Clearwire 2008 Annual Report Download - page 20

Download and view the complete annual report

Please find page 20 of the 2008 Clearwire annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

|

|

•

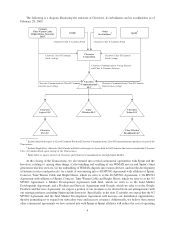

Levera

g

in

gk

e

y

strate

g

ic re

l

ations

h

ips.

W

e expect to

b

ene

fi

t

f

rom our

k

ey strateg

i

cre

l

at

i

ons

hi

ps w

i

t

h

i

ndustr

y

-leaders that have a stron

g

track record of drivin

g

technolo

gy

innovation, deliverin

g

premium

c

ontent, and marketing compelling products and services to consumers, including Sprint, Intel, Google,

Comcast, T

i

me Warner Ca

bl

ean

d

Br

i

g

h

t House. Eac

h

o

f

Spr

i

nt, Comcast, T

i

me Warner Ca

bl

ean

d

Br

i

g

ht

House are entitled to market and resell wireless broadband services over our network as

p

art of a defined

b

un

dl

e, su

bj

ect to certa

i

n except

i

ons, un

d

er t

h

e

i

rown

b

ran

d

names to t

h

e more t

h

an 100 m

illi

on peop

l

e

i

nt

he

Un

i

te

d

States rece

i

v

i

ng t

h

e

i

r serv

i

ces, w

hi

c

h

we

b

e

li

eve w

ill l

ea

d

to more rap

id

growt

hi

nt

h

e num

b

er o

f

peop

l

eus

i

n

g

our networ

k

.Ina

ddi

t

i

on, we

b

e

li

eve t

h

ese re

l

at

i

ons

hi

ps p

l

ace us

i

nana

d

vanta

g

eous pos

i

t

i

on

with respect to access to existing wireless infrastructure, cutting-edge online applications and subscribe

r

d

evices with embedded mobile WiMAX capabilities

.

•

O

ffering premium va

l

ue-a

dd

e

d

services an

d

content.

W

e

i

nten

d

to

g

enerate

i

ncrementa

l

revenues,

l

evera

g

e

our cost structure and improve subscriber retention b

y

offerin

g

a variet

y

of premium services and conten

t

over our network. We intend initially to focus on voice services as a primary premium service. As of

D

ecem

b

er 31, 2008, we o

ff

er VoIP te

l

ep

h

ony serv

i

ces on a

fi

xe

db

as

i

s to our su

b

scr

ib

ers’

h

omes an

d

o

ffi

ce

s

i

n4

5

of our domestic markets. We currentl

y

also offer fixed VoIP telephon

y

services in Portland, Ore

g

on,

and expect to offer mobile VoIP telephon

y

services in each of our mobile WiMAX markets within two t

o

t

h

ree years. Ot

h

er

f

uture serv

i

ce an

d

content o

ff

er

i

ngs may

i

nc

l

u

d

e

li

ve v

id

eocon

f

erenc

i

ng, on

li

ne games

and music broadcast pro

g

rammin

g

, video on demand, and location based services. We believe that ou

r

planned mobile WiMAX deplo

y

ment will enable us to offer additional premium services and content over

our networ

k

as manu

f

acturers

d

eve

l

op an

d

se

ll

su

b

scr

ib

er

d

ev

i

ces t

h

at ta

k

ea

d

vantage o

f

t

h

e capa

bili

t

i

es o

f

m

o

bil

eW

i

MAX tec

h

no

l

o

gy

.

•

Achieving e

ff

icient economics.

