt and equity instruments issued by a group entity

are classified as either financial liabilities or as equity

in accordance with the substance of the contractual

arrangements and the definitions of a financial liability and an

equity instrument.

Equity instruments issued by a group entity are recognized at

the proceeds received, net of direct issue costs.

Repurchase of the Company's own equity instruments is

recognized in and deducted directly from equity. No gain or

loss is recognized in profit or loss on the purchase, sale, issue

or cancellation of the Company's own equity instruments.

Financial liabilities

a. Subsequent measurement

Except the following situation, all the financial liabilities

are measured at amortized cost using the effective interest

method:

Financial liabilities at fair value through profit or loss

(FVTPL)

Financial liabilities are classified as at FVTPL when

the financial liability is either held for trading or it is

designated as at FVTPL.

A financial liability may be designated as at fair value

through profit or loss upon initial recognition when doing

so results in more relevant information and if:

• Such designation eliminates or significantly reduces a

measurement or recognition inconsistency that would

otherwise arise; or

• The financial liability forms part of a group of financial

assets or financial liabilities or both, which is managed

and its performance is evaluated on a fair value basis,

in accordance with the Company's documented risk

management or investment strategy, and information

about the grouping is provided internally on that basis;

or

• The contract contains one or more embedded

derivatives so that the entire combined contract (asset

or liability) can be designated as at fair value through

profit or loss.

Financial liabilities at FVTPL are stated at fair value, with

any gains or losses arising on remeasurement recognized

in profit or loss. The net gain or loss recognized in profit

or loss incorporates any interest and dividend paid on the

financial liability. Fair value is determined in the manner

described in Note31.

b. Derecognition of financial liabilities

The difference between the carrying amount of the

financial liability derecognized and the consideration

paid, including any non-cash assets transferred or

liabilities assumed, is recognized in profit or loss.

Derivative financial instruments

The Company enters into a variety of derivative financial

instruments to manage its exposure to foreign exchange rate

risks, including foreign exchange forward contracts.

Derivatives are initially recognized at fair value at the date the

derivative contracts are entered into and are subsequently

remeasured to their fair value at the end of each reporting

period. The resulting gain or loss is recognized in profit or

loss immediately unless the derivative is designated and

effective as a hedging instrument, in which event the timing

of the recognition in profit or loss depends on the nature of

the hedge relationship. When the fair value of derivative

financial instruments is positive, the derivative is recognized

as a financial asset; when the fair value of derivative financial

instruments is negative, the derivative is recognized as a

financial liability.

Derivatives embedded in non-derivative host contracts are

treated as separate derivatives when they meet the definition

of a derivative, their risks and characteristics are not closely

related to those of the host contracts and the contracts are not

measured at FVTPL.

Hedge Accounting

The Company designates certain hedging instruments, which

include derivatives, embedded derivatives and non-derivatives

in respect of foreign currency risk, as either cash flow hedges.

Hedges of foreign exchange risk on firm commitments are

accounted for as cash flow hedges.

Fair value hedges

Changes in the fair value of derivatives that are designated

and qualify as fair value hedges are recognized in profit or loss

immediately, together with any changes in the fair value of the

hedged asset or liability that are attributable to the hedged

risk. The change in the fair value of the hedging instrument

and the change in the hedged item attributable to the hedged

risk are recognized in profit or loss in the line item relating to

the hedged item.

Hedge accounting is discontinued prospectively when the

Company revokes the designated hedging relationship, or

when the hedging instrument expires or is sold, terminated,

or exercised, or when it no longer meets the criteria for hedge

accounting.

Cash flow hedges

The effective portion of changes in the fair value of derivatives

that are designated and qualify as cash flow hedges is

recognized in other comprehensive income. The gain or loss

relating to the ineffective portion is recognized immediately

in profit or loss.

The associated gains or losses that were recognized in other

comprehensive income are reclassified from equity to profit

or loss as a reclassification adjustment in the line item relating

to the hedged item in the same period when the hedged item

affects profit or loss. If a hedge of a forecast transaction

subsequently results in the recognition of a non-financial

asset or a non-financial liability, the associated gains and

losses that were recognized in other comprehensive income

are removed from equity and are included in the initial cost of

the non-financial asset or non-financial liability.

Hedge accounting is discontinued prospectively when the

Company revokes the designated hedging relationship, or

when the hedging instrument expires or is sold, terminated,

or exercised, or when it no longer meets the criteria for hedge

accounting. The cumulative gain or loss on the hedging

instrument that has been previously recognized in other

comprehensive income from the period when the hedge

was effective remains separately in equity until the forecast

transaction occurs. When a forecast transaction is no longer

expected to occur, the gain or loss accumulated in equity is

recognized immediately in profit or loss.

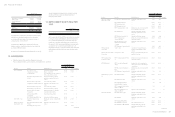

Provisions

Provisions, including those arising from contractual obligation

specified in service concession arrangement to maintain or

restore infrastructure before it is handed over to the grantor,

are measured at the best estimate of the discounted cash flows

of the consideration required to settle the present obligation

at the end of the reporting period, taking into account the

risks and uncertainties surrounding the obligation.

When some or all of the economic benefits required to settle

a provision are expected to be recovered from a third party,

a receivable is recognized as an asset if it is virtually certain

that reimbursement will be received and the amount of the

receivable can be measured reliably.

a. Warranty provisions

The Company provides warranty service for one year

to two years. The warranty liability is estimated on the

basis of evaluation of the products under warranty, past

warranty experience, and pertinent factors.

b. Provisions for contingent loss on purchase

orders

The provision for contingent loss on purchase orders is

estimated after taking into account the effects of changes

in the product market, evaluating the foregoing effects

on inventory management and adjusting the Company's

purchases.

Revenue Recognition

Revenue is measured at the fair value of the consideration

received or receivable. Revenue is reduced for estimated

customer returns, rebates and other similar allowances. Sales

returns are recognized at the time of sale provided the seller

can reliably estimate future returns and recognizes a liability

for returns based on previous experience and other relevant

factors.

Revenue from the sale of goods is recognized when the goods

are delivered and titles have passed, at which time all the

following conditions are satisfied:

• The Company has transferred to the buyer the significant

risks and rewards of ownership of the goods;

• The Company retains neither continuing managerial

involvement to the degree usually associated with

ownership nor effective control over the goods sold;

• The amount of revenue can be measured reliably;

• It is probable that the economic benefits associated with

the transaction will flow to the Company; and

• The costs incurred or to be incurred in respect of the

transaction can be measured reliably.