Clearwire 2008 Annual Report Download - page 68

Download and view the complete annual report

Please find page 68 of the 2008 Clearwire annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

|

|

I

n

d

eterm

i

n

i

n

gf

a

i

rva

l

ue, we use quote

d

pr

i

ces

i

n act

i

ve mar

k

ets w

h

ere suc

h

pr

i

ces are ava

il

a

bl

e, or we use

m

odels to estimate fair value usin

g

various methods includin

g

the market, income and cost approaches. For

i

nvestments w

h

ere we use mo

d

e

l

s to est

i

mate

f

a

i

rva

l

ue

i

nt

h

ea

b

sence o

f

quote

d

mar

k

et pr

i

ces, we o

f

ten ut

ili

ze

c

erta

i

n assumpt

i

ons t

h

at mar

k

et part

i

c

i

pants wou

ld

use

i

npr

i

c

i

ng t

h

e

i

nvestment,

i

nc

l

u

di

ng assumpt

i

ons a

b

out r

i

s

k

and or the risks inherent in the inputs to the valuation technique. These inputs are readil

y

observable, market

c

orro

b

orate

d

, or uno

b

serva

bl

e Company

i

nputs.

We estimate the fair value of securities without quoted market prices usin

g

internall

yg

enerated pricin

g

model

s

th

at requ

i

re var

i

ous

i

nputs an

d

assumpt

i

ons. We

b

e

li

eve t

h

at our pr

i

c

i

ng mo

d

e

l

s,

i

nputs an

d

assumpt

i

ons are w

h

at

m

arket participants would use in pricin

g

the securities. We maximize the use of observable inputs to the pricin

g

m

odels where quoted market prices from securities and derivatives exchan

g

es are available and reliable. We

t

yp

i

ca

ll

y rece

i

ve externa

l

va

l

uat

i

on

i

n

f

ormat

i

on

f

or U.S. Treasur

i

es, ot

h

er U.S. Government an

d

Agency secur

i

t

i

es

,

as well as certain corporate debt securities, mone

y

market funds and certificates of deposit. We also use certain

unobservable inputs that cannot be validated b

y

reference to a readil

y

observable market or exchan

g

e data and rel

y

,

t

o a certa

i

n extent, on management’s own assumpt

i

ons a

b

out t

h

e assumpt

i

ons t

h

at mar

k

et part

i

c

i

pants wou

ld

use

in

p

ricin

g

the securit

y

. Our internall

yg

enerated pricin

g

models ma

y

include our own data and require us to use our

j

ud

g

ment in interpretin

g

relevant market data, matters of uncertaint

y

and matters that are inherentl

y

sub

j

ective i

n

n

ature. We use many

f

actors t

h

at are necessary to est

i

mate mar

k

et va

l

ues,

i

nc

l

u

di

ng,

i

nterest rates, mar

k

et r

i

s

k

s

,

m

ar

k

et sprea

d

s, an

d

t

i

m

i

n

g

o

f

cas

hfl

ows, mar

k

et

li

qu

idi

t

y

,an

d

rev

i

ew o

f

un

d

er

lyi

n

g

co

ll

atera

l

an

d

pr

i

nc

i

pa

l,

i

nterest and dividend pa

y

ments. The use of different

j

ud

g

ments and assumptions could result in different

p

resentations of pricing and security prices could change significantly based on market conditions

.

F

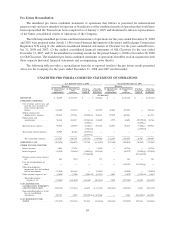

air Value Measurement

s

D

urin

g

2008, we adopted SFAS No. 157

,

F

air Va

l

ue Measurement

s

, which we refer to as SFAS No. 157, for our

financial assets and liabilities that are reco

g

nized or disclosed at fair value on an annual or more frequentl

y

recurrin

g

basis. These include our derivative instruments and our short-term and long-term investments.

As defined in SFAS No. 1

5

7, fair value is the

p

rice that would be received to sell an asset or

p

aid to transfer a

li

a

bili

ty

i

nanor

d

er

l

y transact

i

on

b

etween mar

k

et part

i

c

i

pants at t

h

e measurement

d

ate. In

d

eterm

i

n

i

ng

f

a

i

rva

l

ue,

we utilize certain assumptions that market participants would use in pricin

g

the asset or liabilit

y

, includin

g

assumptions about risk. These inputs can be readil

y

observable, market corroborated, or

g

enerall

y

unobservable

i

nputs. We ut

ili

ze va

l

uat

i

on tec

h

n

i

ques t

h

at max

i

m

i

ze t

h

e use o

f

o

b

serva

bl

e

i

nputs an

d

m

i

n

i

m

i

ze t

h

e use o

f

unobservable inputs. Based on the observabilit

y

of the inputs used in the valuation techniques, we are required t

o

p

rovide the followin

g

information accordin

g

to the fair value hierarch

y:

L

evel 1: Quoted market

p

rices in active markets for identical assets or liabilities

.

L

eve

l

2: O

b

serva

bl

e mar

k

et

b

ase

di

nputs or uno

b

serva

bl

e

i

nputs t

h

at are corro

b

orate

dby

mar

k

et

d

ata

.

L

eve

l

3: Uno

b

serva

bl

e

i

nputs t

h

at are not corro

b

orate

dby

mar

k

et

d

ata

.

I

n accordance with SFAS No. 157 and our polic

y

, it is our practice to maximize the use of observable inputs and

m

inimize the use of unobservable inputs when developin

g

fair value measurements. When available, we use quoted

m

arket prices to measure fair value. If listed prices or quotes are not available, fair value is based on internall

y

d

eve

l

ope

d

mo

d

e

l

st

h

at pr

i

mar

il

y use, as

i

nputs, mar

k

et-

b

ase

d

or

i

n

d

epen

d

ent

l

y source

d

mar

k

et parameters,

i

ncludin

g

but not limited to interest rate

y

ield curves, volatilities, equit

y

or debt prices, and credit curves. I

n

e

stimatin

g

fair values, we utilize certain assumptions that market participants would use in pricin

g

the financial

i

nstrument,

i

nc

l

u

di

ng assumpt

i

ons a

b

out r

i

s

k

.T

h

e

d

egree o

f

management

j

u

d

gment

i

nvo

l

ve

di

n

d

eterm

i

n

i

ng t

h

e

f

a

i

r

5

6

C

LEARWIRE

CO

RP

O

RATI

O

N AND

SU

B

S

IDIARIE

S

MANA

G

EMENT’

S

DI

SCUSS

I

O

N AND ANALY

S

I

SO

F FINAN

C

IAL

CO

NDITI

O

N

AND RESULTS OF OPERATIONS —

(

Continued

)