DIRECTV 2003 Annual Report Download - page 112

Download and view the complete annual report

Please find page 112 of the 2003 DIRECTV annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

|

|

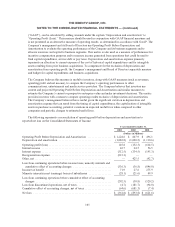

THE DIRECTV GROUP, INC.

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS — (continued)

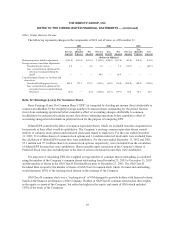

(“GAAP”), can be calculated by adding amounts under the caption “Depreciation and amortization” to

“Operating Profit (Loss).” This measure should be used in conjunction with GAAP financial measures and

is not presented as an alternative measure of operating results, as determined in accordance with GAAP. The

Company’s management and its Board of Directors use Operating Profit Before Depreciation and

Amortization to evaluate the operating performance of the Company and its business segments and to

allocate resources and capital to business segments. This metric is also used as a measure of performance for

incentive compensation purposes and to measure income generated from operations that could be used to

fund capital expenditures, service debt or pay taxes. Depreciation and amortization expense primarily

represents an allocation to current expense of the cost of historical capital expenditures and for intangible

assets resulting from prior business acquisitions. To compensate for the exclusion of depreciation and

amortization from operating profit, the Company’s management and Board of Directors separately measure

and budget for capital expenditures and business acquisitions.

The Company believes this measure is useful to investors, along with GAAP measures (such as revenues,

operating profit and net income), to compare the Company’s operating performance to other

communications, entertainment and media service providers. The Company believes that investors use

current and projected Operating Profit Before Depreciation and Amortization and similar measures to

estimate the Company’s current or prospective enterprise value and make investment decisions. This metric

provides investors with a means to compare operating results exclusive of depreciation and amortization.

The Company’s management believes this is useful given the significant variation in depreciation and

amortization expense that can result from the timing of capital expenditures, the capitalization of intangible

assets in purchase accounting, potential variations in expected useful lives when compared to other

companies and periodic changes to estimated useful lives.

The following represents a reconciliation of operating profit before depreciation and amortization to

reported net loss on the Consolidated Statements of Income:

Years Ended December 31,

2003 2002 2001

(Dollars in Millions)

Operating Profit Before Depreciation and Amortization ................. $1,228.6 $ 867.9 $ 496.1

Depreciation and amortization ..................................... (1,082.8) (1,020.2) (1,110.6)

Operating profit (loss) ............................................ 145.8 (152.3) (614.5)

Interest income ................................................. 42.7 24.5 56.5

Interest expense ................................................. (312.5) (334.5) (195.3)

Reorganization expense ........................................... (212.3) — —

Other,net ...................................................... — 425.5 (92.7)

Loss from continuing operations before income taxes, minority interests and

cumulative effect of accounting changes ........................... (336.3) (36.8) (846.0)

Income tax benefit ............................................... 71.9 27.6 275.9

Minority interests in net (earnings) losses of subsidiaries ................ (28.1) (21.6) 49.9

Loss from continuing operations before cumulative effect of accounting

changes ..................................................... (292.5) (30.8) (520.2)

Loss from discontinued operations, net of taxes ........................ (4.7) (181.7) (94.0)

Cumulative effect of accounting changes, net of taxes ................... (64.6) (681.3) (7.4)

Netloss ....................................................... $ (361.8) $ (893.8) $ (621.6)

105