W

e believe our economic model for deplo

y

in

g

our network combine

s

m

ean

i

ng

f

u

l

ear

l

y coverage w

hil

e opt

i

m

i

z

i

ng t

h

e cap

i

ta

l

out

l

ay requ

i

re

df

or us to

b

u

ild

t

h

e networ

k

an

d

o

b

ta

i

nsu

b

scr

ib

ers. We

b

e

li

eve our

b

us

i

ness requ

i

res s

ig

n

ifi

cant

ly l

ower

fi

xe

d

cap

i

ta

l

an

d

operat

i

n

g

e

xpenditures relative to other wireless and wireline broadband service providers. Our deplo

y

ment pla

n

i

s based on replicable and scalable individual market builds, allowing us to repeat our build-out processes a

s

we expan

d

.Un

d

er our commerc

i

a

l

a

g

reements w

i

t

h

Spr

i

nt, we expect to

b

ea

bl

eto

l

evera

g

eex

i

st

i

n

g

Spr

i

n

t

n

etwor

ki

n

f

rastructure to

b

ot

h

acce

l

erate t

h

e

b

u

ild

-out an

d

re

d

uce t

h

e costs o

f

networ

kd

ep

l

o

y

ment,

i

ncluding utilizing its towers, collocation facilities and fiber resources. We also expect to achieve lowe

r

s

u

b

scr

ib

er acqu

i

s

i

t

i

on costs

d

ue to manu

f

acturers’ p

l

ans to em

b

e

d

mo

bil

eW

i

MAX c

hi

psets

i

nto

h

an

dh

e

ld

c

ommun

i

cat

i

ons an

d

consumer e

l

ectron

i

c

d

ev

i

ces, suc

h

as note

b

oo

k

computers, net

b

oo

k

s, mo

bil

e Interne

t

d

evices, or MIDs, PDAs,

g

amin

g

consoles and MP3 pla

y

ers. This should reduce subscriber acquisition cost

s

b

yre

d

uc

i

ng su

b

s

idi

es an

dl

everag

i

ng manu

f

acturers’

di

str

ib

ut

i

on networ

k

s. As our capa

bili

t

i

es evo

l

ve, w

e

a

l

so expect to generate

i

ncrementa

l

revenue

f

rom our su

b

scr

ib

er

b

ase

b

y

d

eve

l

op

i

ng an

d

o

ff

er

i

ng prem

i

u

m

products and services, such as VoIP telephon

y

services.

S

ervice

s

As o

f

Decem

b

er 31, 2008, we o

ff

er our serv

i

ces pr

i

mar

il

y

i

n 47 mar

k

ets t

h

roug

h

out t

h

eUn

i

te

d

States an

di

n

4

i

nternational markets. Our services toda

y

consist primaril

y

of providin

g

wireless broadband connectivit

y

, and, as of

D

ecember 31, 2008, in 4

5

of our domestic markets, we also offer fixed VoIP telephon

y

services. Domestic sales

accounte

df

or approx

i

mate

l

y 87% o

f

our serv

i

ce revenue

f

or t

h

e year en

d

e

d

Decem

b

er 31, 2008, w

hil

eou

r

i

nternational sales accounted for approximatel

y

13% of service revenue over the same period.

We plan to continue to offer our subscribers a number of Internet and voice services, includin

g

mobile services,

as our pr

i

mary serv

i

ce o

ff

er

i

ngs. We a

l

so p

l

an to o

ff

er va

l

ue-a

dd

e

d

serv

i

ces t

h

roug

h

partners

hi

ps w

i

t

hd

ev

i

ce

m

anufacturers/develo

p

ers, value-added a

pp

lication develo

p

ers, and content develo

p

ment com

p

anies. Unlik

e

e

xistin

g

cellular networks, applications over our mobile WiMAX network will be Internet Protocol-based wit

h

open App

li

cat

i

on Programm

i

ng Inter

f

aces, w

hi

c

h

we re

f

er to as APIs, w

hi

c

h

can

b

e accesse

d

on a var

i

ety o

f

el

ectron

i

c

d

ev

i

ces. We

b

e

li

eve t

hi

s approac

h

s

h

ou

ld

encoura

g

et

h

e cont

i

nua

l

creat

i

on o

f

new app

li

cat

i

ons an

d

t

he

s

erv

i

ces to support t

h

em. Amon

g

ot

h

ers, we expect to

b

ea

bl

e to eventua

lly

o

ff

er

li

ve v

id

eocon

f

erenc

i

n

g

,v

id

eo on

demand, online gaming and music broadcast programming and location-based services as value-added services.

8